Floating Shares Explained: Meaning, Formula & Uses

Key Takeaways:

- Floating shares are the shares of a listed company available for public trading on stock exchanges. In India, Category B Public shareholding in a company’s shareholding pattern is often used as a proxy for public float.

- Low float stocks have fewer tradable shares, while high float stocks have over 100 million tradable shares.

- Low-float stocks tend to be more volatile because a smaller tradable supply can amplify buying and selling pressure. They may offer sharp price movement, but they also carry higher liquidity, slippage, and manipulation risk

- High-float stocks usually have better liquidity and more stable price discovery, but they can still be volatile during major news, earnings shocks, sector sell-offs, or index-related flows.

"Floating shares," or "float," refers to a company’s shares that are publicly available for trading (buy/sell) on the stock exchanges. In short, it is referred to as the "tradeable pool" of a stock.

The float excludes shares held by company insiders, promoters, or otherwise locked up and restricted from trading.

How Floating Shares Are Calculated

The following formula is used to calculate floating shares:

|

Floating Shares: (Outstanding Shares) - (Promoter & Promoter Group) - (Non-Promoter/Non-Public if any) |

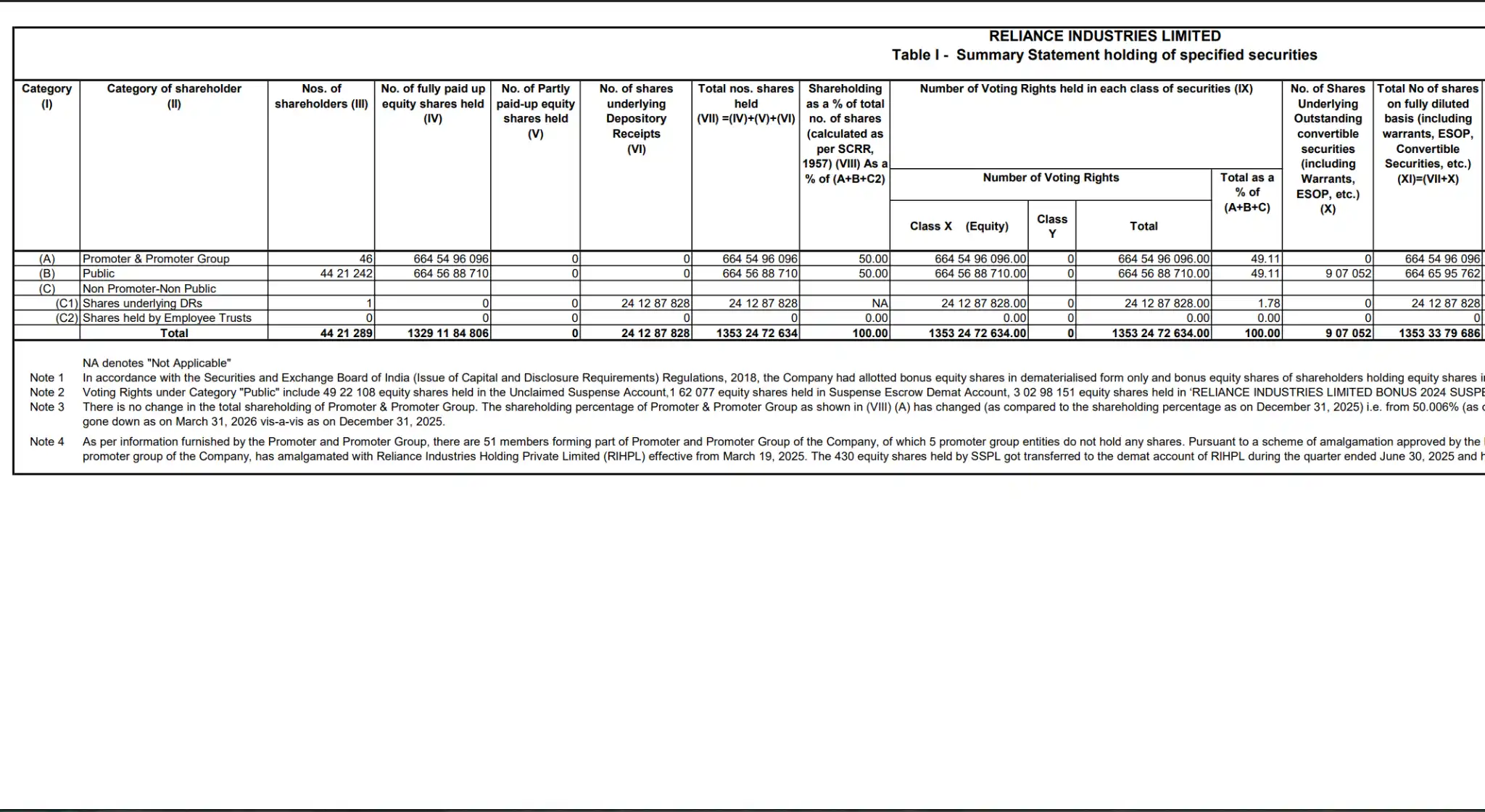

Now, let’s take Reliance Industries as an example to understand how “Float” is calculated.

[Source: Reliance Industries Shareholding Pattern filed with BSE and NSE as on March 31, 2026]

- Total Outstanding Shares: 1353,24,72,634

- Promoter & Promoter Group [Restricted / Not Freely Tradeable]

- 664,54,96,096 shares, i.e., 50.00% of total outstanding shares.

- Non-Promoter, Non-Public [DRs, also excluded from float]

- 24,12,87,828 shares, i.e., 1.78%

Float Calculation

|

Component |

Shares |

Percentage (%) |

|

Total outstanding shares |

1353,24,72,634 |

100.00% |

|

Less: Promoter & Promoter Group |

664,54,96,096 |

50.00% |

|

Less: GDR / Depository Receipts |

24,12,87,828 |

1.78% |

|

Public Float |

664,56,88,710 |

~48.22% |

|

Float and Float (%) = ~66.46 crore shares, or approximately 48.22% of total outstanding shares. |

||

Free Float Market Capitalisation

Total market cap of a company is calculated using: Share Price × Total Outstanding Shares

However, this number also includes shares that are locked by promoters and cannot be traded. Major indices, including Nifty 50 and Sensex, do not use total market cap. They use free float market cap so that index weights are based only on shares that are freely available for trading.

Free Float Market Cap = Share Price × Floating Shares

For instance,

|

Metric |

Company XYZ |

|

Share Price |

₹100 |

|

Outstanding Shares |

100 crore |

|

Floating Shares |

40 crore |

|

Total Market Cap |

₹10,000 crore |

|

Free Float Market Cap |

₹4,000 crore |

Applying the free-float market-cap formula to Reliance Industries.

Considering the share closing price as of March 31, 2026, ≈ ₹1,282

|

Metric |

Calculation |

Value |

|

Total Market Cap |

₹1,282 × 1353,24,72,634 shares |

~₹17.35 lakh crore |

|

Free Float Market Cap |

₹1,282 × 664,56,88,710 shares |

~₹8.52 lakh crore |

Reliance's actual index weight is calculated on ₹8.52 lakh crore, not ₹17.35 lakh crore, because half the company is locked with promoters and not accessible to the market.

When a stock gets added to or removed from the Nifty 50 or other indexes, index funds tracking those benchmarks must buy or sell that stock. The quantity they trade is driven by the free-float market cap, not the total market cap.

This is why index inclusion events can trigger sharp price moves, especially in low-float stocks, where even modest index-driven buying hits a thin, tradable pool and moves the price disproportionately.

Outstanding Shares vs Floating Shares

Outstanding shares and floating shares are often confused and used interchangeably, but they represent very different things. Here’s how they differ.

|

Parameter |

Outstanding Shares |

Floating Shares |

|

Definition |

Total number of shares issued by the company. For instance, in the Reliance Industries case, it was 135.32 crore shares |

Shares available for public trading |

|

Includes insider holdings |

Yes |

No |

|

Includes restricted shares |

Yes |

No |

|

Used for |

EPS, market cap calculations |

Liquidity and trading analysis |

Low Float vs High Float Stocks

Broadly, a stock falls into two categories:

- Low Float

- A stock is generally considered low float when it has fewer tradeable shares (threshold varies by market cap).

- These are usually highly volatile; even small buy/sell orders can move the stock price significantly

- Low float stocks can be easily manipulated. Sudden spikes can reverse just as fast.

- Often seen in small-cap and mid-cap companies

- High Float:

- Stocks with larger freely tradable shares are considered high float.

- Their volatility is generally low, which provides greater stability and predictability

- Common among blue-chip and large-cap companies

Why Low-Float Stocks Can Experience Short Squeezes

A low-float stock attracts heavy short-selling. Traders bet against it because it looks overvalued, has weak fundamentals, or has simply run up too far too fast. Since the float is small, a large percentage of the available shares are now borrowed and sold short.

A piece of positive news arrives: earnings, a product announcement, a large investor disclosing a stake, or even a viral social media post. Buyers start rushing in.

Short sellers now need to buy back shares to close their positions and limit their losses. But they are trying to buy in a market that already has very few shares available; the float is thin. Every short seller buying to cover competes with new buyers entering the market on positive news. Demand explodes against a fixed, tiny supply. The price rockets upward.

As the price rises, more short sellers face margin calls and are forced to cover regardless of their view. This forces more buying, pushing the price higher and forcing more covering. The squeeze feeds itself.

Why Float Matters In Trading

Low-float stocks can cause explosive market rallies.

Let’s say a company has announced its earnings, and the results are extraordinary. This could trigger a sudden buying spree.

Many traders rush in, but only a limited number of shares are available.

Result: Price can jump 10%, 20%, or even hit upper circuits repeatedly.

Low float also increases downside risk

The same mechanism works in reverse.

When bad news arrives:

Everyone wants to sell. Very few buyers are available. So, price can collapse quickly.

Entry and exit ease, as high-float stocks are harder to manipulate

In high-float stocks, getting in and out of positions is much easier without disrupting prices.

Float and Liquidity

Liquidity refers to how easily a stock can be bought and sold on the stock exchanges.

Float and liquidity are directly proportional.

- High Float (↑) = High Liquidity (↑)

- Low Float (↓) = Low Liquidity (↓)

For long-term investors, low liquidity is a real concern. You might buy into a low-float stock easily, but exiting a large position when sentiment turns could be difficult.

Higher float usually improves liquidity because more shares are available for trading.

However, please note that float is only the supply base.

Actual liquidity depends on trading volume, trading value, bid-ask spread, market depth, and investor interest.

Float and volatility

Float and volatility usually have an inverse relationship. But it's not always true. Low float can amplify price moves, but high-float stocks can still be volatile during earnings announcements, macro events, etc.

The lower the float, the higher the potential volatility. Here's why.

With fewer shares available, any imbalance between buyers and sellers has an outsized effect on price. A sudden surge in buying interest against a small float means there aren't enough sellers to absorb demand at the current price, so the price has to move up to find them.

- In India, daily movement is constrained by exchange-imposed price bands or circuit filters. This is why low-float stocks hit repeated upper or lower circuits rather than doubling freely in a single trading session.

- The same stocks can collapse just as fast on negative sentiment

- Penny stocks and micro-caps, which typically have low floats, see extreme intraday swings.

How Promoters, Insiders, & Locked-in Shares Affect Float

The composition of a company's shareholder base directly determines the stock’s float size.

Promoter Holdings

In India, promoter holdings are disclosed quarterly, as mandated by the Securities and Exchange Board of India (SEBI).

A company where promoters hold 70–75% of shares automatically has a very limited public float; only 25–30% of shares are available for trading. High promoter holding is often seen as a sign of confidence in the business, but it also means the stock can be highly volatile due to limited supply.

Insider Holdings

Insider-held shares are not automatically locked at all times. Some shares may be locked due to IPO, ESOP, contractual, or regulatory restrictions.

Separately, insiders and designated persons are subject to SEBI's insider trading rules and trading window restrictions. Post-IPO lock-in periods (usually 6–12 months) keep these shares off the market entirely. Once lock-ins expire, the float can expand significantly, which is why “lock-in expiry” dates are closely tracked by traders.