What Is Implied Volatility (IV) in Options Trading?

Options are highly leveraged and extremely volatile. Every trader is trying to get an idea of an option's volatility. This expectation of the future price movement of the underlying is represented by Implied Volatility (IV).

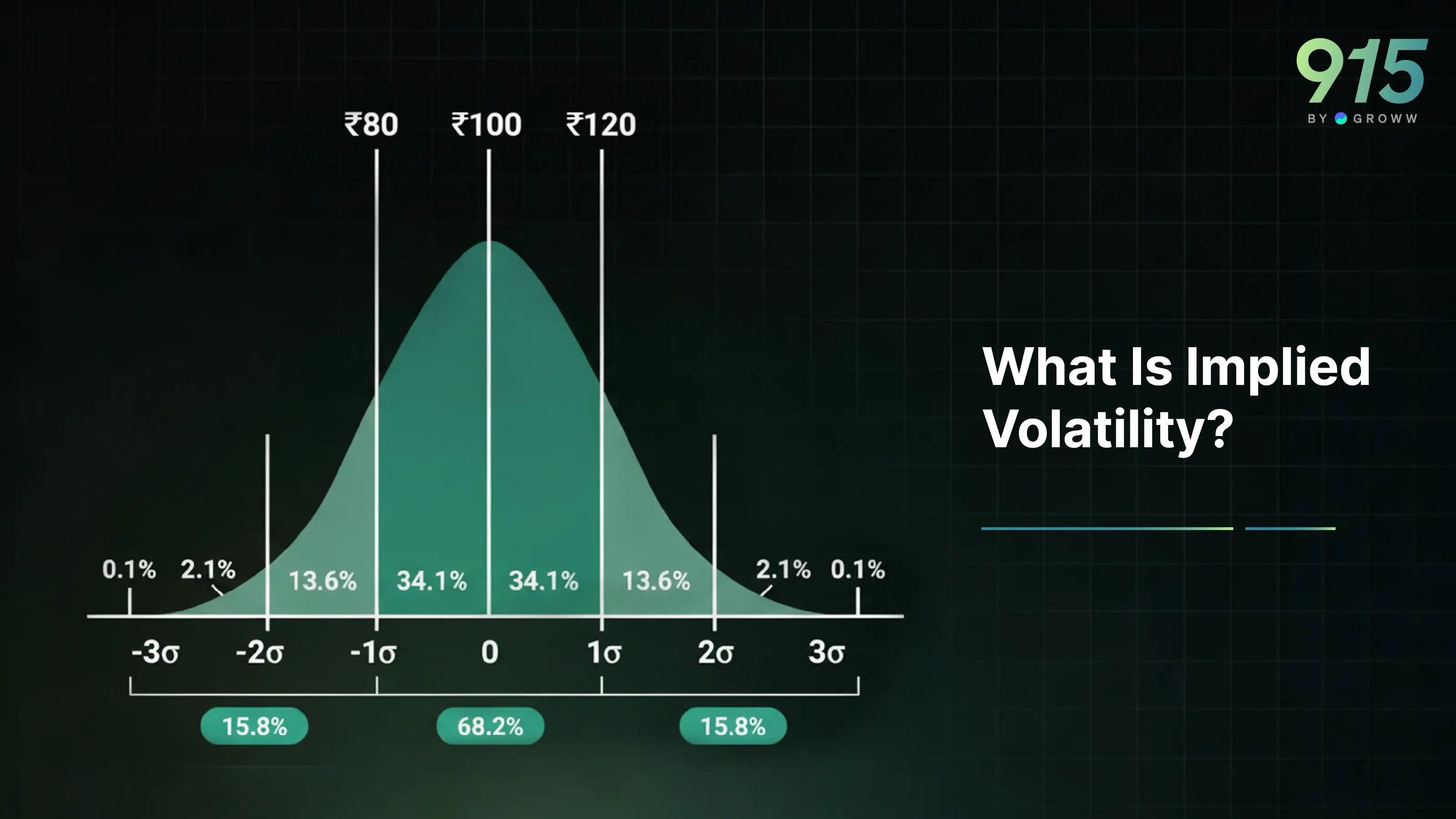

It is important to note that Implied Volatility is a scalar quantity. It only tells the magnitude of the expected movement. However, it fails to predict the direction, whether it’s going to go up or down. Usually, when the IV is high, the market is expecting big moves, and when the IV is low, the market is expecting small moves.

IV is dependent on a lot of variables such as premiums, risk, strategy selection, timing and profit potential

How IV Impacts Option Premiums

Option prices are very complex and are impacted by intrinsic value, time value as well as volatility premium. When the IV is high, it results in expensive options. On the other hand, when the IV is low, the options are relatively cheap.

From a trading perspective, an option buyer would prefer:

- Low IV at the entry

- High IV at the exit

An option writer would prefer the opposite:

- High IV at the entry

- IV crush after the event

In fact, most of the time, many traders lose money simply by ignoring the IV state.

Also check : Scalper Mode on 915 | Straddle Chart

IV Crush: The Silent Risk for Option Buyers

Have you noticed option prices drop unexpectedly after an important event, such as an earnings announcement or a budget? The sudden drop in option prices is due to a decline in IV. This phenomenon is called IV Crush.

This is common not only after earnings announcements, but also after Fed meetings, major news releases, and during the results season. Here are some examples of when an IV crush can happen:

Let's say a trader expected the price of stock ABC to rise due to its earnings. The earnings were positive, and the stock rose slightly after the results were announced. However, after the event and the uncertainty had passed, IV collapsed, resulting in an IV crush.

As a result, the option prices fell, and the trader lost money despite being correct about the predicted direction.

IV Expansion: Opportunity for Option Sellers

While IV crush is bad for option buyers, IV expansion can help option buyers immensely. IV expansion refers to an increase in IV, which in turn increases the option premium. Some of the reasons why IV expansion can occur:

- Geopolitical tensions

- Election periods

- Sudden market volatility spikes

When IV expansion occurs, premiums rise rapidly. If the option buyer is already in trade, he can gain handsomely during this time. A lot of option writing also occurs at elevated premiums because option writers expect the elevated IVs to cool off and make a profit. Overall, knowing when IV is elevated helps traders avoid poor timing.

IV Rank and IV Percentile

We have been using the terms “high IV” and “low IV”. But how do we decipher whether the IV is high or not? Is 10 IV high or is 100 IV high? And perhaps the degree will also depend on the symbol we are checking. For example, since Banknifty is more volatile than Nifty, it is bound to have higher IV. So, there are two metrics that can help us compare the current IV to historical ranges:

IV Rank

Formula:

(Current IV – 52-week IV Low) / (52-week IV High – 52-week IV Low)

So, if the IV rank is 0%, it means that the current IV is very low. On the other hand, if the IV rank is close to 100%, that means that the current IV is very high.

IV Percentile

The IV percentile shows how many days in the past year had IV lower than today. For example, if the IV Percentile is 80%. It means “IV today is higher than 80% of last year.”

Using both IV rank and IV percentile, traders can decide whether the IV is high or low and take trades accordingly.

What Drives Implied Volatility?

Let us now discuss why IV moves. Contrary to popular belief that IV moves based on news, IV actually reacts to expectations. Some of the main drivers of IV are:

- Earnings announcements

- Economic policy releases (Fed/RBI)

- Geopolitical tensions

- Major elections

- Interest rate changes

- Market crashes

- Commodity shocks

- Liquidity crunches

- Unexpected corporate events

IV vs Historical Volatility (HV)

Another concept is HV. HV, or historical volatility, measures past price movements. So, in essence, it is backwards-looking. The option prices can also be predicted using the comparison of IV vs HV:

- If IV > HV, this can lead to options being more expensive

- If IV < HV, options are usually cheap

Professional traders constantly monitor this gap.

Vega: The Greek Connected to IV

There is a common confusion about IV and Vega. Vega measures the change in the option premium for a given change in IV. ATM options have high Vega, so they gain value quickly when IV rises and lose value quickly when IV falls.

It is very important for option traders to focus on Vega. From the option buyer's perspective, a high Vega combined with a fall in IV can lead to big losses. Similarly, for option writers, high Vega can lead to losses when IV increases.

A very important property of IV is that it is mean-reverting. Hence, IV does not remain extremely high or extremely low for long. During some crisis or due to some unforeseen circumstances, the IV can spike dramatically, but it slowly normalises to its average. This mean-reversion property is why option sellers thrive during high-IV environments.

Practical Framework for Traders

Here are some frameworks that traders can use to trade options based on IV.

For option buying:

- A low IV environment is preferred. However, IV should not be too low as well

- Expected IV expansion (news ahead). However, the exit should be done before the news is announced

- Trending markets and strong directional conviction can help option buyers

Option Selling can be done based on the following:

- A high IV environment is usually helpful for option writes because the option premiums are high

- If there is an expected IV crush after the event, it can be used by option writers for their benefit

- Mean-reversion setups are always good for option writers

Conclusion

Options trading is complex, and Implied Volatility is one of its core pillars. IV can influence option premiums, along with strategy selection and the risk-reward ratio. Every trader should understand how IV works, as it can help turn options into a structured business. As a trader, the goal is to respect volatility and take informed decisions after checking IV and HV.