Gamma Risk Explained Through 0DTE Options

Expiry trading, or 0DTE (zero days to expiry) trades, has become extremely popular. The reason is that traders like options because they move very quickly, which gives them the possibility of quick profits. For option buyers, the movement helps them develop good directional strategies.

The most commonly traded strategy is the 0 hero trade. On the other hand, option writers like 0DTE trades because of extremely high theta decay. However, one of the most misunderstood risks in options on 0DTE is the gamma risk.

The major issue for option writers is the risk-to-reward ratio. If their initial view is wrong and there is a sudden move against them, it can lead to big losses, often due to Gamma. Hence, option writers need to understand Gamma and its implications to improve their trading strategies, especially on expiry day.

What is Gamma?

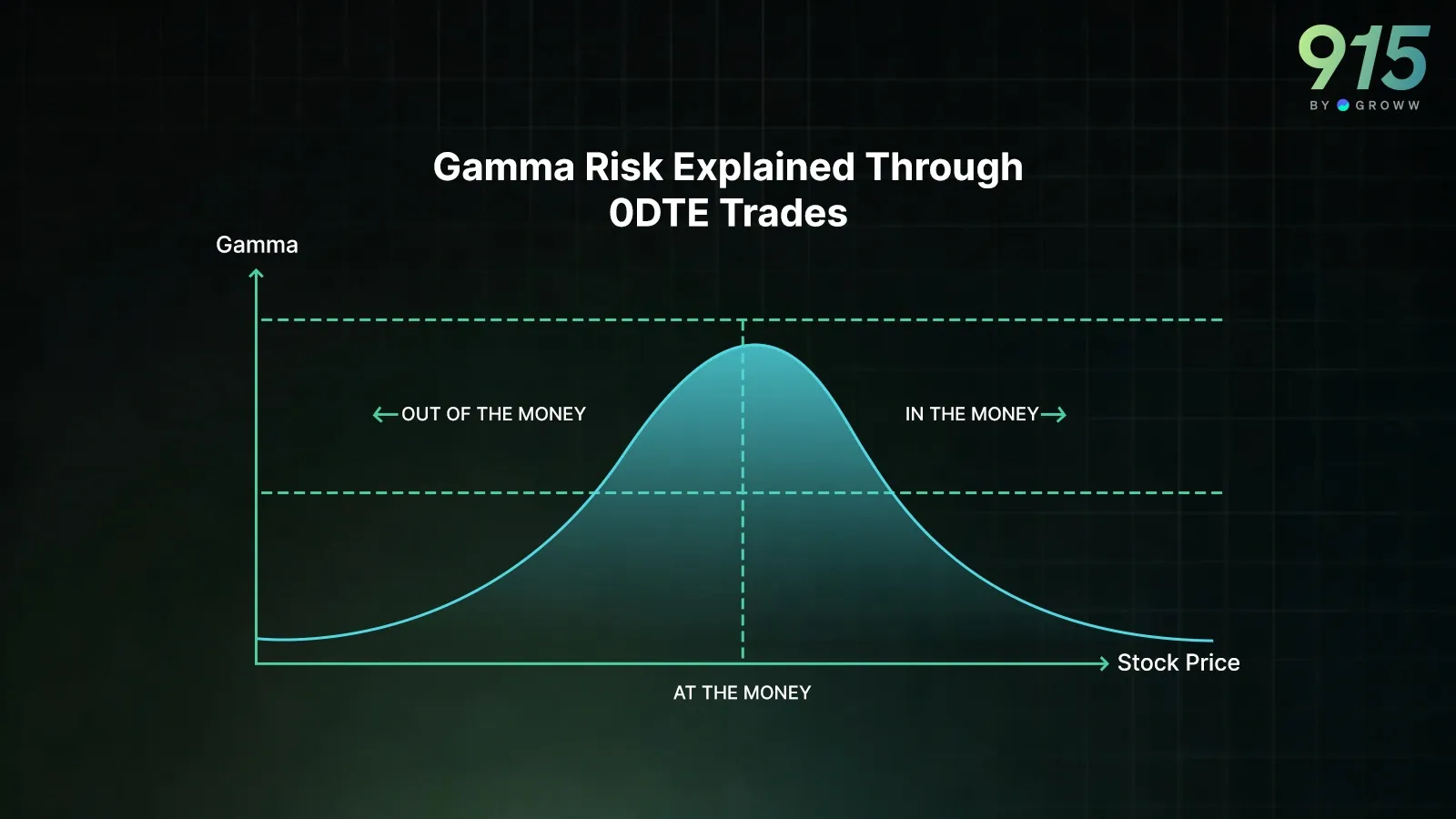

Gamma measures Delta's movement when the underlying moves. As we know, Delta shows how much the option can move when the underlying moves. If the Delta of the ATM option is 0.5 and the underlying moves by 100 points, then we can expect the option to move by 50 points. However, if there is a 100-point movement, then the ATM option will no longer be ATM. It would have shifted to be an ITM option, and hence its Delta should be more than 0.5. Let's assume it's 0.6. This change in the Delta from 0.5 to 0.6 is what is explained by Gamma.

In other words, we can say that Gamma tells us how quickly the position starts behaving very differently from what the trader initially thought. If a trade is taken assuming a Delta of 0.5, the movement will be approximately 50% of the underlying. Gamma will tell us the change in movement when there has been a sudden, quick movement in a particular direction.

When Gamma is high, even small movements in the underlying can create large changes in option price behaviour.

Why Gamma Is Highest in 0DTE

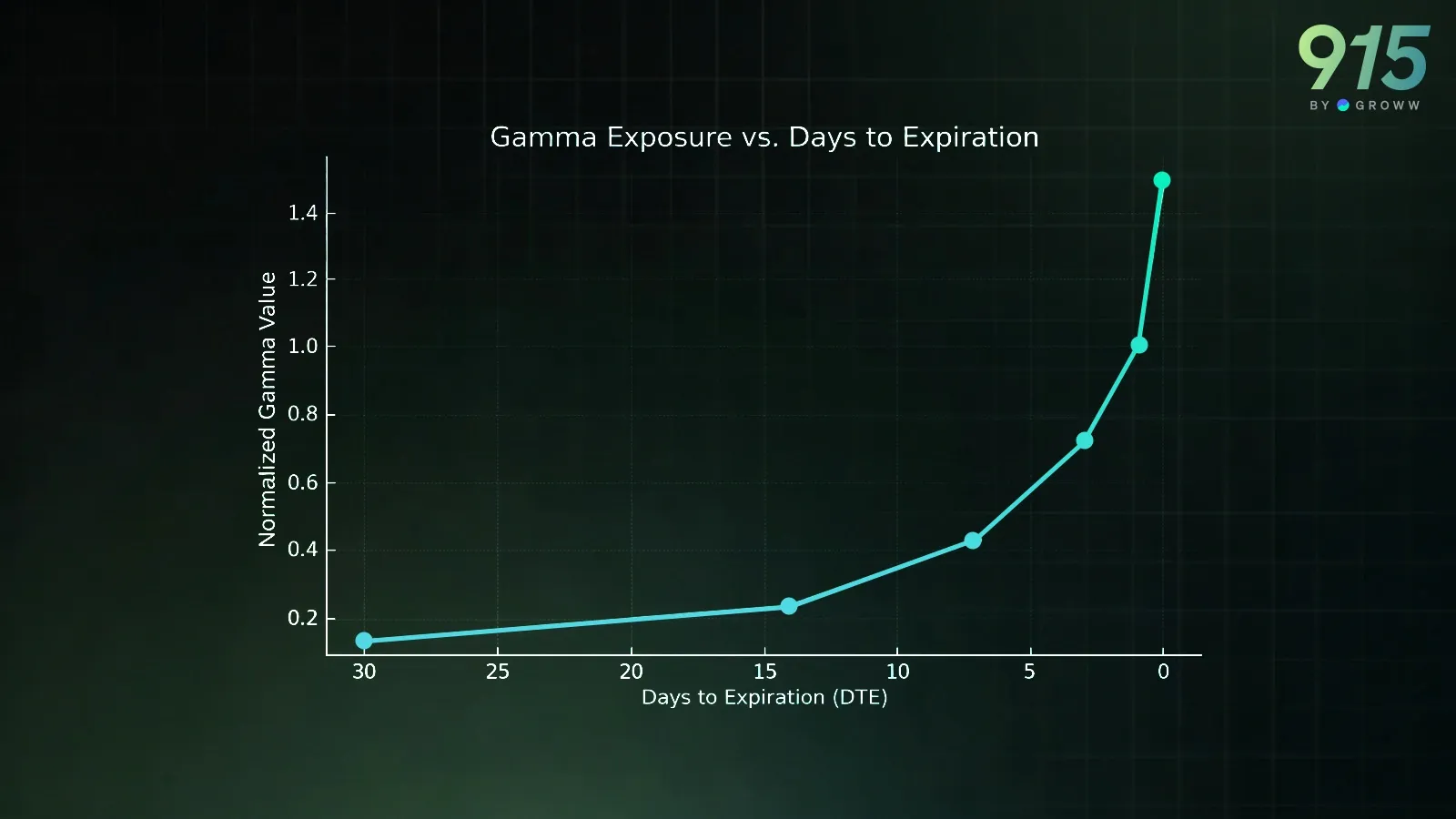

Here is how Gamma reacts as expiry approaches.

Both Gama and theta react differently as they approach expiry. As the expiry approaches, the theta decay accelerates. Theta Decay is highest on the day of the expiry. Above, you can see the Gamma exposure based on proximity to the expiry day. Similar to theta, Gamma increases as expiry approaches. Another thing to note here is that the increase in Gamma is exponential rather than linear.

The impact of both theta and Gamma is that, on the day of expiry, ATM options experience rapid changes in Delta. Moreover, the option premiums react extremely aggressively to even small changes in the underlying. This also means that the option sellers face a risk that becomes highly non-linear. Hence, the positions that look safe in the morning can become extremely risky extremely quickly.

Why Option Sellers Face Sudden Losses in 0DTE

One of the most common forms of trading is expiry day trading. This is usually done by option writers seeking to profit from theta decay. This is extremely attractive since theta decay is the fastest. However, the increase in Gamma simultaneously nullifies the benefit. Let us take an example. Let us assume that Nifty is at 23000 and the option writer has sold a 23,100 call option. At first, the option looks safe because it is 100 points out of the money. However, if the Nifty moves quickly towards 23,100, the following will happen.

- Delta increases rapidly

- Option price rises sharply

- Losses accelerate faster than expected

This is the exact gamma risk that is showing in action.

Why Option Buyers Also Need to Understand Gamma

While it may seem that Gamma applies only to option writers, option buyers also need to understand the Gamma effect. As an option buyer, Gama can usually help in the movement. So, for an option buyer, 0DTE trades offer:

- Quick momentum can generate rapid profits

- Slow movement can destroy option value quickly

So timing becomes extremely important. A delayed breakout often results in premium decay, even if the direction eventually works out.

How Gamma Changes Throughout the Day

That is the Gamma constant throughout the day. The answer is no. On the day of the expiry, in the morning, the Gamma will usually be moderate since the market still has time value. During the afternoon, the Gamma starts to increase rapidly. And over the last couple of hours, Gamma has risen sharply, and options have reacted violently to small price movements. Therefore, afternoon trades feel very unpredictable and risky on zero DTE.

How to Manage Gamma Risk

Traders can manage their Gamma risk by understanding Gamma and how it can help them create an edge in their trading strategies. They should also avoid selling naked options at the close of the expiry day. Moreover, a better strategy is to use spreads to limit gamma exposure. Position sizing can also be a tool to reduce Gamma exposure, since wing prices can be highly volatile. And finally, risk management is most important; traders must set their stop losses in the right places.

Summary

0DTE trades are very attractive due to the rapid theta decay. But this thete decay is nullified due to the increase in Gamma. Due to the Gamma, we see that on the day of expiry, there are violent movements even in response to small changes in the underlying. Gamma is often described as a second-order Greek, but in 0DTE trading, it becomes the primary driver of risk. It explains:

- Why small moves create large losses

- Why does expiry day feel unpredictable

- Why can risk suddenly increase even without news