Tax Loss Harvesting - Everything You Should Know

Key Takeaways:

- Tax-loss harvesting is a tax-saving strategy that involves selling underperforming assets at a loss to reduce taxable capital gains income.

- Short-term Capital Loss (STCL) can be offset against both STCG and LTCG up to 8 assessment years

- Long-term Capital Loss (LTCL) can be offset against only LTCG up to 8 assessment years

- Use the Groww tax loss harvesting calculator to know the overall summary of your portfolio and how you can save by offsetting capital gains with capital losses.

- To be eligible for tax harvesting, the loss must be booked before “March 31st” of the financial year.

- Capital losses cannot be used to reduce income from other heads such as salary, business, interest, or other income.

- To carry forward capital losses, the ITR must be filed within the due date under Section 139(1). Otherwise, the carry-forward benefit will be lost.

What is Tax-Loss Harvesting (Tax Harvesting)?

Tax-loss harvesting is a tax-saving strategy in which capital losses are offset against capital gains, thereby reducing the total capital gains tax payable.

Here, the investor takes advantage of a red portfolio and sells underperforming assets that are at a loss. Using tax-loss harvesting, the losses from these sales are then used to balance out the gains made from other profitable investments, which results in less taxable income. In some cases, losses can be carried forward to future years to offset future gains.

As per the Union Budget 2024, profits earned from selling equity instruments are subject to two types of capital gains taxes.

- Short-term capital gains (STCG) at 20% if the investment is held for less than one year.

- Long-term capital gains (LTCG) at 12.5% (exempted up to ₹1.25 lakh) if the investment is held for more than 12 months.

Tax-loss harvesting can be used to reduce these tax liabilities. Here's how it works.

How Does Tax Loss Harvesting Work?

Let's understand the working of the tax-loss harvesting strategy with an example.

Mathew invested in two stocks:

Stock X: was bought in May 2024, and he made a profit of ₹80,000 and sold the stock in August 2024.

Since the stock was held for less than a year, ₹80,000 is Mathew’s short-term capital gain (STCG) and is taxed at 20%.

Tax payable: ₹80,000 × 20% = ₹16,000

Stock Y: Mathew bought another stock in May 2024, but it didn’t perform well and is at a loss of ₹50,000. Mathew sold the stock Y after six months. This results in short-term capital loss (STCL).

Tax payable: Zero tax due to loss.

As the tax season is around the corner, Mathew did tax-loss harvesting to save some taxes, as stock Y in his portfolio is at a loss.

|

Tax payable without tax harvesting |

₹16,000 |

|

Tax payable with tax harvesting |

₹6,000 |

Here’s how!

₹50,000 loss from Stock Y is offset against the ₹80,000 gain from Stock X.

This brings taxable capital gain income down to:

₹80,000 - ₹50,000 = ₹30,000

Revised Tax Payable: ₹30,000 × 20% = ₹6,000

Tax Savings: ₹16,000 - ₹6,000 = ₹10,000

In short, Mathew saved ₹10,000 using tax-loss harvesting!

Carry Forward Losses

In the above example, losses were less than gains. (Gains>Losses)

But what if the opposite happens? Losses become more than gains? (Losses>Gains)

Will Tax Loss Harvesting Work?

Yes, it will, as taxpayers are given one more advantage here!

According to the Finance Act 2002, “The capital losses can be carried forward and used to offset future capital gains for up to 8 assessment years.”

This means you have eight assessment years to adjust your unutilised capital losses against any capital gains you earn in the future.

To be eligible to carry forward these losses, taxpayers must file their income tax returns (ITRs) within the due date for the year in which the loss was incurred.

How Does Offsetting Work in Tax-Loss Harvesting?

Offsetting in tax-loss harvesting works differently for STCL and LTCL. Let’s break it down:

|

Type of capital loss |

Can be offset against |

Is carry forward allowed? |

Carry forward period |

|

Short-term Capital Loss (STCL) |

Both STCG and LTCG |

Yes |

Up to 8 assessment years |

|

Long-term Capital Loss (LTCL) |

Only LTCG |

Yes |

Up to 8 assessment years |

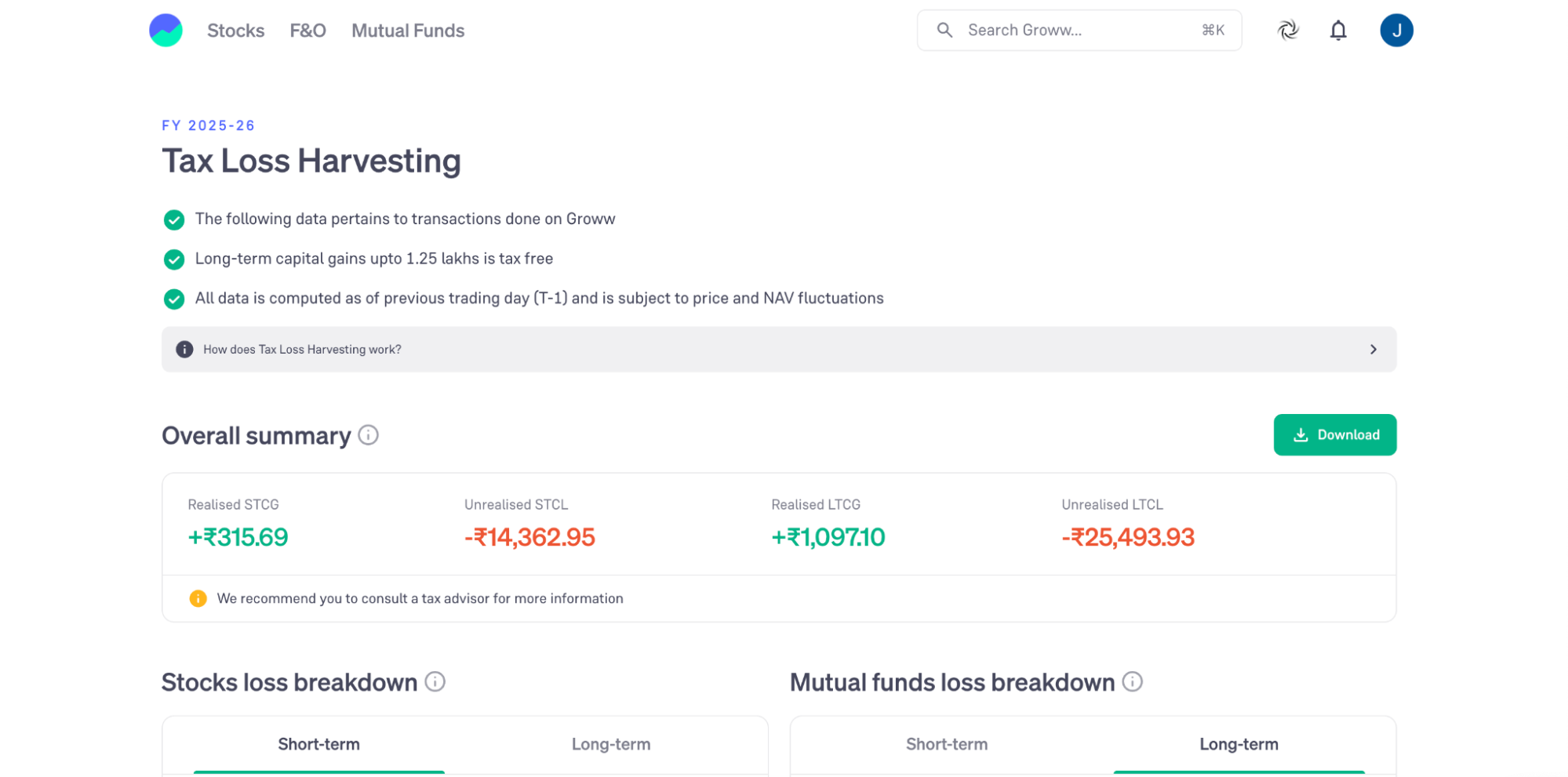

Groww Tax-Loss Harvesting Calculator

At Groww, we have built a tax-loss harvesting calculator that calculates how much tax investors can potentially save by offsetting capital gains with capital losses.

The tool automatically analyses your transactions (both stocks/mutual funds) executed on Groww and provides a clear summary of your realised gains and unrealised losses, both short-term and long-term.

Click here to use the calculator and view the entire summary (as shown in the screenshot below).

Benefits of Tax-Loss Harvesting

Over and above tax savings, individuals can enjoy several benefits with tax-loss harvesting. Read on to know more.

Pay Less Tax

Tax-loss harvesting allows investors to offset their capital gains with capital losses, which ultimately slashes their tax bills.

Carry-Forward Losses

One of the best advantages of tax loss harvesting is that it allows the carry forward of both STCL and LTCL for up to 8 assessment years.

This means that if you’re unable to offset your capital losses against gains in the current financial year, you still have up to 8 years to adjust these losses against future capital gains.

Offsets Both Short-term and Long-term Gains

There is no limitation on offsetting short-term capital loss (STCL) in tax loss harvesting. It can be adjusted against both STCG and LTCG; however, LTCL can only be offset against LTCG.

Rebalance Portfolio

In tax-loss harvesting, you sell your underperforming assets.

This offers a two-fold advantage.

- Firstly, it reduces the tax liability, and

- Allows investors to rebalance their portfolio by investing in better-performing assets.

Essential Considerations of Tax Loss Harvesting

- The timing of selling underperforming assets matters a lot in tax loss harvesting. The loss must be realised before “March 31st” of the financial year. For FY 25-26, it must be done before 31st March, 2026.

- If you have booked the loss and think the stock/fund has long-term potential, you can buy it again. However, it is worth remembering that the holding period will also reset.

- Tax-loss harvesting strategies can get complex; it's better to consult a financial advisor.

- Be mindful of whether the asset is classified as a short-term or long-term investment based on its holding period. This affects the type of capital gain or loss it creates, which in turn determines how it can be offset.

Conclusion

With tax-loss harvesting, you can turn losses into tax-saving opportunities. By strategically offsetting capital losses against gains, taxpayers can minimise tax bills.

But always remember, while saving on taxes is great, long-term wealth creation should always be the goal.

Disclaimer: This blog is solely for educational purposes. The securities/investments quoted here are not recommendatory.

To read the RA disclaimer, please click here