Slippage in Trading: Meaning, Causes and How to Reduce It

Slippage in trading is the difference between the expected price of a trade and the price at which it actually executes. This happens mainly during periods of low liquidity or high volatility in the market, often leading to a worse price (negative) and sometimes a better price (positive) than desired, which in turn impacts market orders. It may also happen due to major news or announcements, market openings, and sudden market gaps.

So, the types are negative slippage (buying at a higher price or selling at a lower price than anticipated) and positive slippage (buying at a lower price or selling at a higher price than anticipated). Let us learn more about slippage in trading below.

What is Slippage?

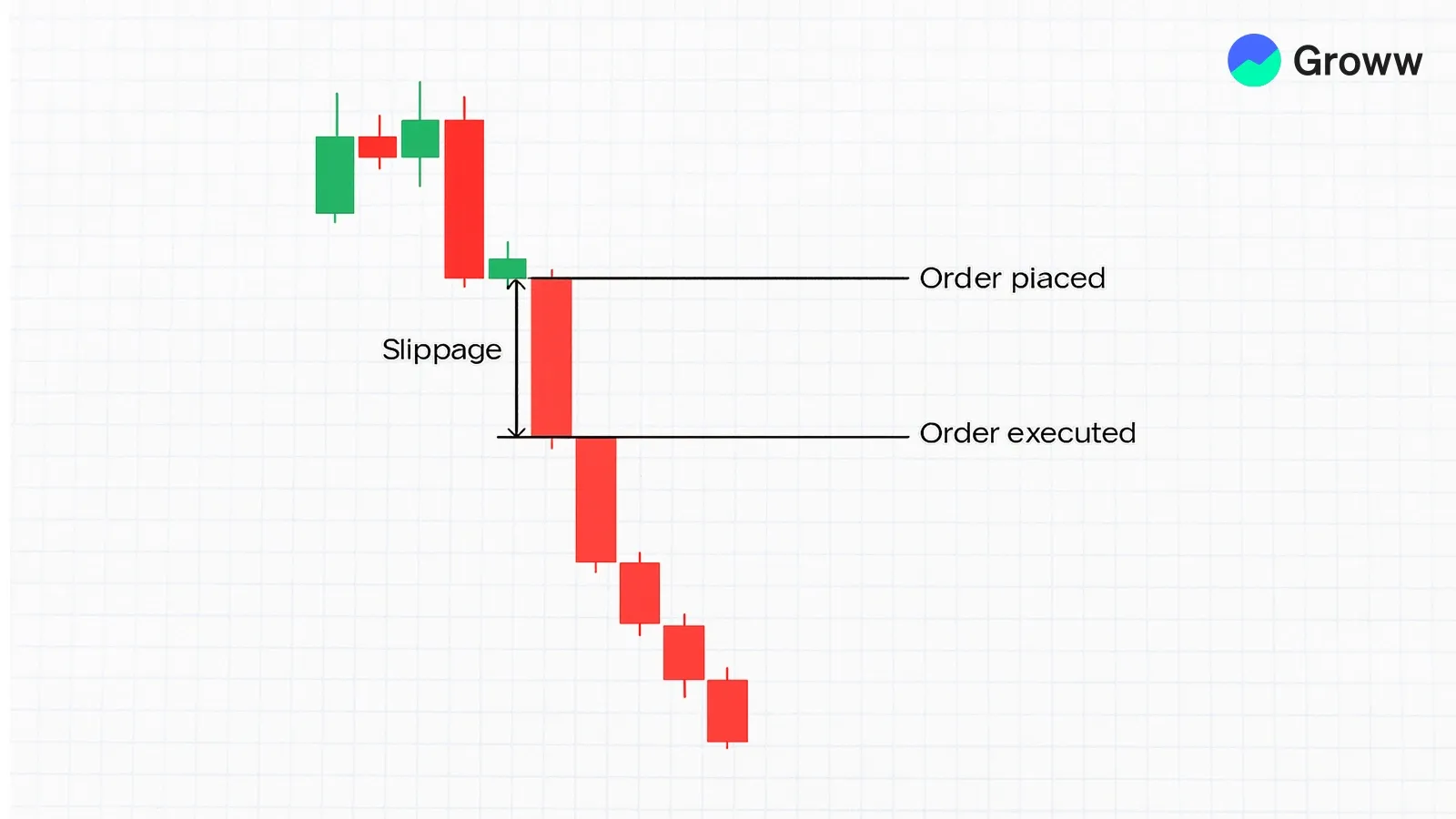

Slippage is the difference between a trade’s expected price and the actual price at which it is executed, often more pronounced during periods of low liquidity or high market volatility. It leads to a quicker but sometimes less favourable execution price and is common in low-volume, high-frequency, or fast-moving markets. Let us take an example to understand the concept.

Suppose you wish to purchase shares of a company at ₹100 and place a market order when you see the prices of the same at ₹100. However, since prices are moving quickly, your order is ultimately processed at ₹101 per share, so you end up paying ₹1 more per share than expected.

Positive Slippage vs Negative Slippage

Let us take a closer look at both positive and negative slippage below:

Positive Slippage:

- It happens when the execution price crosses the intended price, thereby benefiting the trader.

- Buy order: Suppose you place a buy order at ₹100, but it executes at ₹98.

- Sell order: Suppose you place a sell order at ₹100, but it executes at ₹102.

- The outcome is a higher profit or reduced costs.

Negative Slippage:

- It is when the execution price is much worse than the requested price.

- Buy order: You place a buy order at ₹100, but it executes at ₹103.

- Sell order: You place a sell order at ₹100, but it executes at ₹97.

- The outcome is higher losses or increased costs.

People Also Read: Outstanding Shares vs Floating Shares | Types of Stock Market Orders

Why Does Slippage Occur

Slippage occurs when a market order executes at a price different from the anticipated price, typically during periods of low liquidity, high volatility, or rapid market changes. It may happen because the price moves between the time an order is placed and when it is filled, mostly due to fast-moving markets, large, illiquid orders, and major news updates. Let us look at these reasons below:

- Higher volatility: Rapid price fluctuations mean the price at which you order the asset may not be available by the time the order reaches the exchange.

- Lower liquidity: If there are insufficient sellers or buyers at your desired price, then the order will slip to the next best available price.

- Big order sizes: A huge order may surpass the available volume at a particular price point, thereby forcing the broker to fill the order remainder at higher (or lower) prices.

- Gaps in the market: Major news updates, earnings reports, and weekend gaps may trigger price jumps, thereby bypassing intermediate levels and causing orders to be filled at less favourable prices.

- Technical latency: Delays of even microseconds in order execution in high-frequency trading environments may lead to price changes. This will result in slippage.

- Economic announcements: Major news, such as policy or interest rate decisions, may trigger rapid price changes.

- Market orders: Market orders focus on speed over price, unlike limit orders. This makes them vulnerable to slippage.

How Volatility and Liquidity Affect Slippage

Slippage increases during periods of high volatility and low liquidity. Here’s how these two factors affect it:

Volatility:

- Rapid price movements: Highly volatile markets see prices change in seconds between the moment an order is placed and when it executes. This may lead to higher slippage.

- Events and major news: Key economic announcements or updates may trigger significant volatility, increasing the risk of considerable slippage.

- Quick market execution: In fast-moving markets, orders are executed in a particular sequence. This allows prices to move even further before your order fully executes.

Liquidity:

- Thin markets: Lower liquidity means fewer participants on the opposite side of the trade. It may lead to delays that enhance slippage.

- Large orders: More liquidity is required for large orders to be filled at a single price. However, in low-liquidity environments, large orders simply walk the book, i.e., execute at progressively worsening prices.

- Bid-ask spread: Low liquidity often leads to wider bid-ask spreads, thereby increasing slippage costs when using market orders.

Market Orders, Limit Orders, and Slippage

Here’s looking at these vital concepts in more detail below:

Market Orders

Used for speed to guarantee that a trade fills immediately. The only drawback here is the absence of any price control. This means that you may buy higher or sell lower than expected in fast-moving markets.

Limit Orders

They are used to control costs by setting a specific price limit. A buy limit will execute at this price or lower, while a sell limit will execute at this price or higher. This prevents any negative slippage but does not guarantee execution.

Slippage

It is the difference between the expected price of a trade and the actual price at which it is filled.

Slippage in Stocks vs F&O vs Forex/crypto

Let us look at a brief comparison of slippage for these asset classes.

|

Asset Class |

Usual Slippage Level |

Main Cause |

Key Attributes |

|

Stocks |

Low (Large Cap) |

Market opening/closing, low volume, news |

High liquidity lowers impact and hence large-cap stocks have lower slippage than their small-cap counterparts |

|

F&O |

Low to Medium |

High volatility for options, lower liquidity |

Option slippage is more than future slippage, particularly for illiquid strikes |

|

Forex |

Low (Majors) to High (Exotics) |

Low liquidity pairs, key news events |

High volatility pairs may lead to higher slippage, while majors are usually tight |

|

Crypto |

High (Altcoins) |

Extremely high volatility, shallow order books, and a 24/7 market |

Small-cap tokens may have high slippage. Also, DEXs or decentralised exchanges may often have higher slippage in comparison to CEXs (centralised exchanges) |

So, as you can see, highly liquid stocks have narrow spreads, thereby leading to minimal slippage. Futures are highly liquid, although options (especially far-month or out-of-the-money contracts) may witness considerable slippage due to wider bid-ask spreads.

Large orders may also eat into the order book, triggering slippage. The Forex market is also highly liquid, thereby keeping slippage low for major pairs.

However, it may rise during high-volatility events, such as central bank announcements, or for less-traded exotic currency pairs.

Cryptocurrency is extremely volatile and can lead to high slippage, with slippage exceeding 5% on small-cap tokens during periods of volatility. Smaller CEXs or DEX liquidity pools lack the depth of a traditional market, thereby sparking significant price movements from large orders.

How Slippage Changes Actual Profit and Loss

Slippage may change actual profit and loss by creating a discrepancy between the expected entry/exit price and the actual execution price of a trade. Here’s how it changes the actual P&L:

- Lowering Profit (Negative Slippage)

When buying, the asset will be bought at a higher price than anticipated, thereby lowering potential profits. When selling, it is sold at a lower price than anticipated, thereby reducing the profits. - Amplifying Losses (Negative Slippage)

If a stop-loss gets triggered during rapid drops in prices (market gaps), the position ay close at a much lower price than desired. This may lead to a larger loss than planned. - P&L Improvements (Positive Slippage)

The trade may sometimes execute at a better price than anticipated, thereby reducing losses or enhancing profits. - Eroding High-Frequency Margins

For scalpers and high-frequency traders, small slippage amounts on multiple trades may technically eat into the thin margins (per trade).

How to Reduce Slippage

Here are some strategies that traders can follow to reduce slippage:

- Using Limit Orders

In place of market orders, you can consider using limit orders to set the exact prices (or even better) at which you are willing to sell/buy. This ensures you will never pay more than you expect. However, it can sometimes lead to missed opportunities during quick price movements. - Trading Liquid Securities

Always focus on securities with higher trading volumes and narrow bid-ask spreads, i.e., major currency pairs and large-cap stocks. This is because they are less likely to witness sharp price gaps. - Bypass High-Volatility Periods

Reduce or stop trading during any highly volatile periods, i.e. the market open/close, key economic announcements, earnings report releases, etc. These periods may otherwise witness swift price fluctuations and wider spreads. - Use Quicker Execution Tools

Aim to leverage stable, fast internet connections with trading tools such as a VPS (Virtual Private Server). This helps lower latency between placing the order and its final execution. - Break Up Big Orders

In case you’re trading large positions, break them into smaller orders. This will help you avoid exhausting the available liquidity at a specific price level. - Use Stop-Limit Orders

In case of stop-losses, you may consider using stop-limit orders. They guarantee a specific exit price, unlike stop-market orders, which may fill at any price.

Slippage vs Bid-Ask Spread

The bid-ask spread is the visible and constant cost of trading, i.e. the difference between the highest buy and lowest sell prices. On the other hand, slippage is the difference between the expected price and the actual execution price, resulting from low liquidity or high market volatility. While both increase the costs of trading, the spreads are always known upfront, while slippage remains hidden.

Here are their key differences below:

|

Key Aspect |

Bid-Ask Spread |

Slippage |

|

Cost Type |

Fixed, known, and transactional |

Hidden and variable |

|

Timing |

Visible before trading |

Known only after execution |

|

Causes |

Liquidity provider demand and market structure |

Low liquidity and high volatility |

|

Control |

Cannot be avoided |

May be minimised with limit orders |

So, basically, the spread is the cost of entering the market, while slippage is the penalty for entering at the wrong time or with too much volume.