Why Trading Strategies Stop Working When They Get Crowded

A lot of times, traders can, after extensive testing, develop a strategy with good metrics. It has a good risk-to-reward ratio and high accuracy, and it has delivered good returns in the past. However, it is sometimes observed that when this strategy becomes crowded, its edge begins to fade. A strategy becomes crowded when a large number of traders enter the same trades at the same time, using the same logic and on the same instrument.

When the strategy is overcrowded, it leads to changes in market microstructure, eroding its original edge. This overcrowding can happen to equities, futures, and especially options strategies. One of the most commonly cited examples in Indian markets is the 920 Straddle.

The 920 Straddle - What It Was

This is a very popular strategy in which the ATM straddle is shorted at 9:20 AM daily. The reason this is done is that traders observed:

- Post-opening volatility settles around 9:20 AM

- Implied volatility drops

- Premiums decay steadily

- The market often remained range-bound intraday

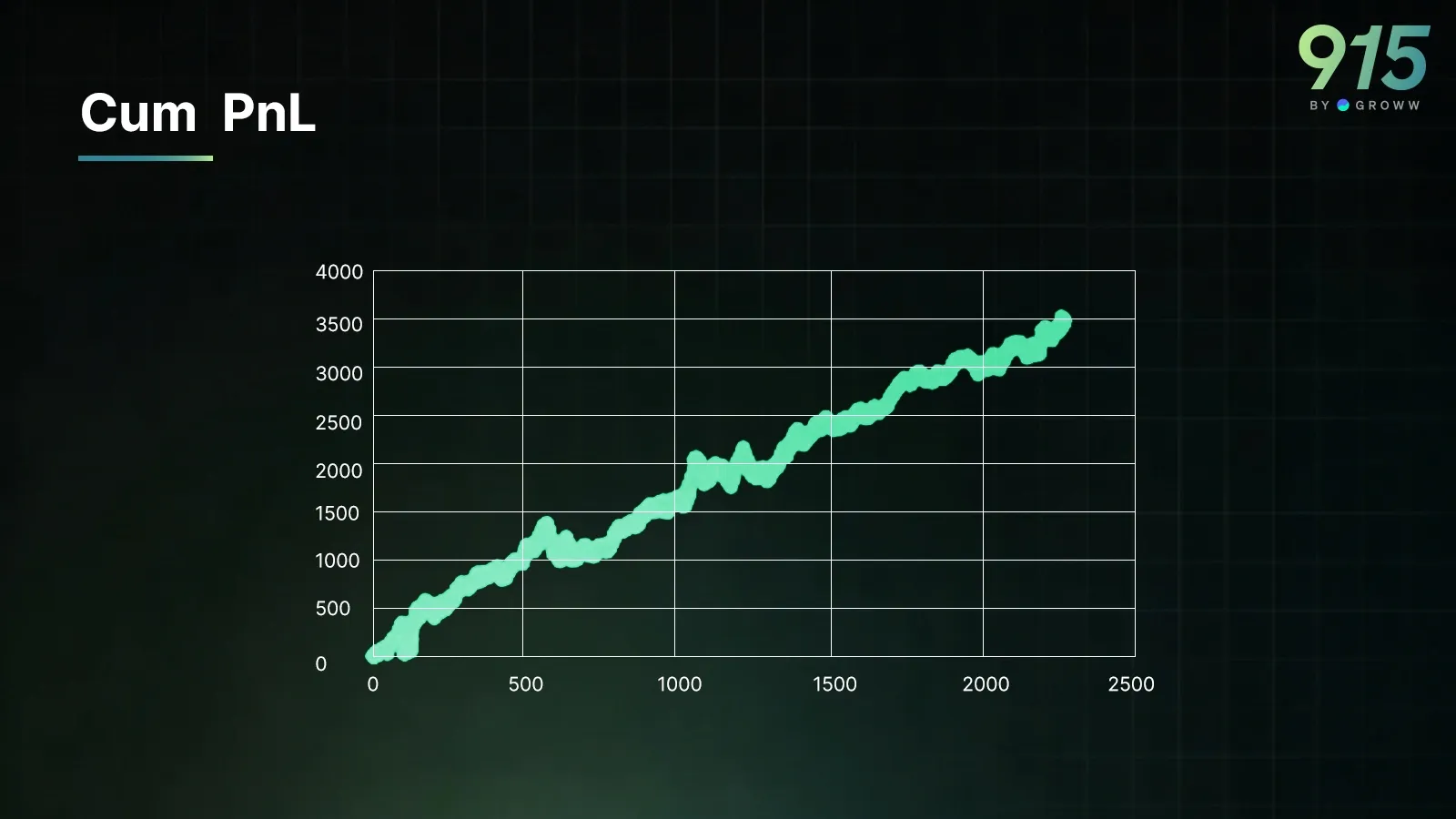

Here are the results of the strategy from 1 Jan 2020 to 30 Jul 2024

Some metrics during this time:

The total P&L during this time was 3,400 points. This spans 4.5 years, and the total number of trades was around 2,260. This means that the profit per trade was around 1.5 points. The accuracy was about 38%, and the strategy's maximum drawdown was around 387 points.

The results were definitely looking very promising:

- High win-rate

- Smooth theta decay

- Manageable gamma risk (before expiry day)

- Low realised volatility relative to implied

For many traders, this became a “daily income strategy”.

Also check : Scalper Mode on 915 | Straddle Chart

Why It Worked in the Beginning

Some of the reasons why the strategy was working were:

- Orderflow Was Thin: The strategy was relatively unknown. Few traders were crowding the same strike at the same time.

- IV Was Often Rich Relative to RV: The Nifty options enjoyed higher Implied volatility than realised volatility intraday.

- Gamma Was Manageable: Another important factor was that the market moved less intraday compared to premiums.

Together, these conditions created a short vol edge.

Then the Strategy Became Popular

However, the strategy became increasingly popular. One of the reasons was that the strategy was very easy to understand and could be initiated both manually and using algo. Over time:

- YouTube channels promoted it

- Gurus sold workshops on it

- Discord/Telegram groups shared signals

- Broker APIs made execution trivial

- Capital scaled (pro desks + retail)

- Algo shops began auto-executing it

And thousands of traders began selling ATM straddles at 9:20 AM daily. And suddenly the results changed!

The First Principle: Crowded Strategies Lose Edge

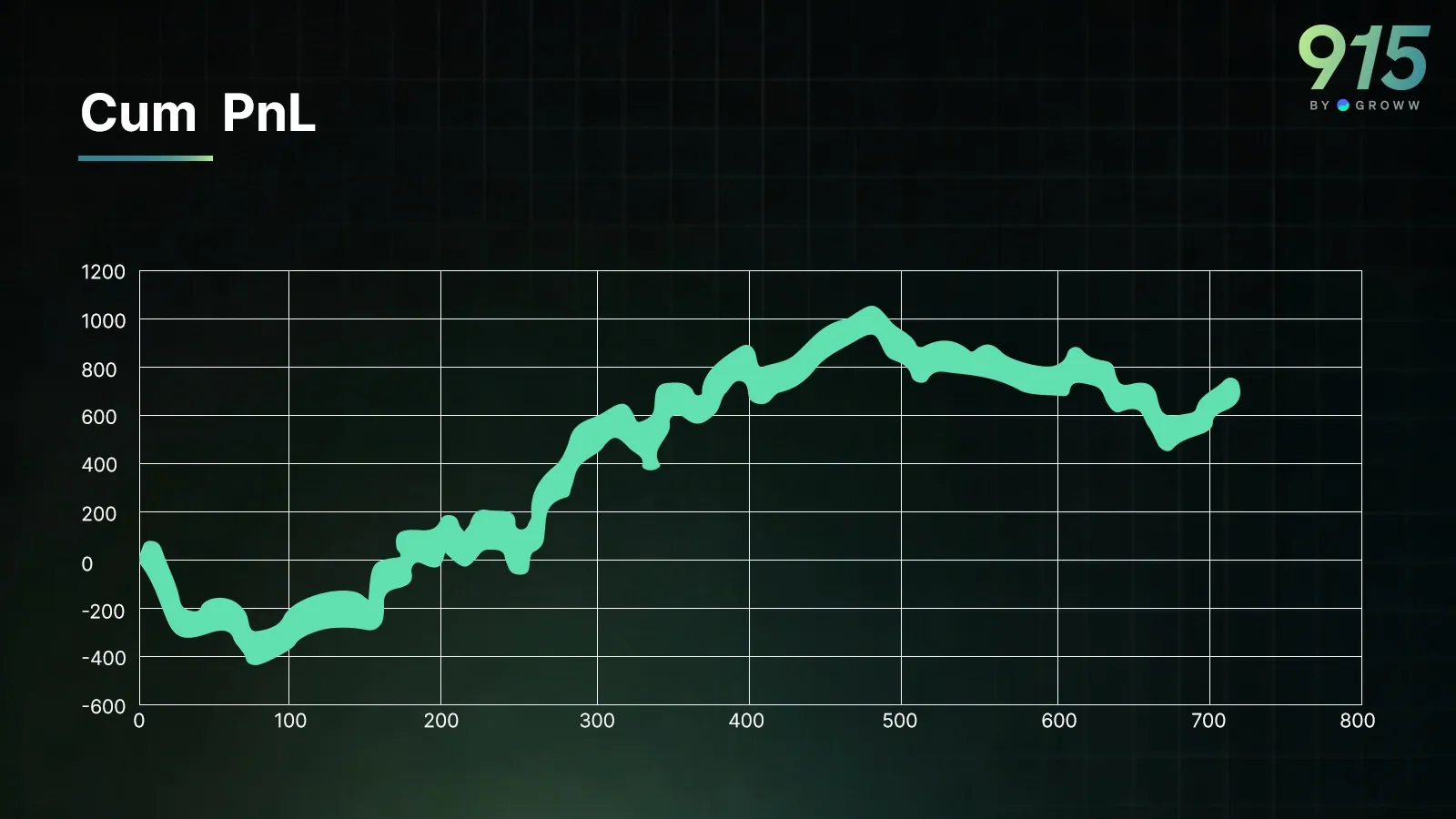

Here are the results of the strategy post Jul 2024.

Over the past 1.5 years, total profit has been just 673 points, with 0.9 points per trade. The accuracy has reduced to 36%, and the max drawdown has increased to 520 points. The strategy does not seem profitable after adding all costs, including brokerage, stt, and other exchange costs.

How Crowding Erodes Strategy Performance

It is a good case study to see why the strategy lost its edge.

- Liquidity Distortion: The strategy was known as the “920 Straddle”, and everyone was selling the same strike at 9:20 AM. This led to premium compressing faster, the IV dropping instantly, and high slippage for traders.

- Bad Trade Location

Since many traders were trading at the same level, it led to a poor average entry price. The Greek exposure was uniform across traders, and traders used to get trapped together in the case of any adverse moves

- Broker + Exchange Infrastructure Stress

Moreover, during the same period, algorithmic trading in India was booming, leading to API bursts and execution slippage. There were margin spikes and a delay in fills. Overall, the microstructure issues destroy the edge, even if the thesis is correct.

- Adverse Selection from Smart Money

A major issue was that smart money, other hedge funds, and liquidity providers were able to take advantage of the strategy by being on the opposite side of the trade. When all retail traders are willing to take the entry at 9:20, it is easy for the smart money to push option prices lower and buy at lower levels. This flips the edge in favour of crowded participants.

- Risk-Reward Shifts

The strategy was originally lucrative because premiums were high and the risk was low. However, overcrowding, premiums compressed, and risks increased. This led to a lopsided risk-to-reward ratio.

Overall, all the above changes led to traders seeing:

- There were frequent directional moves post 10 AM, which led to stoplosses being hit

- The amount of theta decay was insufficient to cover moves

- A lot of days, especially on expiry, had volatility shocks

- Many trades were not filled at good prices due to thin premiums

What is worse is that many traders who had tasted success in the past increased their position sizing. But the system stopped performing well, leading to blowups.

Conclusion

Trading strategies take time to develop. They are created after thorough testing. However, sometimes a working strategy stops working. This is not by bad luck or magic. They stop working because markets adapt to capital flows.

We saw why the very popular 920 Straddle became ineffective: it became too popular, leading everyone to trade it. There was a clear shift in the volatility regime, and the crowding kills the edge. In trading, survival depends on recognising what the actual edge is and when it disappears.