ETF Creation and Redemption Process Explained

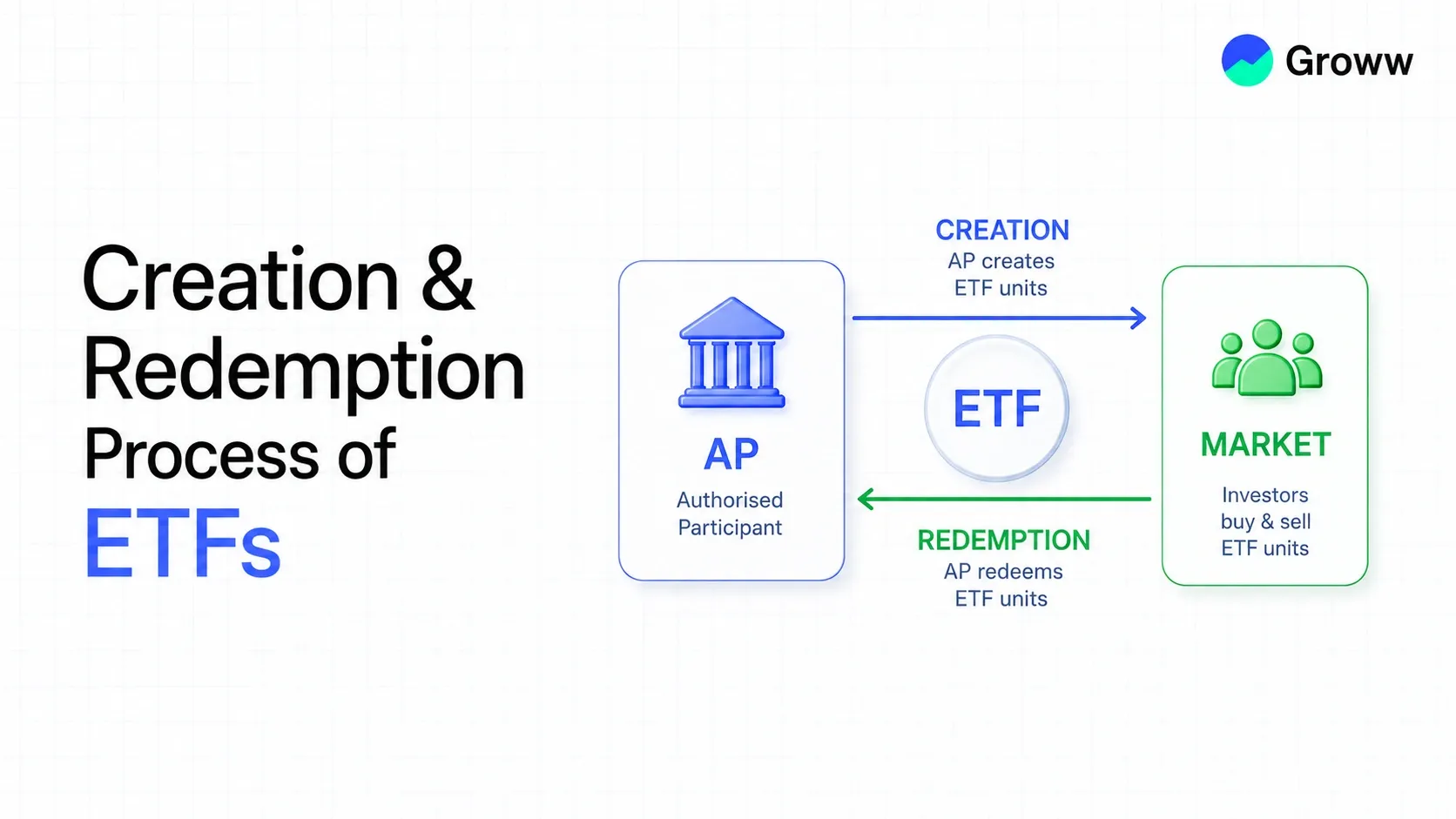

The creation and redemption process for ETFs in India is an in-kind system managed by APs (Authorised Participants). They create new ETF units by delivering baskets of underlying securities to AMCs (asset management companies), and redeem them by returning units for underlying securities.

The primary market mechanism ensures that the ETF price remains near the NAV (net asset value). So, in this case, the authorised participants (market makers or large institutional investors) play a vital role. A large block of ETF units may be created or redeemed at once, whereas the exchange of securities for ETF shares (or vice versa) helps ensure tax efficiency and lower costs.

ETF creation and redemption are important for investors since they ensure lower costs and tax efficiency. This is because of the in-kind exchange, in which the fund does not have to sell securities to meet investors' redemption requests. This keeps the transaction costs on the lower side while minimising the realisation of capital gains (taxable).

The system also keeps market prices stable, ensuring ETF prices stay close to their NAVs. If the ETF trades above its underlying assets, the APs create additional shares to sell, thereby lowering prices. If it trades lower, they redeem shares, thereby raising prices accordingly.

The ability to create new shares helps investors usually purchase or sell large quantities without any major impact on the share price. Unlike mutual funds, where redemptions by a single investor may trigger taxable events for everyone, the redemption process here means investors are not penalised by the buying or selling activities of others.

How ETFs Are Structured

ETFs (exchange-traded funds) are open-ended investment funds that trade on stock exchanges and allow investors to buy or sell shares throughout the day at market prices (unlike regular mutual funds).

Primary Market vs Secondary Market

ETFs function in two specific and interconnected markets.

Primary Market:

- This is where new ETF shares are created, while existing shares are also redeemed.

- Only APs transact here and directly deal with the ETF manager or issuer.

- This involves an in-kind procedure in which the APs deliver baskets of underlying securities to issuers to create new ETF shares or receive securities in exchange for redeeming them.

Secondary Market:

- This is where regular investors (institutional or retail) purchase and sell ETF shares on stock exchanges, much like individual stocks.

- Transactions take place between investors and not the ETF issuer.

- Prices are mainly driven by market supply and demand, although arbitrage keeps them closer to NAV.

Role of Authorised Participants (APs)

Authorised Participants (APs) are usually big financial institutions or market makers who are contracted by ETF issuers. They have a vital role to play in the following:

- Redeeming/Creating Shares: They are the sole entities that are allowed to redeem or create ETF shares in the primary market.

- Arbitrage System: If the price of an ETF in the secondary market deviates from its NAV (trading at a premium), APs will buy the underlying securities and create new ETF shares. They will then sell them to make a profit on the exchange. This pulls the ETF prices down towards the NAV.

- Enabling Ample Liquidity: By facilitating the creation and redemption of shares, APs ensure adequate ETF share inventory on the exchange. This keeps the bid-ask spreads tight.

A Creation Unit is the minimum block size of ETF shares that may be created or redeemed directly by APs (authorised participants) with ETF managers. Here are some key aspects worth noting.

- They are usually big blocks, usually comprising 25,000-100,000+ shares.

- The large size enables higher efficiency while allowing ETF issuers to manage the fund at lower transaction costs for smaller trades.

- APs gather specific security baskets needed to represent the creation unit. They also deliver the same to the issuer and then receive the corresponding ETF shares to sell in the secondary market.

Also Read: Passive ETFs | Build a Diversified Portfolio Using ETFs | Active vs Passive ETFs

The Creation Process Explained

Here is the process of how new ETF shares are created in a nutshell:

- Demand Growth: There is a surge in demand for an ETF, driving its market price above the value of the underlying securities it holds (a premium).

- AP Identification: Authorised Participants (usually market makers and big financial institutions) identify the price premium and the need for new share creation.

- Basket Assembling: The AP will then purchase the underlying securities, such as stocks and bonds, that the ETF is designed to hold. They are then assembled in the proportions required by the ETF manager.

- Issuer Delivery: This creation basket of securities is then delivered to the ETF issuer by the AP.

- Creation Unit Exchange: The ETF issuer, in return, provides a creation unit to the AP. This is a big block of ETF shares.

- Secondary Market Sale: The AP will sell these new ETF shares in the open market to investors, thereby reducing the price premium and aligning ETF prices with NAV.

In-Kind Creation vs Cash Creation

The creation basket may be delivered to issuers in two ways, although in-kind delivery is the traditional method. It is the standard system in which APs deliver the underlying securities, thereby ensuring higher tax efficiency (since taxable capital gains are not triggered when the fund receives the securities).

Cash Creation, on the other hand, is where cash is delivered to the ETF issuer by the AP. The issuer then uses the same to buy the required securities. It is used when the underlying securities are hard to buy, though it is less tax-efficient and may lead to higher transaction costs or slippage.

Example of a Creation Transaction

Let us assume a hypothetical ETF tracking the BFSI Top 10 index trades at a premium to its NAV. In this case, let’s say One Creation Unit is 50,000 shares of the BFSI ETF. Now, the ETF manager releases the necessary creation basket, i.e. a list of 10 stocks in particular proportions. The AP will then purchase 50,000 shares’ worth of the 10 stocks in the open market. It will also send this bundle to the issuer. The issuer will accept the same and issue 50,000 new shares to the AP.

The AP will now sell these 50,000 shares on the stock exchange, profiting from the difference since it purchased the underlying stocks at lower prices and sold ETF shares at a higher premium. Thus, the ETF’s market price stays in sync with the underlying holdings, except for any disruptions to existing investors.

The Redemption Process Explained

Redemption occurs only in the primary market between the ETF issuer and the AP, mostly in large blocks called Creation Units (typically 25,000-100,000+ shares). Here is a stepwise guide to redemption:

- Share Accumulation by the AP: The AP accumulates a big block of ETF shares from the secondary market.

- Redemption Order: The AP will notify the ETF sponsor of the wish to redeem a Creation Unit.

- Share Transfer: The AP transfers the block of ETF shares to the ETF issuer.

- Verification: The shares are verified by the ETF issuer.

- Asset Delivery: The ETF's issuer transfers the underlying securities (and sometimes a small cash component) to the AP from the fund's portfolio.

- Cancellation: The ETF issuer retires/destroys the returned shares, thereby reducing the fund's overall outstanding shares.

In-Kind Redemption vs Cash Redemption

In-kind redemption is when the AP returns ETF shares, while the issuer delivers the underlying securities held in the portfolio. The key benefits include higher tax efficiency (no capital gains taxes are triggered since no securities were sold for cash), lower transaction fees, and standard usage for a majority of fixed-income and equity ETFs.

Cash redemption is when the AP returns the ETF shares and the issuer pays the AP with cash (that is equal to the underlying security value). It is used when the underlying securities are difficult to transfer, and it is common in emerging or global markets. This may also be a mechanism for less-liquid and highly specialised ETFs. It may, however, trigger capital gains taxes within the fund and lower overall efficiency.

Example:

Let us imagine that an ETF tracks a particular U.S. stock index and is trading at a small discount to its NAV. An AP views this discount and wishes to profit from the same. The AP will then purchase 50,000 shares of the ETF from regular investors on the exchange. Thereafter, the AP will inform the issuer of the redemption of these shares for the underlying stocks.

Then there is an in-kind exchange where the AP will send 50,000 ETF shares to the issuer. This entity will then send back a basket of stocks representative of the ETF’s composition. The AP will sell the stocks on the open market, getting a higher value than what they paid for these shares. Hence, the supply of ETF shares declines, bringing ETF prices back into alignment with the NAV (and the AP also makes a profit).

Why Creation & Redemption Matter

Keeps ETF Market Price Close to NAV

- Arbitrage System - If the ETF's market price exceeds its NAV (premium), the APs will come into play and create new shares. They buy underlying securities and deliver them to the issuers, while selling the new ETFs for a profit. This higher supply brings prices down towards the NAV.

- Redemption Control - If the ETF trades below its NAV (discount), the AP will purchase cheaper ETF shares and redeem them with the issuer for underlying securities. Also, they will sell the securities for a profit, thereby reducing supply and pushing prices back up.

- Negligible Deviations - The self-correcting, constant arbitrage mechanism ensures that the ETF's exchange price closely tracks its actual portfolio value.

Provides Liquidity for Investors

- Dual-Layer Liquidity Aspect - ETF liquidity will not depend only on the exchange (secondary market) trading volume. Owing to creation or redemption, the ETF will be no more illiquid than its underlying assets.

- Supply On Demand - If demand for an ETF surges, APs can instantly create new shares. This ensures high liquidity, even for ETFs with low average daily trading volumes.

- Large and Efficient Trades - Big investors may execute large, low-cost trades in primary markets without causing major price fluctuations. It would otherwise take place in case they were purchasing small-cap stocks on exchanges.

Enhances Trading Efficiency

- In-Kind Transaction Type - Redemption and creation are usually handled through the in-kind system rather than using cash. It is thus a non-taxable mechanism, enabling ETF issuers to avoid selling appreciated securities (and triggering capital gains taxes).

- Lower Costs of Trading - Since APs handle underlying security trading, costs are not passed on to the fund. This may lead to tighter index tracking and lower investor costs.

- Insulated from Others - Unlike mutual funds, where a sizable redemption by even one investor can force security sales and trigger tax consequences for everyone, long-term holders are insulated here. This is ensured by the in-kind mechanism.

The Role of Arbitrage

ETF arbitrage is the practice of buying an ETF in one market and simultaneously selling it in another market. This is done for locking in a risk-free profit (when the market price of the ETF deviates from its NAV). An ETF may be overpriced if it trades at a premium, while it is underpriced if it is trading at a discount. APs are thus specialised players here, with the exclusive right to interact directly with ETF issuers to create or redeem shares.

Here’s how APs use arbitrage to align ETF price & NAV -

- Creation: When the ETF price exceeds its NAV, the AP buys underlying securities in the open market and delivers them to the ETF issuer. It also gets the newly created ETF shares in turn, then sells them, putting downward pressure on the premium.

- Redemption: When ETF prices are below NAV, the AP purchases undervalued ETF shares in the market. They then deliver them to issuers and receive the underlying securities. This pressure brings ETF prices into alignment with the NAV.

Impact on Price Stability

The effect on price stability is the following:

- Price Alignment - Arbitrage helps ensure that ETF shares rarely trade far from the underlying assets’ fair value.

- Higher Liquidity - APs function as market makers, enabling higher liquidity in the secondary market.

- Cost Efficiency - In-kind creation or redemption mechanisms prevent the fund from being forced to sell assets. This lowers transaction costs along with major shareholder consequences.

- Market Efficiency - The procedure keeps prices more accurate while also reflecting the actual value of the underlying security basket. It is crucial during times of higher volatility.

Benefits of the Creation & Redemption Mechanism

Cost Efficiency:

In-kind transactions allow APs to create/redeem large blocks of shares in exchange for underlying securities (rather than cash). The ETF manager can thus avoid the costs of buying and selling open-market securities. Since transactions do not trigger capital gains or instant brokerage fees, the savings get passed on to investors through low expense ratios. The mechanism also avoids the need to hold large cash reserves to manage redemptions by shareholders (this keeps more money invested as well).

Tax Efficiency:

When investors sell ETF shares, they usually sell to other investors in the secondary market rather than back to the funds. Hence, the funds rarely have to sell underlying securities and can bypass the realisation of capital gains. When an AP redeems shares, ETFs may transfer securities with low cost bases rather than sell them for cash. As a result, ETFs usually distribute less capital gains to shareholders than mutual funds.

Liquidity Benefits Compared to Mutual Funds

Unlike mutual funds, which price only once at the close of the day, ETFs may trade throughout the day on exchanges. This allows investors to buy or sell at market prices in real time. The redemption/creation system keeps ETF share prices in sync with the NAV and restricts arbitrage opportunities. This enables higher liquidity for big trades. Also, the ability to directly trade ETF shares with other market participants on the exchange is crucial. It means liquidity is not strictly dependent on the asset manager's daily cash flow. In many scenarios, this offers higher liquidity than directly holding the underlying assets.

How Mutual Fund Transactions Differ from ETF Creation/Redemption

Here are some key differences worth noting.

- Trading System and Timing: Mutual funds are traded once per day, after the market closes, at the NAV (net asset value). On the other hand, ETFs trade continuously, like stocks on an exchange. As a result, prices fluctuate throughout the day based on supply and demand.

- Transaction Parties: Transactions in mutual funds take place directly between the fund house and investors. ETF trades also usually occur between secondary market investors. Yet, APs trade directly with the fund to create or redeem shares.

- Creation or Redemption: When demand is high, the AP will create new ETF shares by providing a creation basket of securities/cash with the issuer. When supply is high, they redeem shares for the underlying assets. It happens in kind, lowering capital gains taxes compared to mutual funds (which may sell securities) that can trigger taxable events.

- Expenses: Mutual funds may carry higher expense ratios, sales loads, and early redemption charges. ETFs usually come with lower expense ratios but incur bid/ask spreads and brokerage commissions.

- Accessibility Aspects: Mutual funds will be accessible to specific amounts, thereby offering fractional shares. ETFs, on the other hand, are bought in whole shares and need a demat/brokerage account.

Practical Implications for Retail Investors

Can Individual Investors Use Creation/Redemption?

No, it is not possible for individual/retail investors to directly use the creation or redemption process. This only happens in the primary market and exclusively between the ETF issuer or AMC and the authorised participants (APs), who are mostly market makers and large financial institutions/banks. Creation or redemption occurs only in large blocks, which may require significant capital, making it unviable for retail investors as well. Individual investors may purchase and sell ETF shares only in the secondary market through brokerages. They can only redeem directly with the AMC in extremely rare situations where ETF liquidity is severely poor. Yet, this is not the standard procedure for operations.

How This Impacts ETF Liquidity & Trading on Groww

The redemption or creation process works as the core mechanism that ensures the efficient functioning of ETFs for retail investors on Groww. APs use this mechanism to arbitrage any discrepancies between the ETF market price on Groww and its NAV. This keeps ETF prices on Groww close to the actual underlying security values. It also allows long-term investors on Groww to remain insulated from others' short-term trading costs.

Due to active AP involvement, high-volume ETFs (Nifty BeES) usually have narrow bid-ask spreads, thereby enabling efficient entry and exit on Groww.