How Greeks Are Used to Manage Options Positions

Options are complex instruments. The price or the premium of the option is not just dependent on the direction. It depends on many other parameters, such as volatility, time, and speed of movement.

Since options are a derivative, their prices can not only be seen from the live market, but can also be calculated using mathematical models. Black-Scholes is one such model that helps to model option prices. Greeks are also the output of this model. And the same Greeks are the mathematical measures that quantify how an option’s price will change with respect to different market factors. A common misconception is that Greeks are used by traders to predict the direction. While Greeks can give an idea of the direction, their main use is in controlling open positions.

Also check : Scalper Mode on 915 | Straddle Chart

Why Greeks Matter More Than Direction

Stocks and options are very different. Stocks are directional instruments and hence easier to understand. If we buy a stock and it goes up, we stand to make a profit. On the other hand, if the stock goes down, we make a loss.

This is NOT the case in options. If we buy a call option and the stock goes up, it is perfectly possible that we make a good profit, a medium profit, no profit, or even end up with a loss. The reason is that in options, five dimensions matter:

- Direction (Delta)

- Speed of movement (Gamma)

- Volatility (Vega)

- Time decay (Theta)

- Interest rates (Rho — less relevant for short maturities)

Each affects P&L differently. Greeks allow traders to measure these forces rather than guess.

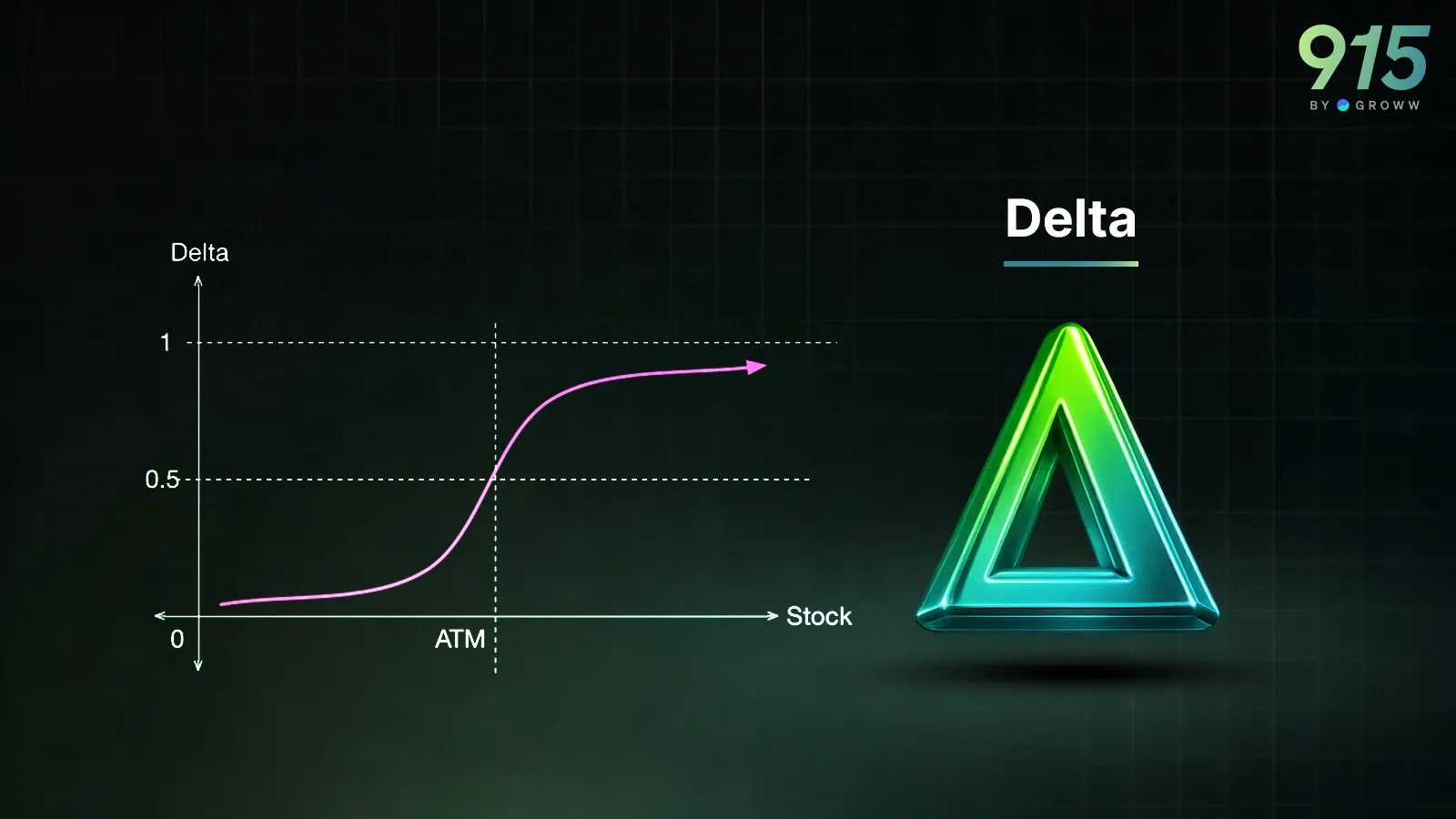

1. Delta - Directional Exposure (Equity Equivalent)

Delta measures how much an option moves for every 1-point move in the underlying. If the delta of a call option is +0.40 and the underlying (e.g., Nifty) moves up by 50 points, we can expect the option to move up by approximately 20 points (0.4*50).

Similarly, if the delta of a put option is -0.50, and if the underlying (for example, Nifty) moves up by 50 points, then we can expect the option to move down by approximately 25 points (0.5*50).

Delta can help with position management because it:

- Shows directional bias (bullish or bearish)

- Helps hedge using futures or stock

- Allows Delta-neutral strategies

- Tell the probability of the option to be ITM

So, in practice, traders use delta for various strategies. Option writers can make delta-neutral strategies, whereas option buyers can trade directional strategies by keeping a higher delta.

Another use of Delta is for hedging. If the delta is too positive, traders can hedge by selling futures or buying put options. If the delta is too negative, traders can hedge by buying calls or buying futures

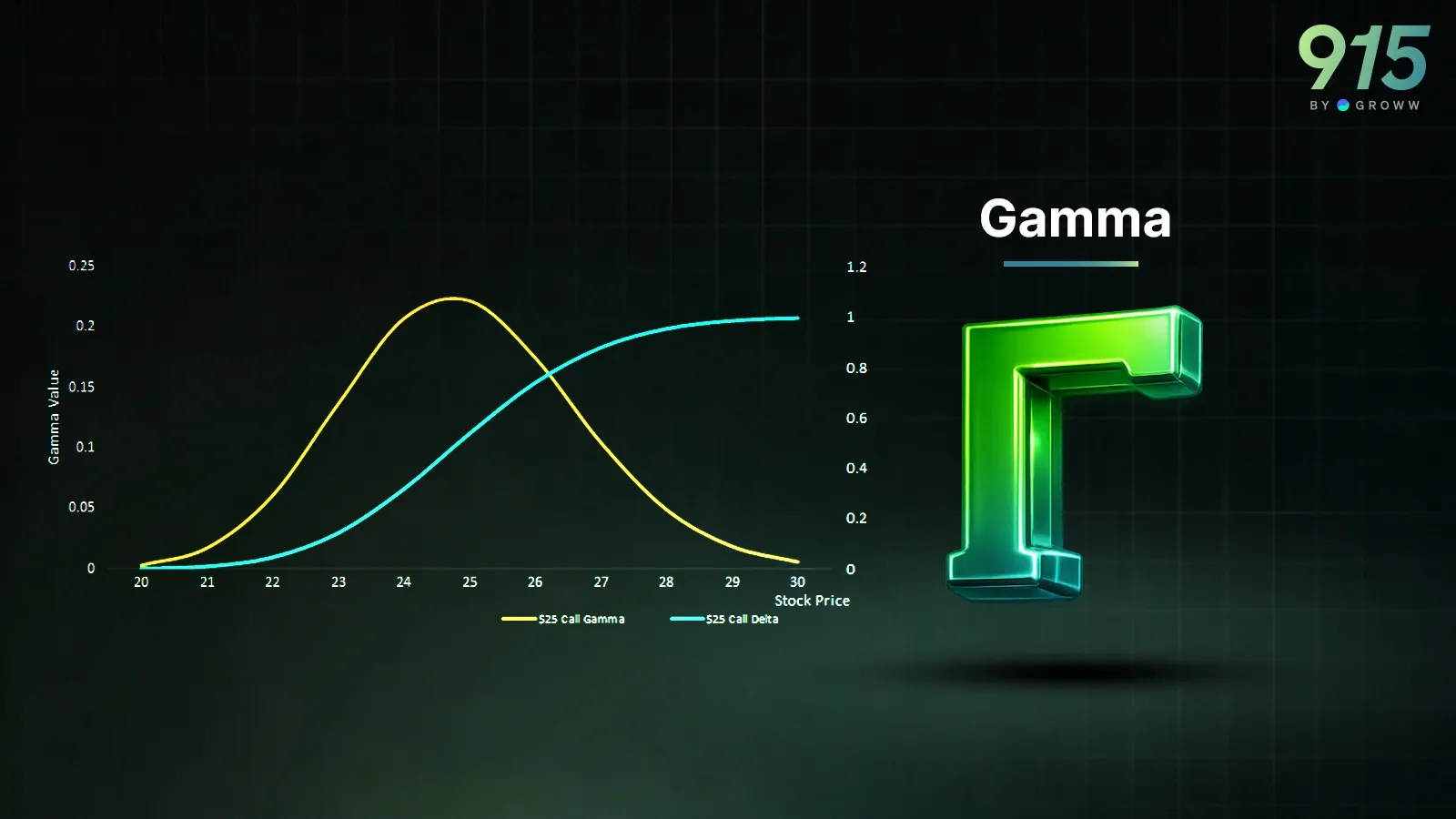

2. Gamma — Acceleration Risk (Danger for Sellers)

Gamma measures how fast Delta changes when the underlying moves. If gamma is high, delta changes quickly. Some of the features of gamma are:

- It is high near expiry

- If it is highest for ATM options and low for far OTM options

- It becomes gradually lower on distant experiences

Gamma can be used in traders' strategies. Usually, buyers benefit from high Gamma, while option writers get hurt by it. So, Gamma helps in explaining why:

- Short straddles are dangerous near expiry

- Markets with sharp moves punish option sellers

- “Gamma spikes” cause intraday blowups

Gamma also explains why options move extremely violently near expiry. The reason is that gamma risk explodes, and delta can change rapidly. Hence, option writers often reduce their position size near expiry or roll it to later expiries. Sometimes, it makes sense to shift strikes away from the ATM where the gamma is lower. Gamma explains most expiry-day volatility pain.

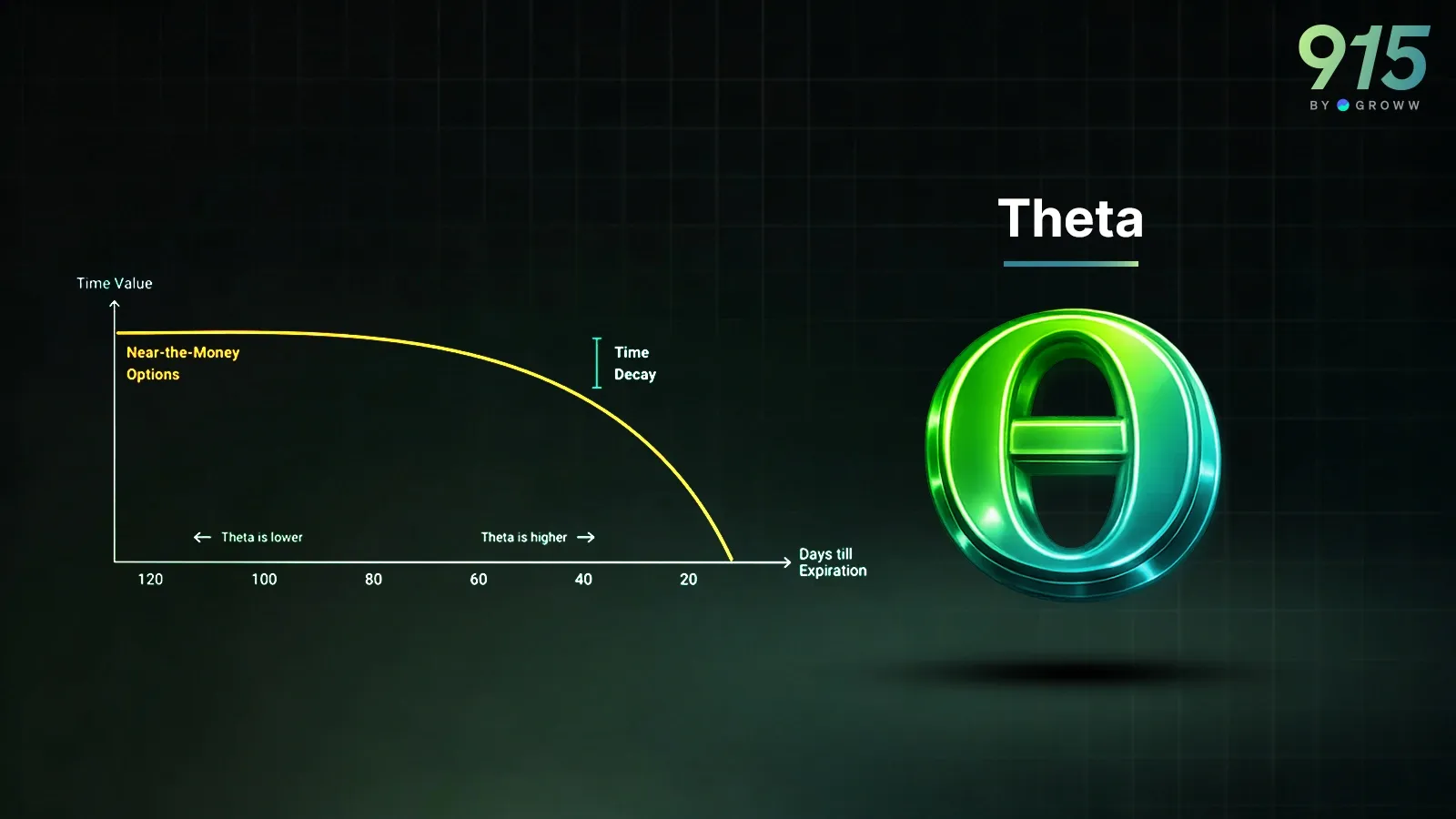

3. Theta — Time Decay (Seller’s Income)

Theta measures how much an option loses in value per day due to time decay. If theta is -5, the option loses ₹5 per day. Theta is great for option writers and hurts option buyers. Here are some of the characteristics of theta:

- It accelerates near expiry

- It is the highest for ATM options

- It is lower on longer-dated options

- It exists even when the market is asleep

Again, theta can be used for making strategies. Option sellers rely on constant decay and therefore use strategies such as a straddle. Option buyers fight against decay daily and hence like to come out of the position quickly. Neutral option sellers maximise theta in range-bound markets.

Theta clearly shows why option Sellers build strategies like below to gain consistent profits:

- Credit spreads

- Iron condors

- Short strangles

- Calendar spreads

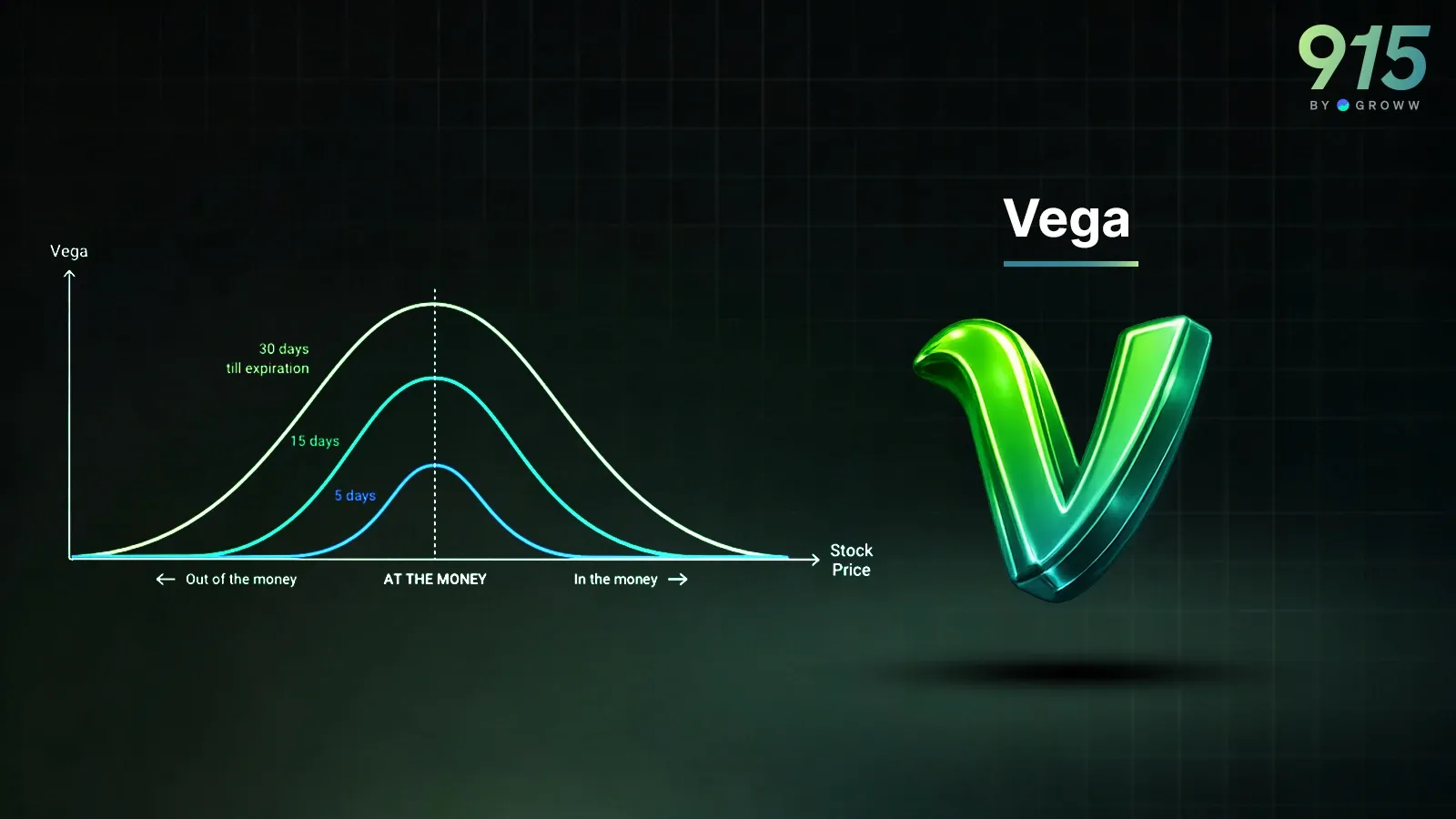

4. Vega — Volatility Sensitivity (Silent P&L Factor)

Vega measures how option prices change with 1% change in Implied Volatility (IV). For example, if Vega is 2.5 and the IV rises by 20% to 21%, then we can expect the option price to increase by 2.5 points. Here are some characteristics of Vega:

- Higher for longer expiries

- Higher for ATM options

- Lower near expiry

- Sensitive during events

Vega is also used for strategy building. If the trader expects the IV to expand, he can use an option-buying strategy to take advantage of Vega. On the other hand, if IV crush is happening, option writing strategies make a profit. Vega explains why option prices rise even when the underlying is flat, especially before the event.

Vega clearly shows why traders monitor their exposure during events such as earnings, elections, and the budget. A high Vega exposure during IV crush can lead to a high risk. Professional traders reduce vega in event risks.

Conclusion

To summarise, Greeks are often called the control panel of options trading. Professional traders use different Greeks to assist with hedging risk, controlling exposure, managing volatility, harvesting time decay, and avoiding gamma blowups. Direction alone is not enough in options; all the risk must be quantified. And Greeks provide that quantification.