Selling Penny Options: Small Gains, Massive Risk

Option writers make money by shorting out-of-the-money options because they feel that if the options remain out of the money, then they will eat the entire premium. A lot of the time, traders will short a far-out-of-the-money option for ₹3, ₹5, or ₹8, hoping the underlying will not move and the option will expire worthless.

While this works a lot of the time, since Nifty will not move 400 or 500 points in a single day, it looks very lucrative. The probability is with the option writers that the option they are shorting will expire worthless.

However, there is no guarantee. Overall, over the long horizon, there could be a Black Swan event in which Nifty moves significantly and eats up the profits that option writers made in the last few years.

The reason is simple: Small, frequent gains cannot compensate for rare, large losses.

What Are Penny Options?

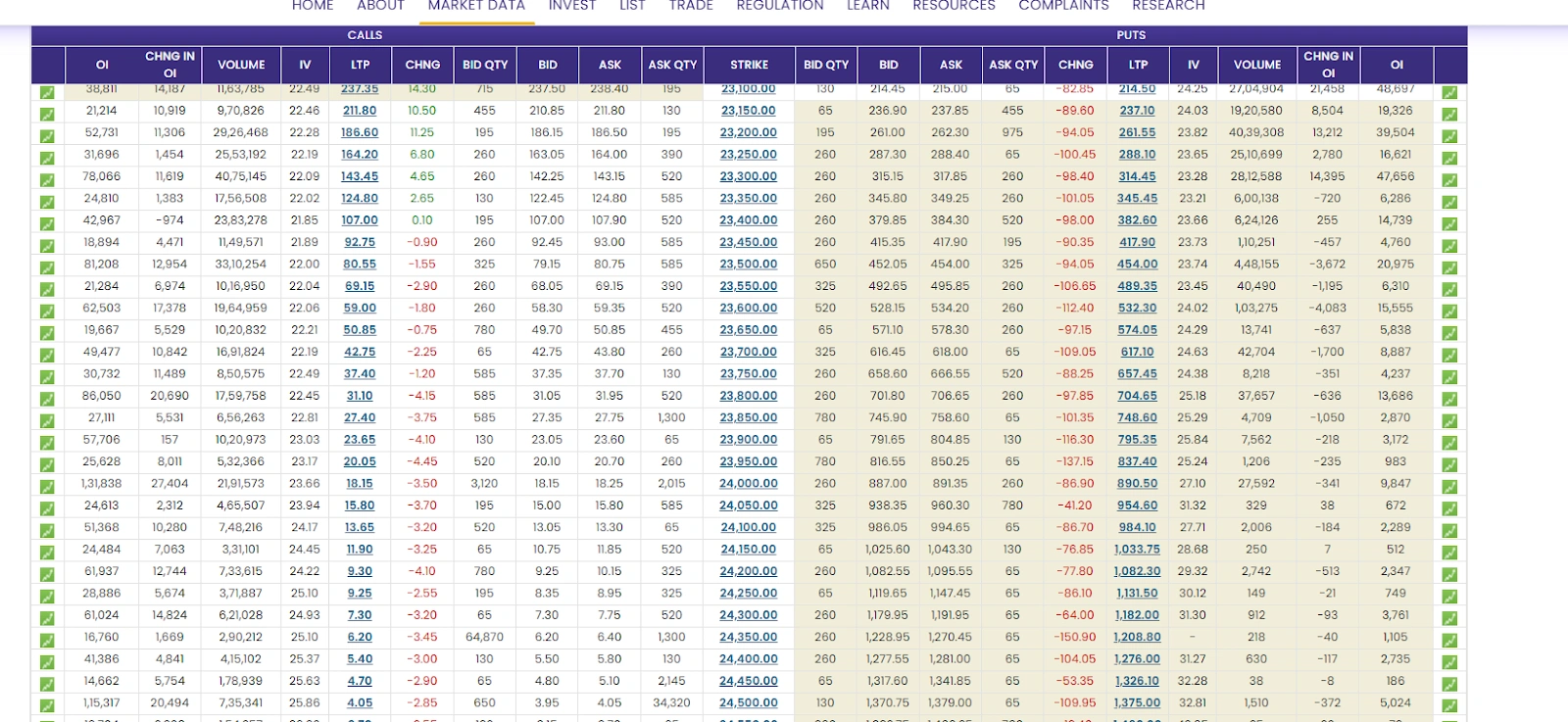

Penny options are extremely far OTM options trading at very low premiums. Let's look at the NSE option chain.

As you can see, the 21,000 Put Option is trading at 3.85

And the 24,500 Call option is trading at 4.05

The current price of Nifty is 23,114.5

So selling these options looks very attractive because Nifty has to move either 1,500 points up or almost 2,000 points down for these options to become in the money. Definitely, the probability of this happening is extremely low. But probability alone does not define profitability.

The Hidden Risk: Asymmetric Payoff

When we sell penny options, the total premium is the maximum profit. So, for example, if we have sold a ₹5 option, the maximum profit is just ₹5. However, if a Black Swan event occurs, the loss can be extremely large. Hence, there is a significant asymmetry between the profits and potential losses when selling penny options. This creates an unfavourable payoff structure. One big loss can wipe out profits for the entire year.

So let us take an example. Let's say a trader is trading ₹5 call and ₹5 put options every week. The lot size of Nifty is 65. So the total profit per week is ₹650. Since there will be four trades (2 entries and 2 exits), the net brokerage cost and other costs will be around ₹100. So the net profit the trader is making every week is around ₹550. This equates to around 8 points per expiry.

Now, let's say there is one Black Swan event in a year. A sudden downward move, and the option is now suddenly trading at ₹200.

The trader is making around 8 points per expiry. So 200 points is around 25 weeks' worth of profit! One bad day wipes out almost 6 months of profit.

Why the Strategy Feels Attractive

This strategy is very attractive for a few reasons. The first is psychological comfort. Since the strategy has an extremely high winning rate, traders like it. It is common to have 8 to 10 winning trades in a row. The profit seems very regular, which yields a smooth equity curve. It is easy to trade, as it takes only two trades per week, and there are no real adjustments to the strategy.

However, it has a very large tail-risk event. A sharp move can happen at any time and cause massive losses. Some reasons the strategy has not performed well in the past include global news, gap openings, event surprises, liquidity shocks, and short-covering rallies. These events are rare, but not rare enough. Another thing to note is that the markers produce large moves because information arrives suddenly, positioning becomes one-sided, stop losses trigger chain reactions, and volatility expands rapidly.

Another thing to keep in mind when trading this strategy is that far OTM options gain value very quickly. Some of the reasons are due to

- Delta expansion

- Gamma acceleration

- IV spike

Summary

Selling penny options is very attractive because the accuracy is extremely high. However, the strategy's extremely high accuracy also creates a lopsided risk-to-reward ratio. The strategy may work for a few months, but one big loss can wipe out years of profits in a single trade. Consistency in options trading comes from managing downside risk, not from chasing high-probability trades with poor payoff structures.