Short Vol vs Long Vol in Options Trading

“Vol” refers to volatility, specifically the implied volatility. As we know, implied volatility is the expected future movement of an asset. Trading options essentially means the trader is either short vol or long vol. If the trader expects low realised volatility, he is trading short vol. If the trader is going to benefit from large realised movement, then is he trading long vol? This is the foundational lens through which all option strategies can be understood.

The Two Fundamental Stances in Options

Before talking about strategies, you must understand these two core exposures:

1. Long Volatility (Long Vol)

Long volatility strategies mean a trader who stands to profit if realised volatility exceeds implied volatility. In this case, he is essentially betting that volatility will be higher than the market is predicting. This also means he is likely to buy options to take advantage of the Vega move. So, as a long vol trader, some of the profitable scenarios are:

- Big directional moves

- Breakouts

- Trend expansions

- Volatility spikes

In all the above scenarios, the trader expects a benefit from positive Vega and Gamma.

Also check : Scalper Mode on 915 | Straddle Chart

2. Short Volatility (Short Vol)

In the case of short vol, traders expect realised volatility to be lower than implied volatility. So the kinds of strategies usually involve option-writing strategies. Some of the common themes for short vol traders are the following:

- Low realised movement

- Consolidation

- Mean reversion

- Volatility crush

In this case, the traders stand to benefit from positive Theta and, more importantly, negative Vega.

How Option Strategies Emerge From Volatility Exposure

Here are the strategies traders can deploy if they are long-vol traders. As the traders stand to benefit from movement, and not just direction, some of the best strategies are:

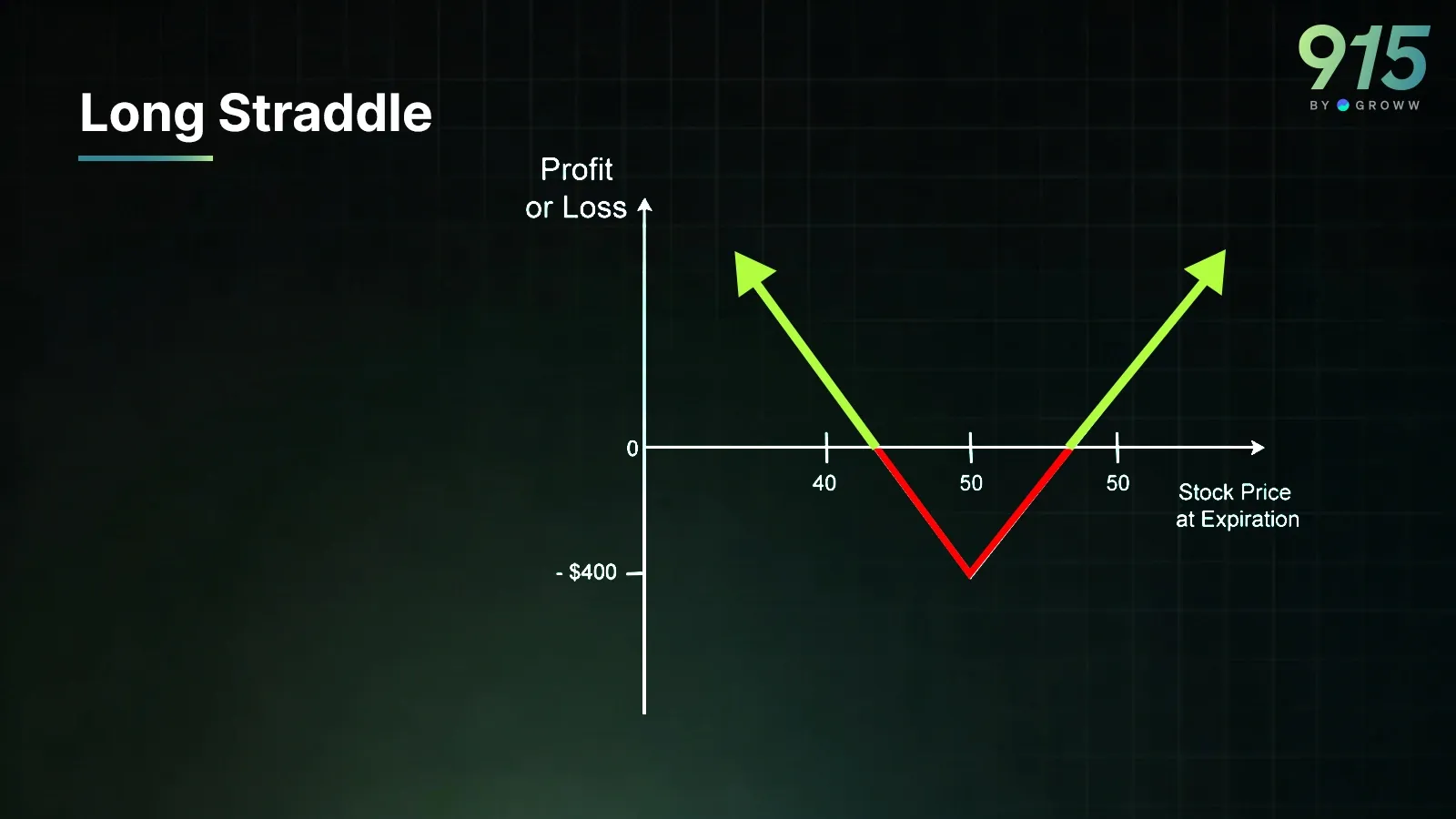

1. Long Straddle

- In this strategy, a trader will take 2 legs: Buy Call + Buy Put (same strike)

- This is a pure long vol play

- The traders will profit if the movement is greater than the premium paid

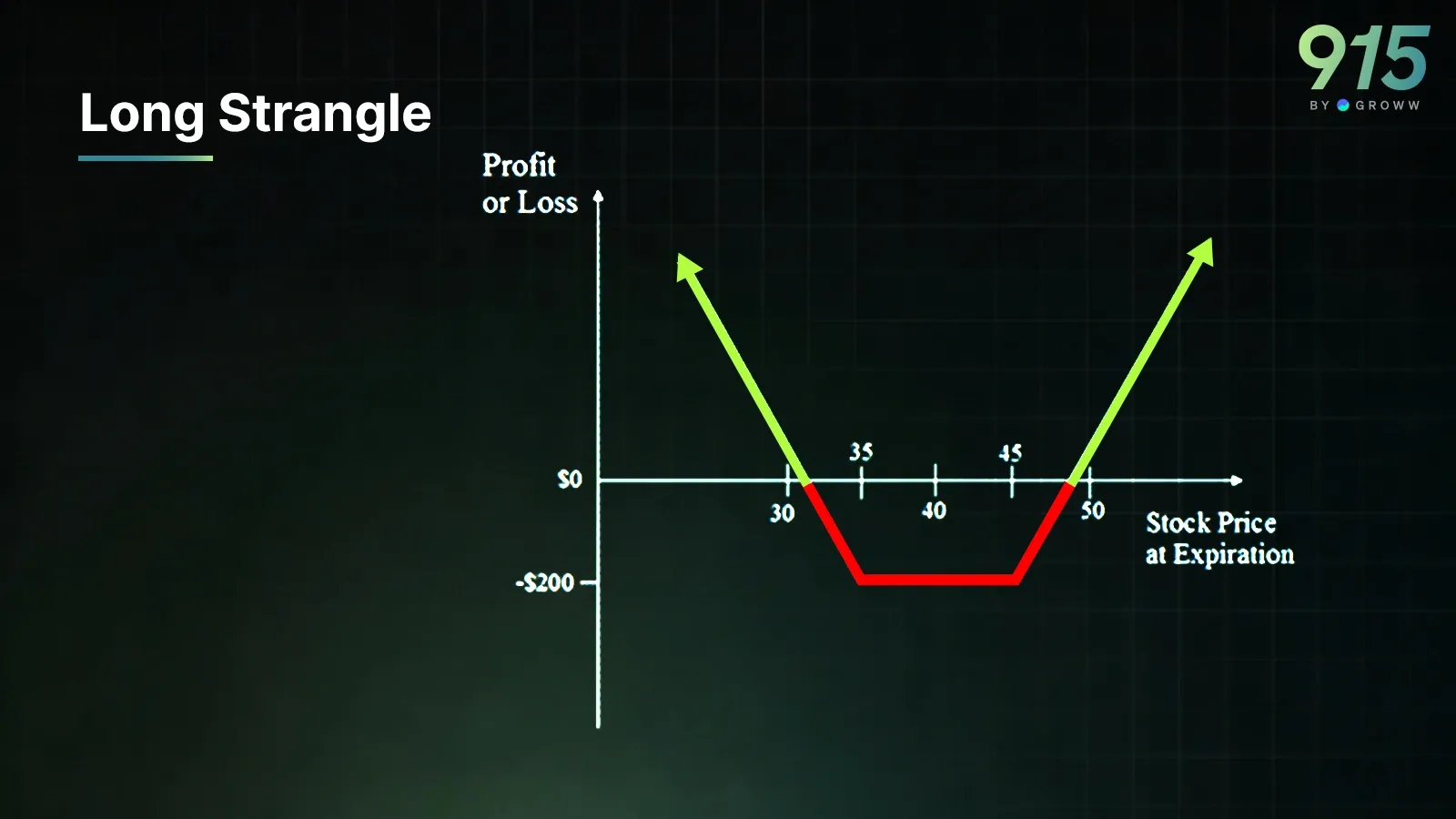

2. Long Strangle

- In this strategy, a trader will take 2 legs: Buy OTM Call + Buy OTM Put

- This is a cheaper alternative to straddling

- But, in this strategy, the traders needs strong move to pay

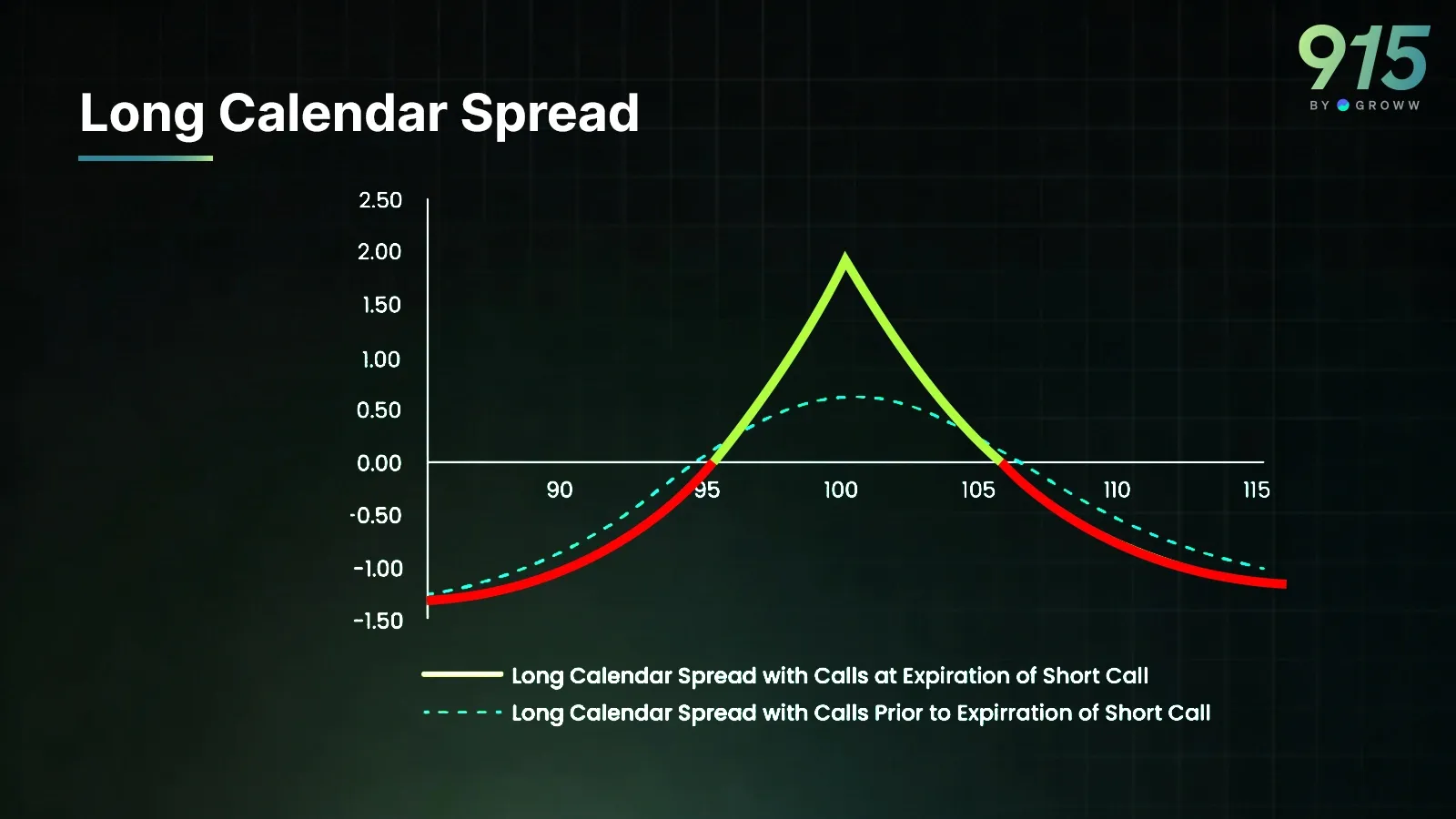

3. Long Calendar Spread (Buying back month, selling front month)

- This is also a long Vega strategy because far-month Vega is more than the near-month Vega

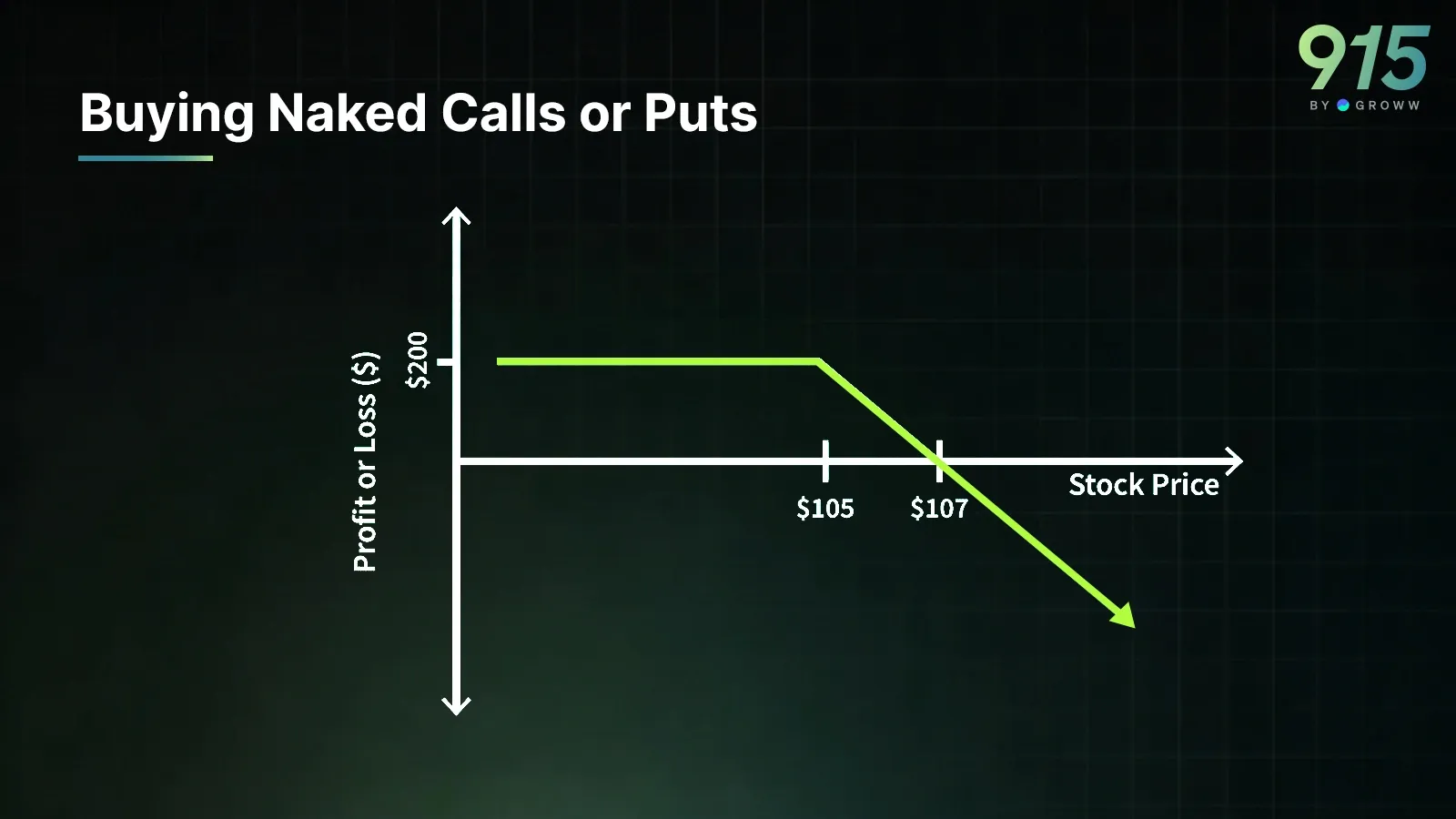

4. Buying Naked Calls or Puts

- This is a simple strategy where the trader is not only betting on long vol exposure, but also on directional bias

The key characteristics of all these strategies are:

- Gamma positive

- Vega positive

- Theta negative

Here are the strategies that the traders can deploy if they are short-vol traders. As the traders stand to benefit when the market does not move, some of the best strategies are:

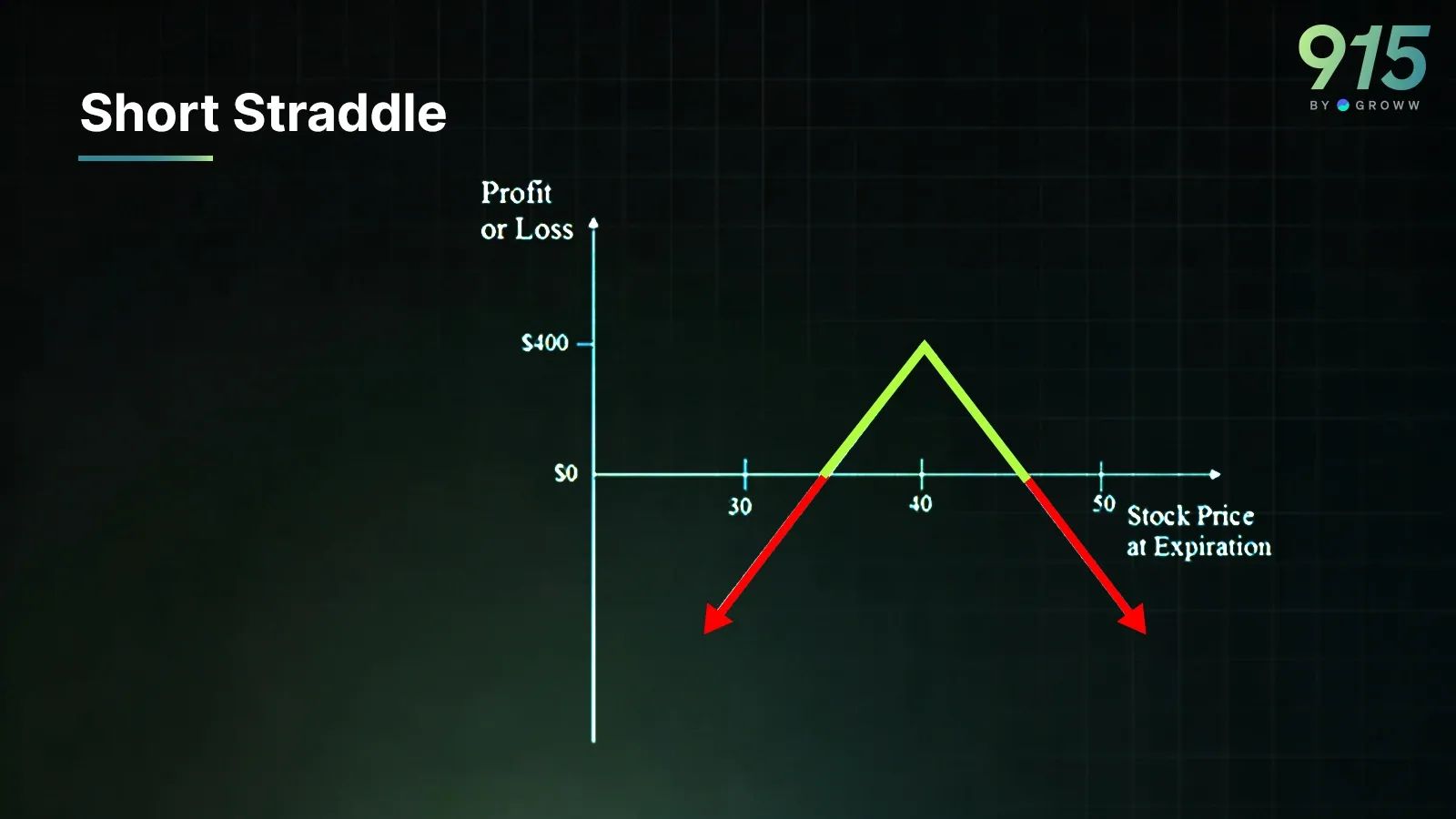

1. Short Straddle

- In this strategy, a trader will take 2 legs: Sell Call + Sell Put (ATM)

- This is the most common short vol strategy.

- The trader stands to benefit most in tight ranges

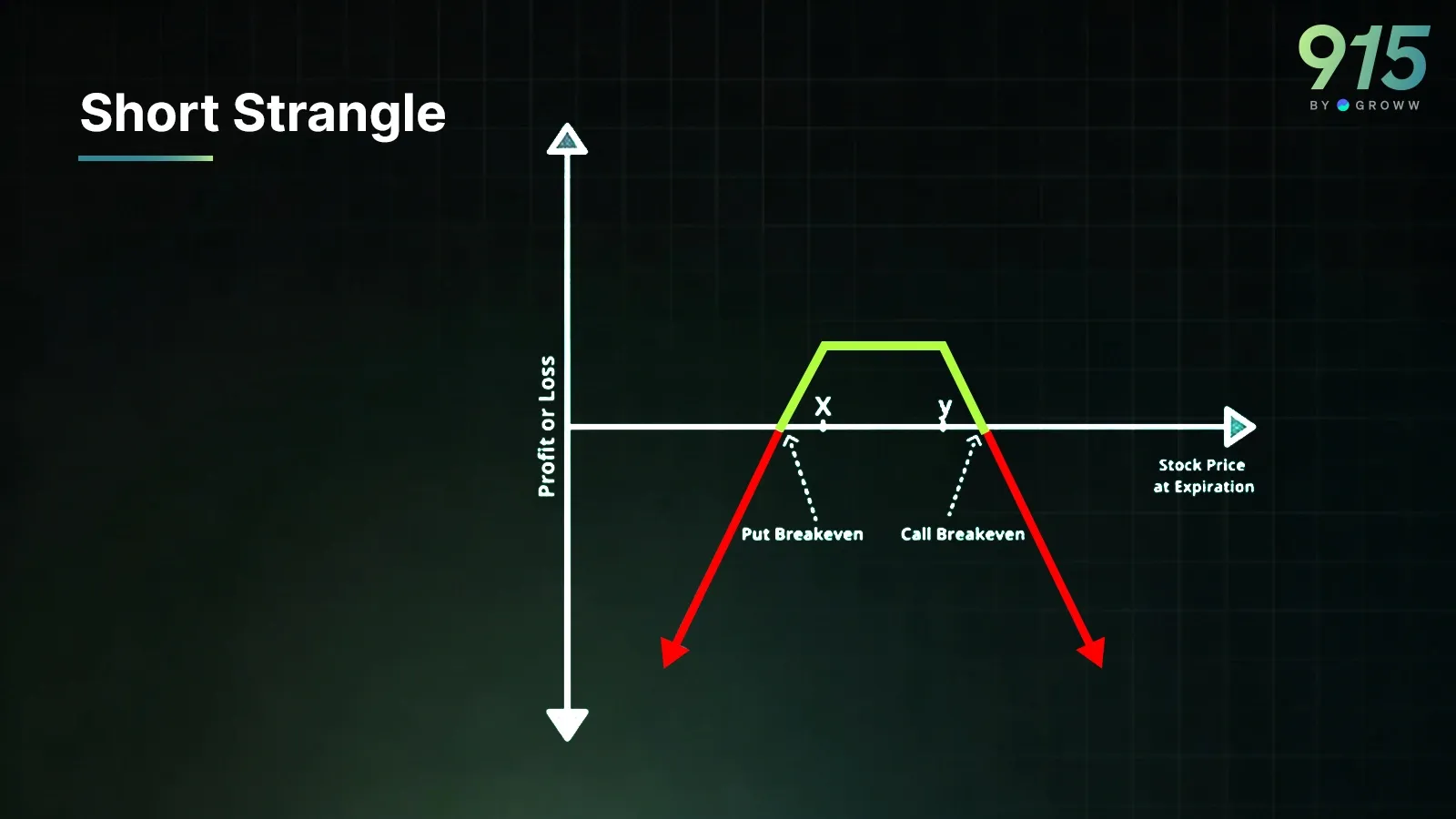

2. Short Strangle

- In this strategy, a trader will take 2 legs: Sell OTM Call + Sell OTM Put

- This strategy has lower risk than a straddle, and a lower premium too

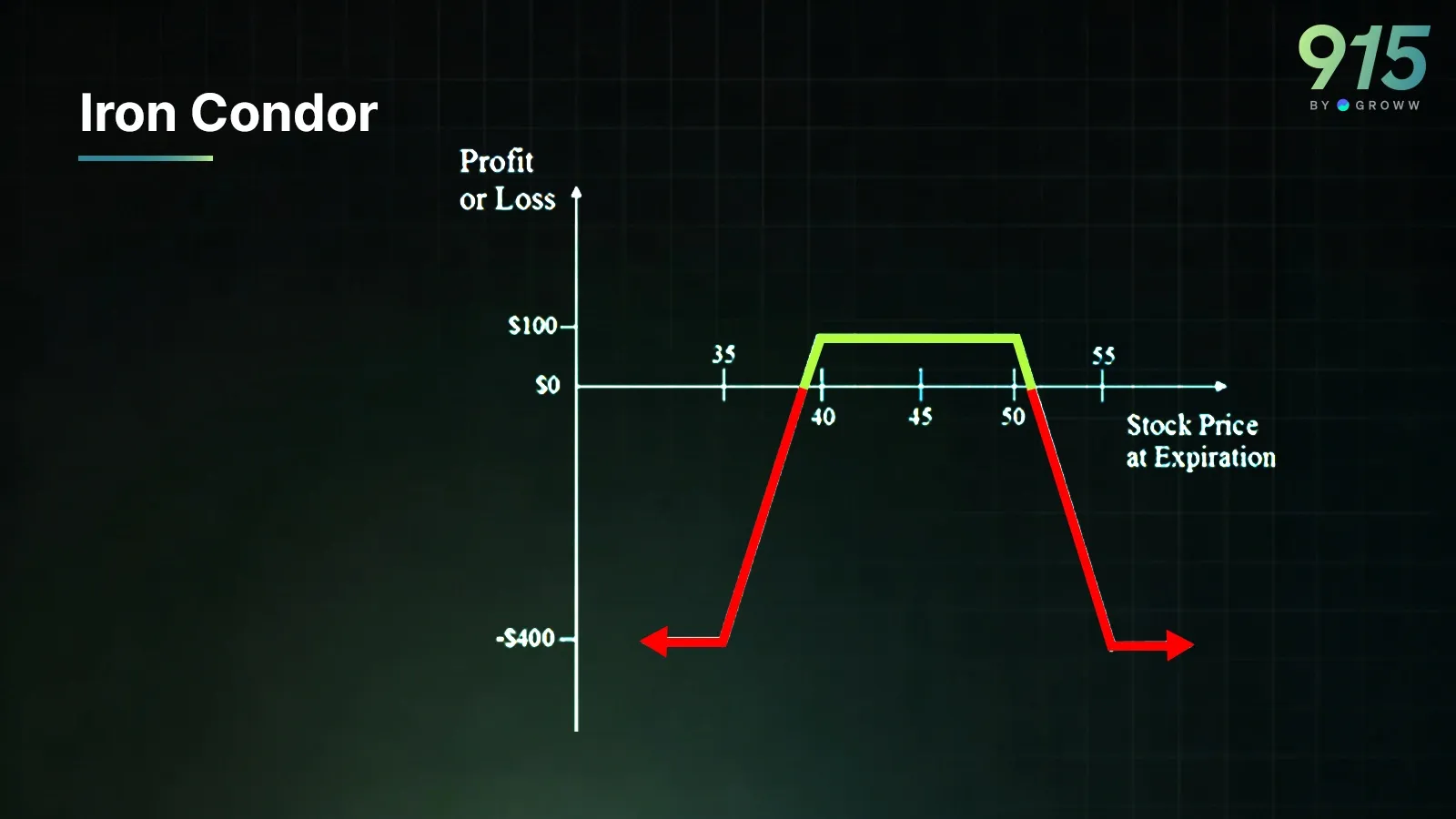

3. Iron Condor

- In this strategy, the trader takes 4 legs: Sell OTM strangle, hedge with further OTM wings

- This is a controlled short vol exposure

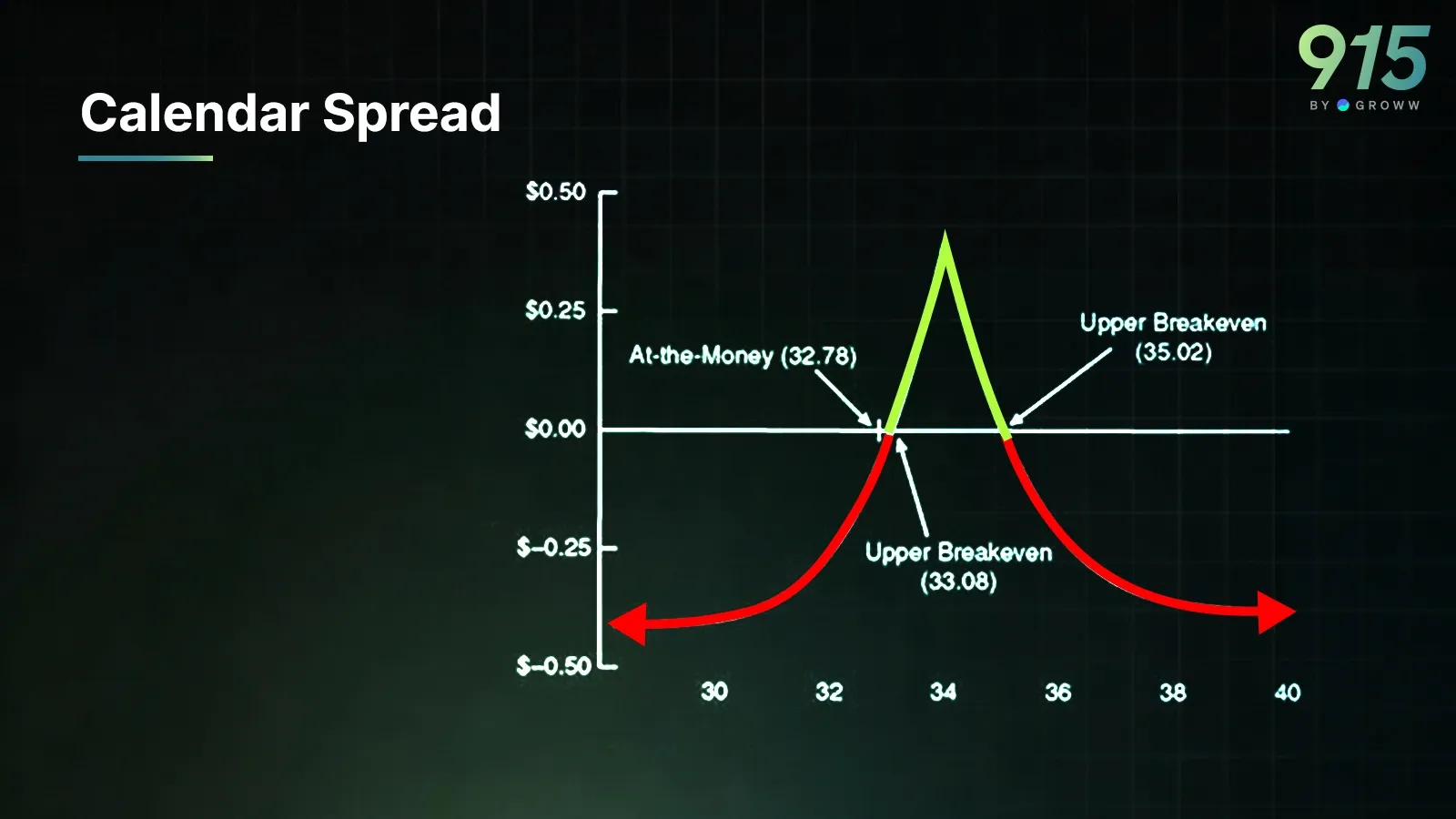

4. Calendar Spread (Selling back month, buying front month)

- This is a relatively less common strategy, which basically flips vega exposure

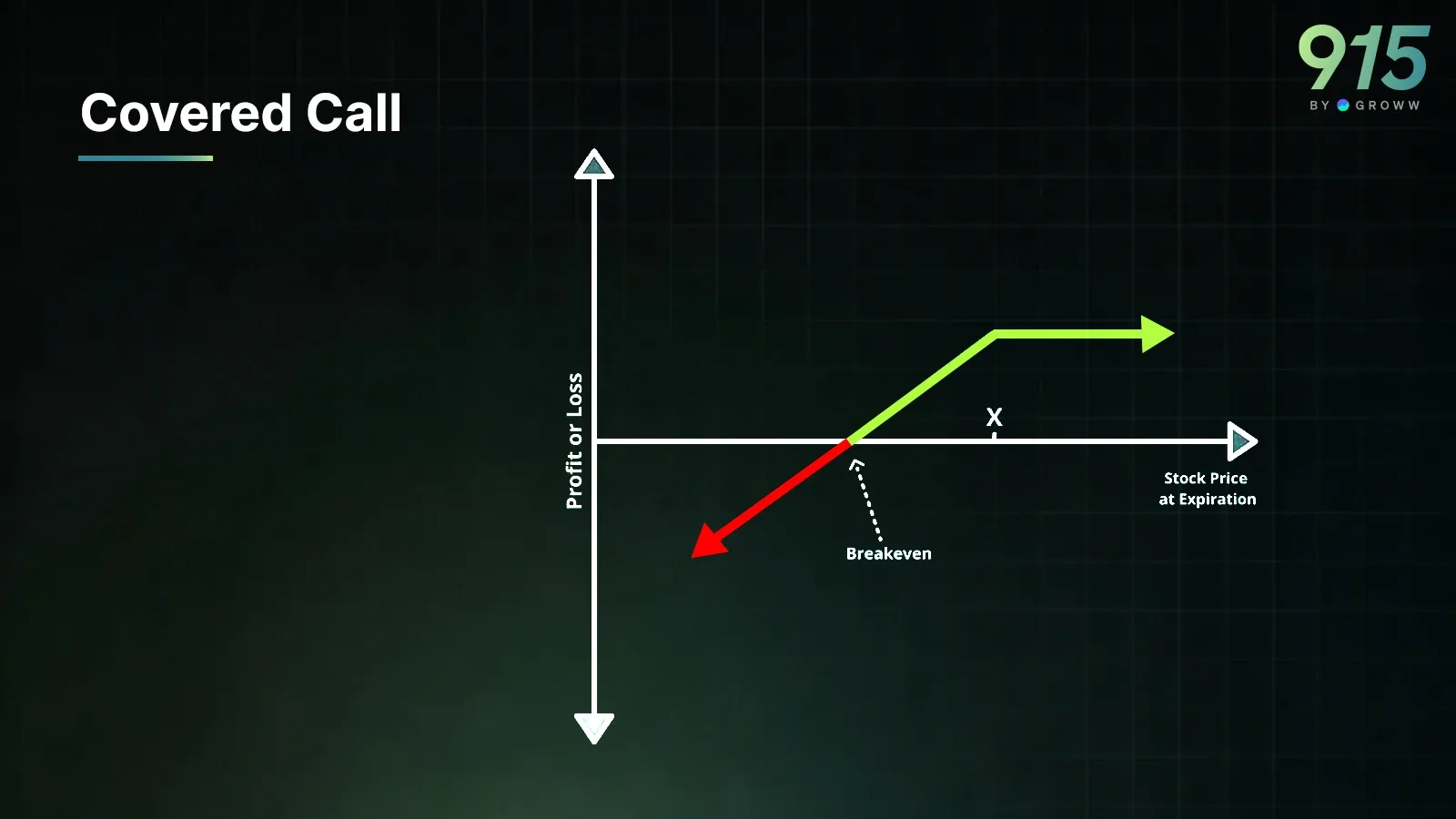

5. Covered Call

- This is also called the rental strategy, where the short call is equal to short vol

- It’s a simple strategy that generates theta income

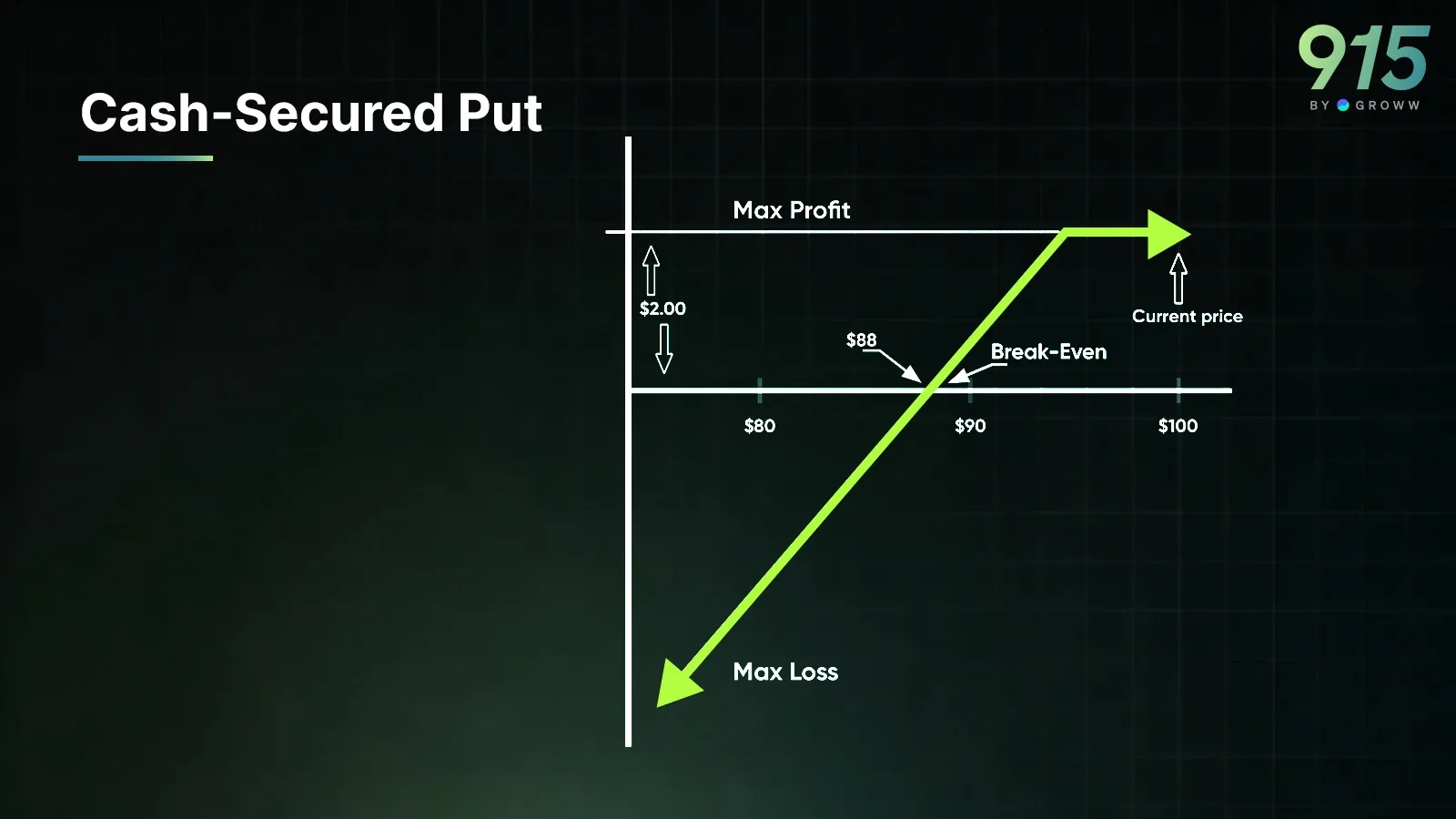

6. Cash-Secured Put

- Similar to above, the selling put is equal to short vol + bullish bias

The key characteristics of all these strategies are:

- Gamma negative

- Vega negative

- Theta positive

Very important to note that most short-vol strategies earn steadily but carry tail risk.

Why This Perspective Matters More Than Indicators

While most trading is done, keeping the direction in mind, volatility is extremely important in options. Professional traders instead ask: “Am I long or short volatility, and what regime am I in?” The answer to this gives them an idea of the strategy they want to trade, the position sizing, and the timing of the entry and exits.

Different market phases favour different vol stances. For example, when volatility is very low and there are tight ranges, short-vol strategies such as condors, straddles, and strangles work best. On the other hand, when there is vol Expansion Phase and a new breakout is starting, then long vol thrives.

Similarly, when we are already in a high-volatility regime and there is a post-shock drift, many traders shift towards a short-vol strategy because IV is expected to revert to the mean. Finally, when there is an event such as earnings or a budget, the pre-event can lead to an IV rise, and short vol strategies are dangerous. But after the event, there is IV crush, which can help with short-vol strategies.

Conclusion

If you strip away complexity, every strategy becomes:

Long Vol Strategy + Direction Bias

- Buy Call (long vol + bullish)

- Buy Put (long vol + bearish)

Short Vol Strategy + Direction Bias

- Sell Put (short vol + bullish)

- Covered Call (short vol + neutral to mild bullish)

Neutral Vol Plays

- Butterfly spreads

- Ratio spreads (can be tuned)

As a trader, this is the strategy that we can trade based on expectation:

- If the trader is expecting a big move with low IV, then we can go for long vol strategies (straddle/strangle)

- If the trader is expecting no move with high IV, then we can go for short vol strategies (condor/strangle)

- If the trader is expecting slow drift with time decay, then we can go for short vol strategies (cash secured puts, covered calls)

- If the trader is expecting a volatility collapse, then we can go for short vega strategies