10 Secrets Only Successful Mutual Fund Investors Know

There are many myths and false beliefs about mutual funds circulating in the markets.

The most successful investors are the ones that ignore the myths and pay attention only to what actually needs their attention.

Successful mutual fund investors know key details that many do not. These secrets are what gives them an edge in their investments.

Secrets Successful Mutual Fund Investor Wants to Tell You

Pay attention to these tips and tricks so you can become a successful investor too.

#1. Past Returns Does Not Mean Good Future Returns

When investing in any mutual fund category, don’t choose which fund to invest in solely based on its past returns.

Many times, a fund manager might have taken higher than normal risk that might have paid off.

The downside is that if the risk taken by the fund manager does not pay off, the mutual fund will under perform.

What to do? Always value consistent performance more than recent high returns. A high return over a long period of time is the hallmark of a good mutual fund.

#2. Lower NAV Is Not Always Better

NAV shouldn’t matter when investing in a mutual fund. Just make sure all other parameters are good.

Let’s say the NAV of a mutual fund called ABC is Rs 13.89, and the NAV of another mutual fund XYZ is Rs 82.56. It is not necessary that mutual fund ABC is a better investment than XYZ.

The NAV of any mutual fund does not indicate how much it will grow.

What to do? Choose good mutual funds based on important factors like AUM, past return consistency and more. Ignore the NAV.

#3. Investment Value Can Go down but that’s okay

The value of a mutual fund can go down in the short term. This is even more relevant in the case of an equity mutual fund.

This is no reason to panic. The value of a mutual fund investment cannot consistently keep going upward.

Equity mutual funds are long-term investments. Checking the value of your investment every single day and panicking at the slightest downward movement is unnecessary.

If you panic and sell when the markets are down, all you will be doing is buying high and selling low.

Stay invested for the long term and review your mutual fund investments every few weeks.

What to do? Don’t panic or fall for the hype. If you’re in doubt, research the market conditions carefully or contact a mutual fund advisor.

#4. Timing the Market Is Hard, Keep Investing

Timing the market is very hard and is something even the best investors struggle to do.

Timing the market refers to investing when the markets are low and selling when the markets are high.

The problem with this approach is that it is nearly impossible to say with certainty if the markets are high or low.

Think the markets are low? What guarantee is there that the markets won’t go down further? Same with the markets being high.

What to do? Opt for investing in mutual funds regularly via SIP (Systematic Investment Plan) or STP (Systematic Transfer Plan). With SIP and STP, you are able to take advantage of cost averaging thus reducing the risk. Read: 13 Things to Know About SIP & What is STP.

#5. Returns Are More Important Than Expense Ratio

Many people look for mutual funds with a low expense ratio. In doing so, they are willing to skip investing in mutual funds that give higher returns.

This is a very wrong move.

Mutual fund returns that are displayed are after the expense ratio has been paid.

What to do? If two mutual funds from the same category are compared, and one has consistently given higher returns, you should invest in it without paying much attention to the expense ratio.

#6. Small Increase in Investment Amount Can Make a Big Difference in Returns

You should invest even slightly more if you can. Thanks to compounding, even a small increase can lead to a much bigger increase in returns.

Look at this example:

| Case 1 | Case 2 |

| Rs 15,000/month in SIP | Rs 16,000/month in SIP |

| 15% p.a return | 15% p.a return |

| 10 years | 10 years |

| Rs 38,99,589 | Rs 41,59,562 |

So you can see, just by increasing your investment amount by Rs 1,000, you can end up making nearly around Rs 2.5 lakh more.

The returns above are assumed and are meant only for use in this example.

#7. ELSS Mutual Funds Are One of the Best Ways to Save Tax

ELSS mutual funds are investments that let you save tax under section 80C.

ELSS funds have the lowest lock-in period of 3 years among all other options that let you save tax under section 80C. They have also offered some of the highest returns among all tax savings options.

What to do? To save tax under section 80C, explore investing in ELSS Funds.

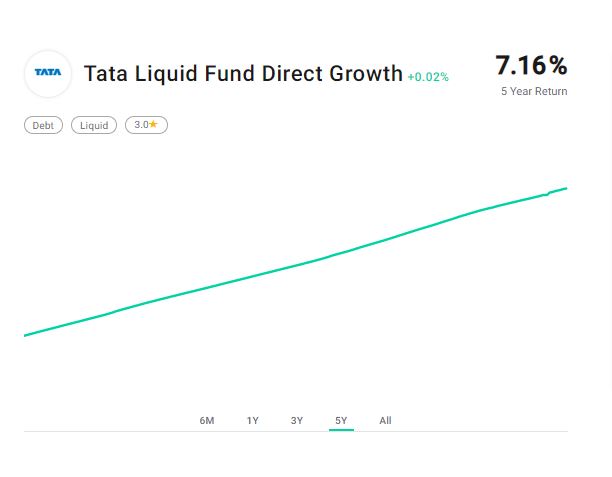

#8. Keeping Money in the Bank Is like Losing It

Savings bank accounts are giving interest of around 3.5%. Liquid funds these days are giving interest of 7%.

And, liquid funds are extremely low-risk mutual funds.

Look at returns given by Tata Liquid Fund over the last 5 years.

The line is nearly straight – no dips.

When you invest in any mutual fund, it takes around 3-4 working days to process the transaction. In the case of liquid funds, it only takes 1-2 working days.

This makes liquid funds a great alternative to keeping cash reserves in a savings bank account.

What to do? What is a liquid fund? Consider using liquid funds as an alternative to keeping money in the savings bank account. Read:

#9. There Are Mutual Funds for Nearly Every Kind of Need

Mutual funds are not just for long-term investing.

If you want to invest for a few days, invest in liquid funds. If you want to invest for a few months to a year, look at ultra-short debt funds.

Here is a table to give you an idea of the types of mutual funds.

| Fund Type | Ideal Duration |

| Large-cap Funds | 4+ years |

| Mid-cap Funds | 6+ years |

| Small-cap Funds | 7+ years |

| Multi-cap Funds | 5+ years |

| ELSS Funds | 3 year (mandatory) |

| Sector Funds | Variable |

| Eqiuty Oriented Balanced Fund | 2-3 years |

| Liquid Funds | Few days – Few weeks |

| Ultra Short Term Funds | 6 months – 1 year |

| Short Term Funds | 1-3 years |

| Monthly Income Plan (MIP) | Variable* |

| Gilt Funds | 1+ year |

| Income Funds | 1-3 years |

| Debt Oriented Balanced Fund | 2-3 years |

What to do? Explore all types of mutual funds. They offer a varying level of flexibility. Read: Types of Mutual Funds

#10. All Mutual Fund Companies are Safe to Invest

All mutual fund companies are monitored and regulated by SEBI. Therefore you need to not stick to only the big names.

As long as you feel a mutual fund suits your expectations, invest in it.

Happy investing!

Disclaimer: This content has been contributed by the content desk of Tata Mutual Funds. The views expressed here are of the author and do not reflect those of Groww.