How to Trade Options When IV Is in the 80th Percentile

Usually, high volatility means there will be significant price movements. This seems good for traders, as they expect greater opportunities and the temptation to buy options increases. However, it is important to understand that during high IV, option prices increase, and options are not cheap. Many times, the option is bought at a high price, and when the IV cools, it can lead to losses. Let’s understand how to approach this situation more structured and professionally.

IV and VIX

Let us first understand the difference and correlation between IV and VIX.

|

Aspect |

Implied Volatility (IV) |

VIX (Volatility Index) |

|

Definition |

This shows the expected volatility for a specific option’s price |

VIX shows the total expected volatility of the market |

|

Scope |

This is for individual options |

This is for the complete market |

|

Coverage |

The results will change based on ATM, OTM, and ITM |

This is usually a weighted |

|

Nature |

It is a micro-level view |

It is a macro-level view |

|

Calculation |

The calculation is done using the Black-Scholes Model |

It is calculated using different option IVs |

|

Movement |

It changes as per the options demand-supply |

This is dependent on the risk of the overall market |

|

Correlation |

It is positively correlated to VIX |

It is derived from IV and hence positively correlated with IV |

|

Example |

23,000 CE IV = 14%, 23,500 CE IV = 18% |

India VIX = 15 |

In a nutshell, both IV and VIX are positively correlated. Now we can see the current VIX chart, and it is already trading at a top 10 percentile.

Understanding IV at the 80th Percentile

An IV of 25 does not give a very meaningful picture. We need to compare “25” against its historical range to determine whether the current IV is high or low. Hence, the implied volatility percentile tells us how current IV compares to its historical range. If the IV is at the 80th percentile, it means that the current volatility is at the top 80% of the last 1 year of IV. This also means the options are trading at a higher premium.

Some reasons IV can be at a high price include budget announcements, central bank policy decisions, or global uncertainty.

Structuring Trades When IV is high

Different strategies offer a better risk-to-reward ratio when the IV is high. Here are some examples:

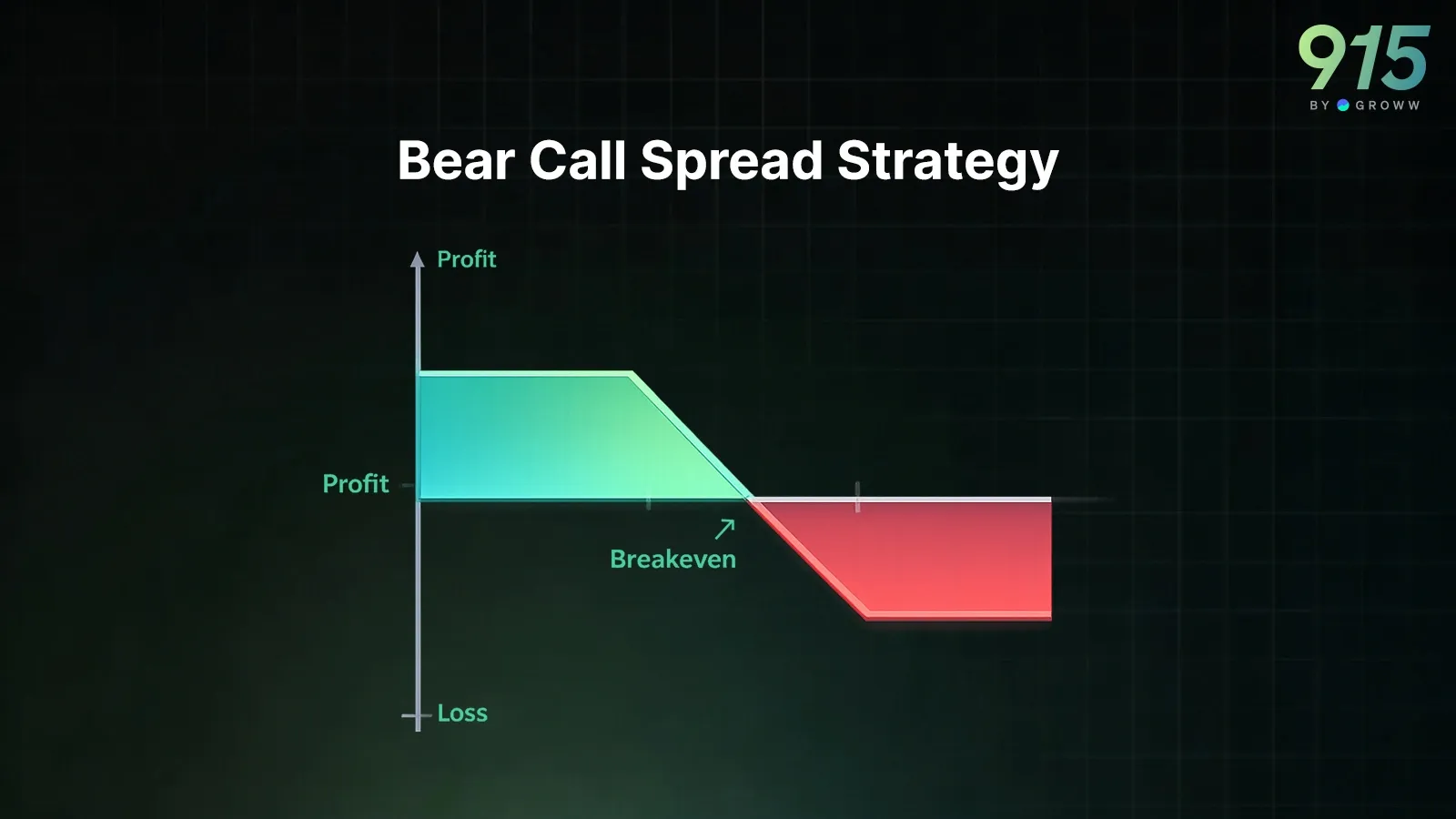

1. Bear Call Spread (Simple and Effective)

We have already seen that IV and VIX are positively correlated. Also, it is well known that the VIX and Nifty are inversely correlated. So if the IV is high, traders can expect the market to decline. This is what has happened for the last 1 month in Nifty. Nifty has fallen from 26,300 to 23,100.

So a bear call spread can be a good strategy. For example:

- Sell 23,200 CE

- Buy 23,500 CE

In this setup, the maximum profit is the total premium received. This is a fully hedged strategy. The strategy has a slight downward bias. Even if the market moves slightly upward, as long as it stays below your short strike, you benefit. Also, important to note that if IV drops after the event, both options lose value quickly, and the spread profits without requiring a precise directional call.

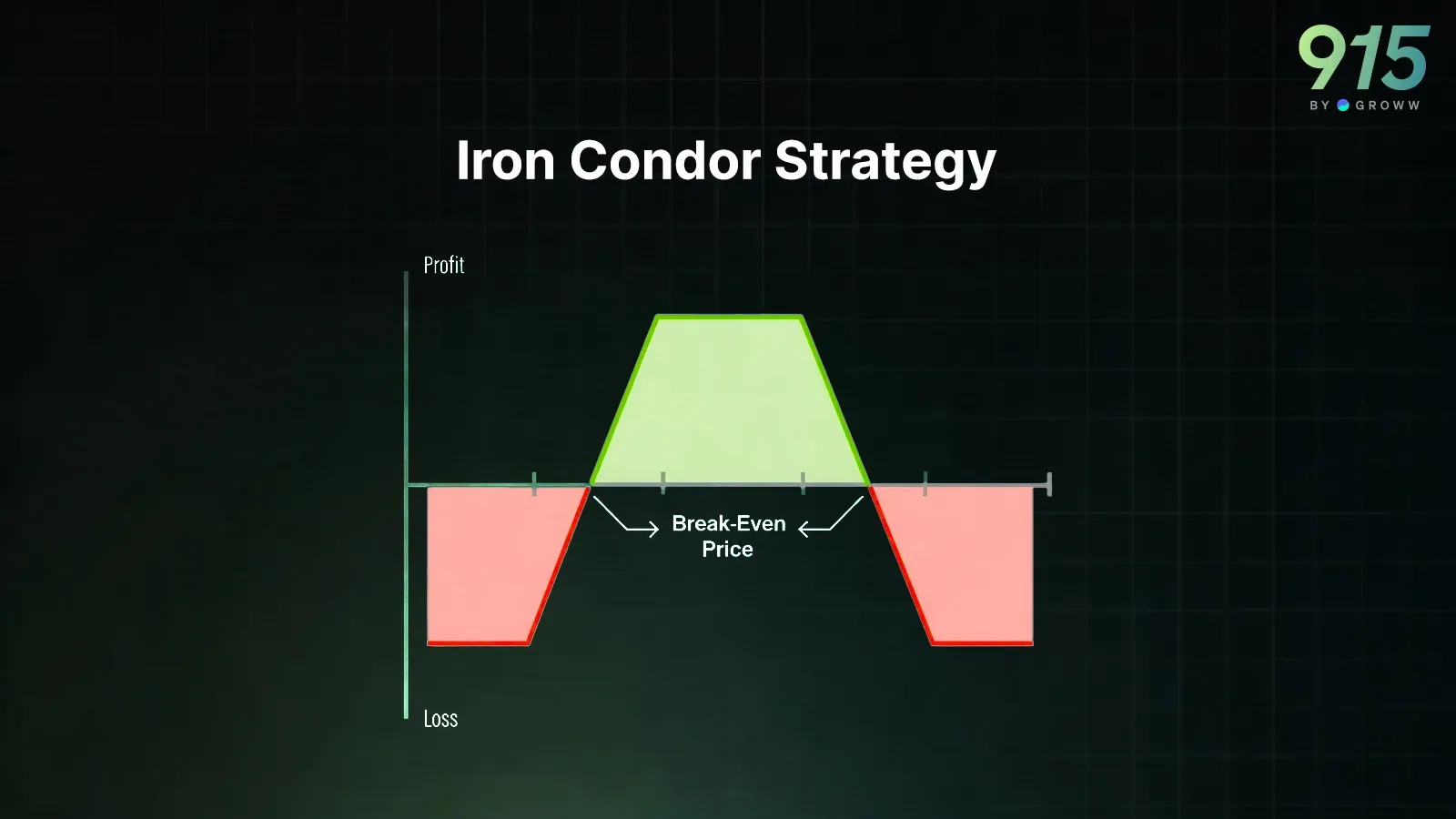

2. Iron Condor

On the other hand, if expectations are that the market will remain sideways, a good trading strategy is an Iron Condor. This is just an extension of the Bear Call Spread along with the Bull Put Spread. Here is one example, assuming Nifty to be around 23,000

- Sell 23,200 CE

- Buy 23,500 CE

- Sell 22,800 PE

- Buy 22,500 PE

The beauty of the strategy is that it allows traders to collect premiums from both sides of the market. If the event passes without extreme movement, volatility drops, and both sides decay simultaneously.

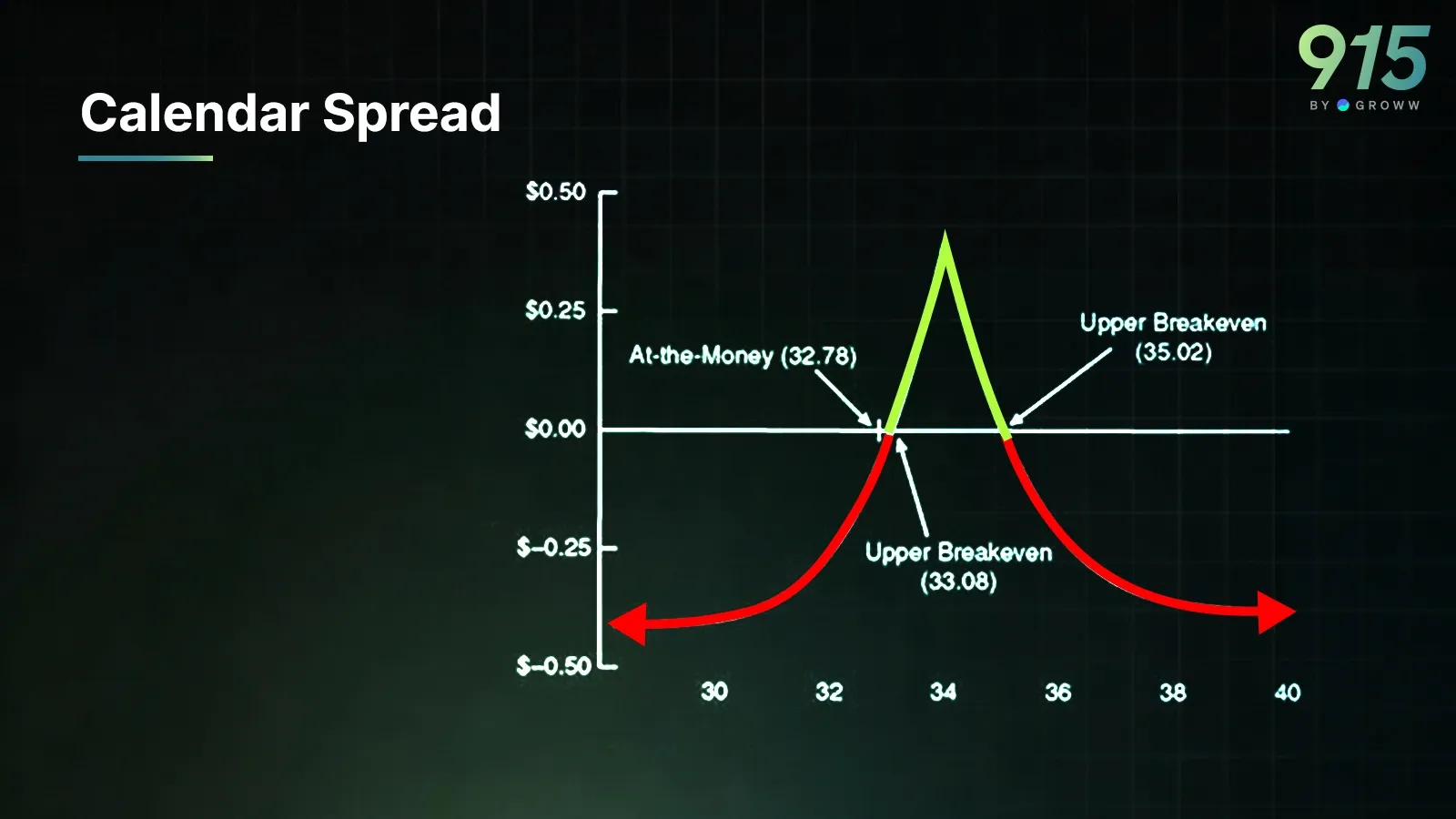

3. Calendar Spread (Volatility Timing Trade)

The third strategy is slightly advanced and involves using time to your advantage. If the expectation is that short-term volatility will drop sharply after the event. In contrast, longer-term volatility remains relatively stable, so a calendar spread is a great strategy to deploy. Here is how it can be implemented:

- Sell the current month ATM option

- Buy the next month ATM option

Summary

When trading in a high-IV environment, it is important always to prefer defined-risk strategies. While naked option buying and writing strategies may look attractive, they can entail significant risk.

Moreover, option Greeks become more important in a high-IV environment. A good understanding of theta and vega is very important when trading.

Some traders might prefer to buy cheap OTM options, expecting big moves, but most of the time these options end up being 0.