Fresh Issue vs OFS: Key Differences Explained

Understanding the difference between a fresh issue and an offer for sale is important in the context of an IPO (initial public offering). A fresh issue raises new capital for the company's growth and expansion, while an offer for sale (OFS) permits existing investors and promoters to sell their shares and cash out. Many IPOs use a combination of these two methods.

Read on below for a more detailed look at the fresh issue vs OFS differences, along with their core differences.

What Is a Fresh Issue in an IPO?

It is basically when a company creates and sells its brand-new shares to the general public. The objective here is to raise new capital that goes directly into the company’s account to fund operations, growth, expansion, or even debt reduction. Here’s how it essentially works:

- The company raises money from the public by selling new shares.

- The proceeds directly flow into the company and increase its total paid-up share capital.

- Since there are more shares in total, the proportionate ownership of existing shareholders will also be diluted.

- A large fresh issue is an indicator that the company's promoters are retaining their stakes, reflecting a strong belief in the entity’s future growth prospects.

- The company lays out its plans for how it will spend the money raised in its offer document or prospectus. Some common use cases include expansion (new technologies, operations, factories, and geographic expansion), debt repayment (repaying existing loans to lower interest costs), working capital (day-to-day operations and business sustainability), and R&D (new product research and development).

What Is OFS in an IPO?

OFS stands for Offer for Sale. In an IPO, existing shareholders (such as founders, promoters, and early investors) sell a portion of their shares to the general public.

Unlike in a fresh issue, the company does not issue new shares, and the proceeds go only to the selling shareholders rather than to the company. There is only a transfer of ownership or existing shares to new investors without any dilution of the company’s equity.

Since no new shares are created, the money paid by investors goes directly to the selling shareholders. Existing investors and shareholders can thus monetise or cash out with a seamless exit route.

Fresh Issue vs OFS: The Core Differences

Here is a closer look at the main difference between a fresh issue and OFS.

|

Key Aspect |

Fresh Issue |

OFS (Offer for Sale) |

|

What takes place |

The company issues new shares to the general public |

Existing shareholders (investors/promoters) sell their existing shares |

|

Where do the funds go? |

Directly to the company in order to fund debt, expansion or operations |

Directly to the selling shareholders |

|

Number of shares |

The overall number of outstanding shares increases |

The total shares remain the same, but the ownership changes |

|

Investor effect |

The ownership of existing shareholders is diluted |

There is no dilution to the equity base of the company |

|

Usual objective |

Expansion, R&D, repaying debt, working capital and general corporate purposes |

Liquidity, complete/partial exit for early investors, and regulatory compliance |

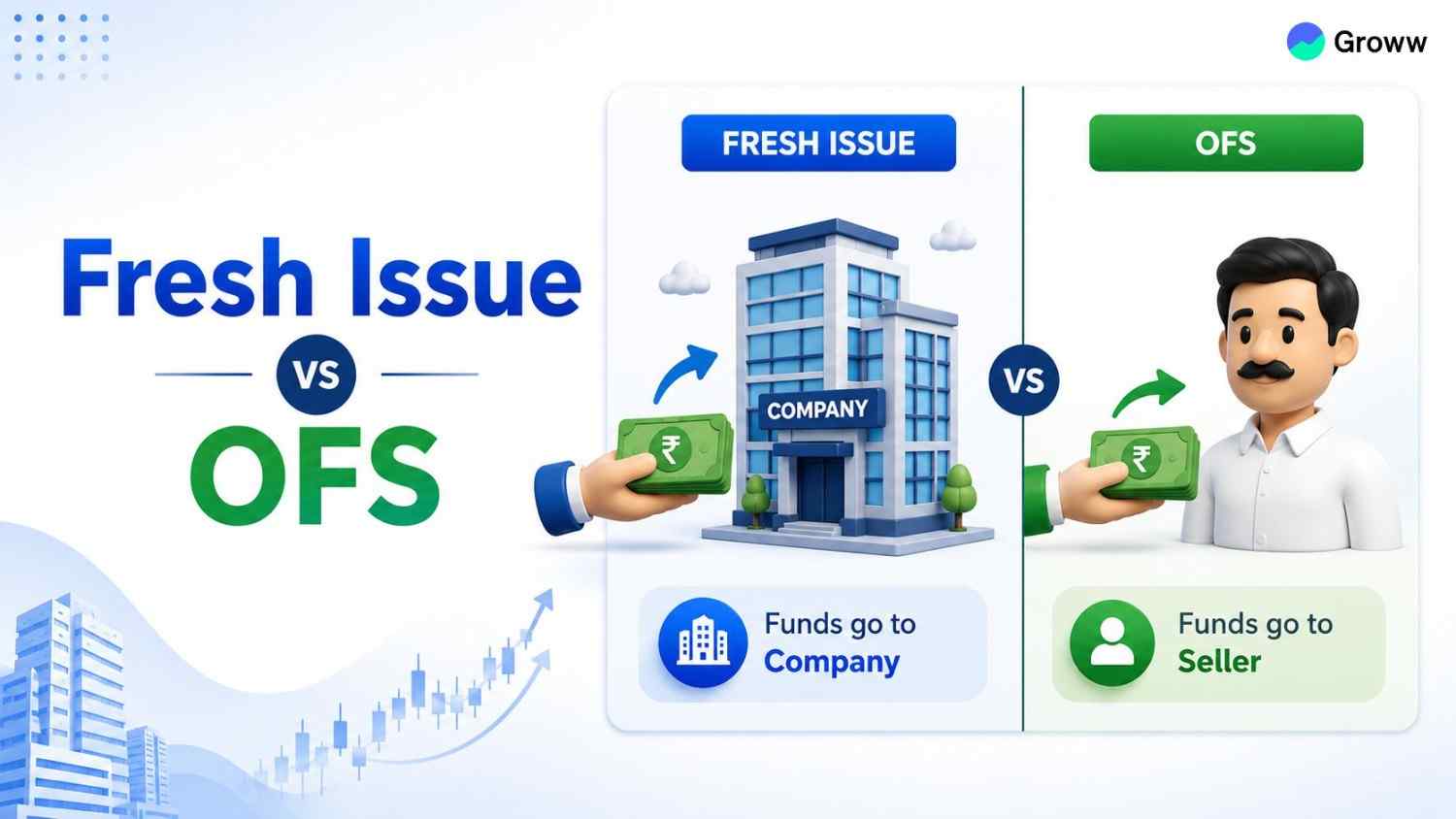

Where Does the Money Go in Fresh Issue vs OFS?

When it comes to the choice between a fresh issue and OFS in IPOs, it is important to understand where the money actually goes. Let’s look at the same below:

Fresh Issue:

- The money directly goes to the company, becoming part of its reserves and paid-up capital.

- The fund allocation takes place as per the Objects of the Issue section in the RHP/DRHP (red herring prospectus or draft red herring prospectus). Typical uses include expansion, debt repayment, working capital and general corporate purposes.

- Existing equity is thus diluted, even as the business is actively being scaled up.

Offer for Sale (OFS):

- In this case, the proceeds go directly to the selling shareholders (early investors or promoters) who cash out, while the company receives nothing.

- This ensures liquidity and a smooth exit route for older investors.

- There is zero impact on the company’s capital structure or internal cash position.

Before you invest, it is always important to check for fresh issue dilution vs OFS in the context of an IPO. You should check the offer breakdown carefully to know exactly who/what you are funding.

This information will be outlined clearly in the Red Herring Prospectus (RHP), and it is available on the official SEBI (Securities and Exchange Board of India) and standard IPO application forms via the broker’s platform.

A heavy focus on fresh issues usually indicates the company’s aggressive expansion, debt reduction, and growth plans. A huge OFS indicates that insiders are using the IPO as an exit strategy to monetise holdings. A 100% OFS IPO will never yield any capital for the company’s future business objectives.

Does Fresh Issue Dilute Shareholding? Does OFS?

You now know the answer to the pertinent question: where does the money go in a fresh issue vs an OFS? It’s important to understand the impact on shareholding across both these types. A fresh issue dilutes the shareholding percentage, while the OFS does not.

The former sees the total number of shares increase, while the proportional ownership of existing shareholders decreases. Yet, for the latter, no new shares are created, and the ownership percentage in the company stays the same. You should check the particular mix of these components for any active IPO by viewing the Objects of the issue section in the SEBI prospectus.

Why Companies Use a Fresh Issue

Companies may use a fresh issue in an IPO to directly raise new capital from the general public. Here are some reasons for the same:

- Growth & Expansion: Companies use fresh issues to raise capital to build new manufacturing facilities or factories, fund capital expenditures, or scale operations into new geographies/markets.

- Repaying Debt: The IPO proceeds are often used to repay existing loans or high-interest debt. This will improve the balance sheet considerably and lower financial risks accordingly.

- R&D: Financing research and development initiatives, the development of new product lines, software and technologies is another reason.

- Working Capital: Funds are often raised to cover day-to-day operational needs and general corporate purposes.

- Acquisitions: Cash reserves may be generated to cover the costs of acquisitions, mergers and strategic partnerships.

A heavy or completely fresh issue is often taken as a sign of investor confidence, signalling that the promoters have confidence in the company's future business prospects.

Why Shareholders Use OFS

Shareholders may use an Offer for Sale (OFS) during an IPO, mainly to cash out, diversify their wealth, and ensure adequate exit liquidity. Here are some reasons worth noting.

- More Efficient Full/Partial Exit: It enables a more straightforward, structured route for larger investors to unlock greater value and book profits. This can be done without undergoing an extensive IPO restructuring process.

- Zero Capital Dilution: Unlike a fresh issue, the OFS will not increase the company's outstanding share count or alter its capital structure. The company's fundamentals and its EPS (earnings per share) base will remain unchanged.

- Regulatory Compliance: Promoters may use OFS to comply with regulatory limits on maximum public shareholding, i.e., SEBI requirements.

- Market Liquidity: By allowing large stakeholders to distribute holdings into the broader market, OFS may help increase the free float of shares. This may enhance overall market visibility in sync with trading volumes.

Is Fresh Issue Better Than OFS for IPO Investors?

When it comes to the offer-for-sale vs fresh issue debate, which one suits you as an investor in an IPO (initial public offering)? Retail investors may often favour a fresh issue, since every rupee raised goes directly into the company/business to build capacity, retire debt or manage working capital requirements. This may often enable higher earnings potential in the future. At the same time, retail investors may feel more confident when they see promoters utilising the funds raised, rather than only selling their own equity.

Yet, an OFS, while not infusing any new funds into the company, is a necessary and standard practice in several scenarios. Under SEBI guidelines, promoters should dilute their holdings to meet the minimum public shareholding (MPS) requirements. It is perfectly natural for private equity funds, venture capitalists and early-stage promoters to partially cash out after backing a business for several years.

Before you focus solely on the ratio, analyse the Objects of the Issue set out in the company’s DRHP (Draft Red Herring Prospectus) on the SEBI portal. If the promoters are fully diluting their stake or reducing it to a nominal percentage, it may be a red flag about their confidence in the company's future.

Yet if they sell only a small portion to ensure market liquidity, that is quite normal. Also, check whether the newly raised funds are being used to repay debt or are solely for speculative expansion.

What Does a Mixed Issue of Fresh Issue + OFS Mean?

A mixed issue in an IPO (initial public offering) combines both an Offer for Sale (OFS) and a Fresh Issue in one offering. The company will thus create and issue new shares, using the proceeds directly to fund business expansion, working capital needs, or debt repayment. It will also use the OFS method to sell shares already held by promoters, founders, and early investors to the general public. They will get this money directly and not the company.

A mixed issue often helps balance the business requirements with the needs of its early financial supporters. The company can raise fresh funds for various purposes, while giving early investors and promoters an exit to book profits. By including an OFS, the company may not have to dilute its equity as much through new shares. This helps safeguard existing EPS (earnings per share) ratios to some extent.

How to Read Fresh Issue and OFS in a DRHP or RHP

Wondering how to read the fresh issue and OFS in DRHP? Here are some steps you can follow.

1. Find the Objects of the Issue section:

- This section helps you understand where the money is going.

- For the fresh issue, the proceeds will directly go into the company’s bank account. Look for specific allocations, such as capital expenditures, setting up new plants, and repaying high-interest debt.

- In the OFS system, the proceeds will go to the selling shareholders, and the company will not get any funds for this portion.

2. Evaluate the Proportions Carefully:

- Most IPOs combine both fresh issues and OFS portions. A balanced ratio may help the company raise capital while allowing a partial exit for early-stage investors.

- Be watchful. If the IPO is a pure OFS, it means the business does not need any new capital and its early backers are simply cashing out.

- A 100% fresh issue may indicate robust expansion plans. However, you should carefully assess the company's execution capabilities.

3. Analyse the Intent of the Promoters:

- If the promoters are selling a large chunk of their stake, it may be a red flag, at times, regarding their confidence in the company’s future prospects.

- If the OFS is mainly from private equity (PE) funds concluding their investment cycles, that is normal and should not be a cause for alarm.

- Read the Capital Structure Section Carefully:

- This comes just after the Objects of the Issue section and shows the pre-IPO and post-IPO share capital data.

- Review this carefully to work out the dilution. A fresh issue increases the total share count and dilutes existing ownership.

- Make sure the anticipated profit growth/revenue from the fresh issue proceeds justifies the dilution in question.

- Watch Out for GCP (General Corporate Purposes):

- In many cases, a large portion of the proceeds from a fresh issue may be allocated to GCP (ambiguous and vague at times).

- Excessively high allocations to GCP (more than 20-30% of the issue size) may be worth watching. This means that the company does not have a proper plan for these funds, thereby offering high flexibility to the management.

Fresh Issue vs OFS: Investor Checklist

Here is a fresh issue vs offer-for-sale checklist that you should keep in mind.

Capital Destination (Fresh Issue)

- Where the money is going (Objects of Offer in the prospectus)

- Prioritise entities using funds for working capital, debt repayment or technological upgrades, among core operations

- Check for a funding gap, i.e. whether the capital raised will be enough to execute the business plan mentioned by the company

Exit Signals (OFS)

- Who is selling- distinction between a partial sell-off by early investors and a full exit by the original company promoters.

- A heavy, majority-OFS structure may indicate that insiders believe the company's valuation has peaked.

- Evaluate the promoter’s post-IPO stake; a retained holding of 50-70% may indicate a strong commitment. Anything less than 30% may indicate a lower long-term alignment with public shareholders.

Valuation and Dilution

- A fresh issue increases the overall share count, which may dilute the EPS (earnings-per-share) unless the new capital generates higher profits (proportionally).

- An OFS does not issue new shares and does not dilute your equity in the future earnings of the company. However, it also offers zero capital to the business.

- Confirm that the price-to-earnings or P/E ratio multiple sought by the entity aligns with its peers in the same industry/sector.

Liquidity & Readiness

- OFS has a role to play in scaling up the public free float. It may improve the stock's liquidity and make it easier to trade (after listing).

- Verify that the OFS adheres to standard corporate governance regulations regarding mandatory lock-in periods and the maximum promoter contribution after listing.

- Review the company’s current Red Herring Prospectus (RHP) through the SEBI database or the regional regulatory authority. This will help you cross-reference the exact ratio of fresh capital to the promoter exits.

IPO OFS vs Stock-Exchange OFS

Do not mistake an IPO OFS for the stock exchange OFS mechanism.

The stock exchange OFS system was established by the Securities and Exchange Board of India (SEBI) and is an exclusive and streamlined trading window on the BSE/NSE. This allows major shareholders of already-listed companies to easily liquidate large blocks of shares.

The company must be a publicly traded entity with ample historical data. This usually works for only a single trading day, leveraging a bidding system and transparent floor pricing rather than a lengthy IPO book-building process.

Promoters sometimes use this system to swiftly reduce their shareholding to comply with regulatory minimum public shareholding (MPS) norms. Retail investors may get a reserved quota (usually 10%) and may frequently bid at a discount, too. Let us examine the core differences below:

|

Key Aspect |

IPO OFS |

Stock Exchange OFS System |

|

Listing Status |

Unlisted (it is a part of the IPO) |

Already listed on the exchange |

|

Bidding Period |

Mostly 3-5 working days |

Usually lasts for 1 trading day |

|

Objective |

Part of the market debut of the company |

Fast-tracking the stake sale by the promoters |

|

Fresh Capital |

None from the OFS part |

None (secondary market transaction) |