What Is Delta Neutral Trading in Options?

There are two kinds of trading strategies: directional and non-directional. In directional strategies, traders aim to predict the direction and take an entry. This is usually done by trading the breakouts. A lot of reversal trading is also part of directional strategies. When a trader goes for a reversal trade at a support or resistance level, that is also a directional strategy. Essentially, in a directional strategy, the trader bets on the direction and takes a single-direction trade. In the case of stocks for futures, this will be a direct buy or sell trade. In the case of options, the trader might go for naked call buying or put buying. The trader can also go for spreads if he wants to have a risk-defined system.

In non-directional strategies, the trader is not predicting a direction and hence uses delta-neutral strategies. Some delta-neutral strategy examples include straddles, strangles, and iron condors. Traders like this kind of strategy because they do not have to predict the direction, which is probably the hardest thing in the market

But in reality, most non-directional trades are not truly neutral when they are initiated. They still carry delta exposure, which means the position can start behaving like a directional trade if the market moves. This is where delta-neutral trading becomes important. It is very important for traders to keep the overall strategy balanced so that they can not only benefit from theta but also avoid being penalised for Delta movement. Hence, it is important to understand the concepts of delta hedging and balancing to achieve consistency in non-directional option trading.

What Is Delta?

Delta measures how much the option price changes for each one-point change in the underlying price.

For example, if the ATM Call options delta is 0.5 and the trader expects Nifty to move by 100 points, then the ATM option is expected to move by 50 points. Hence, the calculation is following:

Expected movement in the option = Delta * underlying movement

In other words, we can also say that Delta represents the direction of exposure. If the overall Delta is high, the option or the entire strategy will move faster in that particular direction. It will have a stronger directional sensitivity.

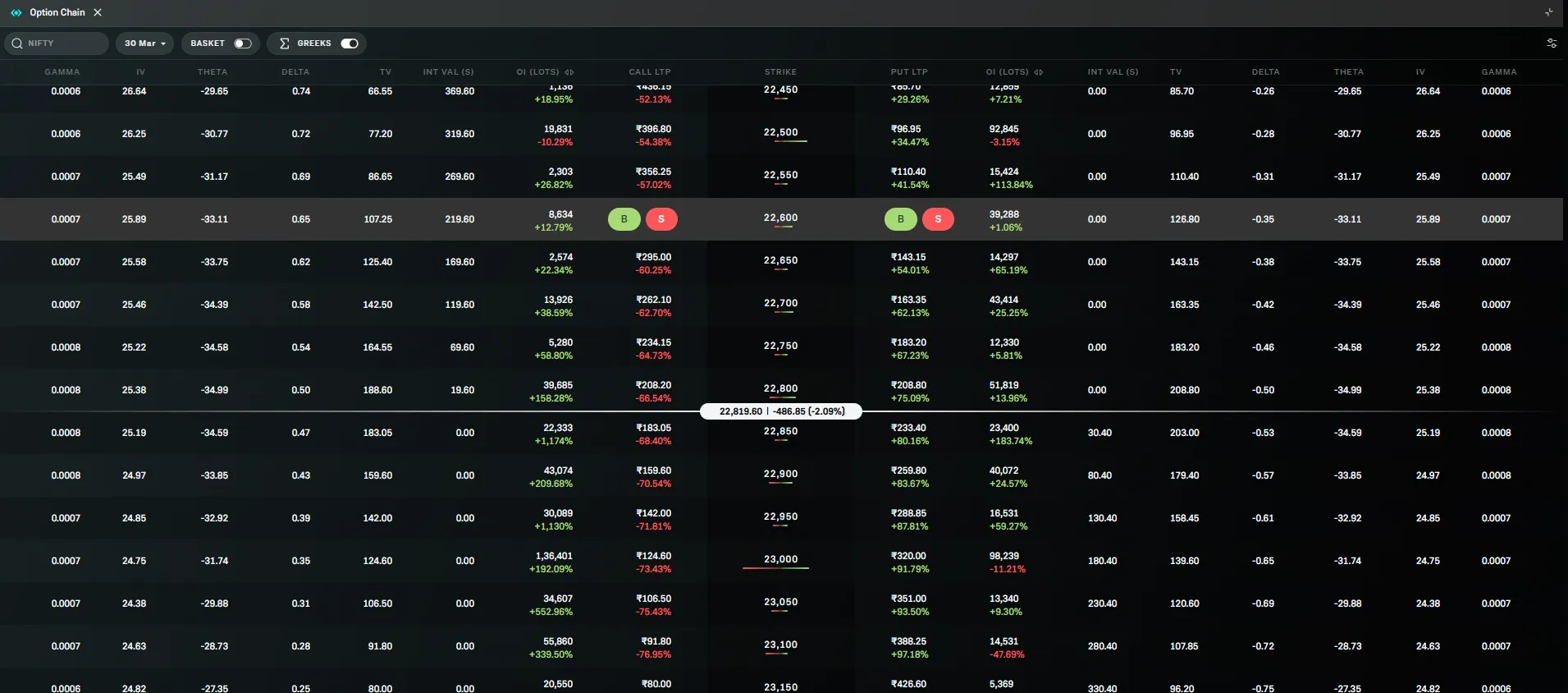

ITM options have high delta and therefore move almost in sync with the underlying, whereas OTM options have low delta and therefore move more slowly. Here are the different values for different strikes:

What Does Delta Neutral Mean?

Delta neutral means that the total strategy has a net exposure of zero. For example, if one position has a delta of +0.4 (that means we have bought an OTM call option) and another position has a delta of -0.04 (that means we have bought an OTM put option), then the net delta of the entire position is 0. This implies that small movements in the underlying price should have minimal impact on overall P&L. The position becomes less sensitive to small price changes. Once this happens, all the trader has to focus on is theta decay, volatility changes and the probability that the market remains range-bound.

The example above is slightly misleading. Usually, when we talk about Delta-neutral strategies, it's about using option writing. So, an actual Delta-neutral position would mean that we are selling an OTM put option with a delta of +0.4 and shorting an OTM call option with a delta of -0.4, thereby giving a net delta of 0 for the entire strategy.

It is usually easy to create delta-neutral strategies to start with. But when the underline moves, the delta for different positions will change differently, and the overall position may have a positive or a negative Delta. In the example we took, if the market starts to go up, we can expect the put option to become more OTM, and hence the delta will decrease to 0.3. On the other hand, the call option shorted will gradually become ATM and hence its delta will be close to -0.5. The overall delta of the position has changed from 0 to -0.2, and hence a downward bias.

Example With Index Near 23,000

Assume the index is trading around 23,000.

You create a short strangle:

Sell 23,300 Call option with delta = -0.2 (2 lots)

Sell 22,700 Put option with delta = 0.2 (2 lots)

At entry, the combined delta may be close to zero.

But if price moves to 23,200:

Call delta increases to -0.4 (2 lots)

Put delta decreases to 0.1 (2 lots)

Net delta becomes -0.3 x 2 = -0.6. Now the position behaves directionally. Risk increases if the price continues moving. Balancing delta helps maintain non-directional exposure.

How Traders Maintain Delta Neutrality

The traders' aim is to ensure that the entire position's delta is close to zero. There are multiple ways a trader can maintain delta neutrality. Delta neutrality is usually maintained through adjustments. Some of the common methods include:

- Adjusting the strike positions: In our previous example in which the deltas become -0.6 a trader can shift the entire position a little up. That means the trader can exit the original 23300 call option and enter the 22700 put option, and take new positions in the 23500 call (sell) and the 22900 put (sell).

- Reducing exposure on one side: In this case, the trader may reduce some positions while adding a few. For example, the trader can exit one of the call positions and short two more lots of put options, thereby making the net Delta zero. The call delta = -0.4 (1 lot) and put delta 0.1 (4 lots) = 0.4

- Using futures to hedge directional exposure: In the event of a very strong directional move, a very good way to maintain Delta neutrality is to take the trade in futures. The Delta of futures is 1 (long) and -1 (short). So, if the net delta of the position is close to -1, the trader can just go long one lot of futures so that the overall delta becomes zero.

Summary

Delta-neutral strategies are highly rewarding because traders are only concerned with the profit they make from theta decay. However, the strategy only works if the movement is small and if the overall position is close to Delta neutral. If the position is not Delta neutral, the trader can incur risk due to directional bias. There are multiple ways a trader can continue to have the position Delta neutral, such as adjusting strike positions and reducing exposure on one side.