How Does CRISIL Rating Affect Your Fixed Deposit?

Off-late, the interest rate has started moving north, and thus investors are scouting for corporate deposits that provide the best interest rate and come with the highest degree of safety.

But how you do get the safety of such deposits?

For this you have, rating agencies like CRISIL, ICRA, and CARE Ratings to provide an unbiased opinion on the creditworthiness of companies offering the scheme.

The rating step is essential as these deposits are not secured, and there have been instances, in the past, where the issuer was unable to service the interest on time and also failed on the principal repayment.

Also, you must have come across the news that says –

CRISIL rated XYZ company’s fixed deposit at CRISIL FAA. Post announcement, the share price of the stock gets impacted depending on the market expectation.

Have you ever thought about what happened, what is rating, what is CRISIL, and why its rating impacts the price of a stock?

In this blog, we seek to provide you with answers to all such questions.

Let us set the context right by starting with CRISIL and its operations, along with the rating scale.

What is CRISIL?

Established in 1987, CRISIL is India’s first credit rating agency that was promoted by the erstwhile ICICI Ltd along with UTI and other financial institutions.

The service offerings, particularly ratings, catered to investors, lenders, issuers, market intermediaries, and regulators.

In simple language, CRISIL provides information that is required by a varied set of investors to assess the feasibility of credit repayment.

What is CRISIL Rate?

CRISIL is a full-service rating agency, and thus its rating service includes a wide array of debt instruments.

These include a certificate of deposit, bank loans, commercial paper, non-convertible debentures, asset-backed securities, mortgage-backed securities, bonds, fixed deposits, etc.

Is CRISIL’s Rating Limited to Certain Sectors?

No, the CRISIL rating covers all manufacturing companies and service companies, including banks and non-banking finance companies.

Companies can be public sector undertakings, state-government-owned companies, private companies, public limited companies, partnerships, proprietorships, mutual funds, microfinance institutions, urban local bodies, etc.

Role of CRISIL

CRISIL ratings play an invaluable role in assisting issuers and borrowers. The company seeks to bridge the gap between the borrowers and funds while also providing an alternative to funding.

Also, CRISIL’s rating offers the cost of capital benefit to the issuer.

How Does CRISIL’s Rating Impact Depositor?

Investors and lenders rely heavily on CRISIL’s rating before their internal evaluation is completed and before they can arrive at a conclusion.

CRISIL’s rating, in general, is considered a benchmark for the pricing and trading of debt instruments. Also, the ratings provide the regulator’s insights while measuring and managing the credit risk with the lending activity.

Lastly, the ratings are also useful in determining an entity’s capital adequacy (a phenomenon prevalent in the banking sector).

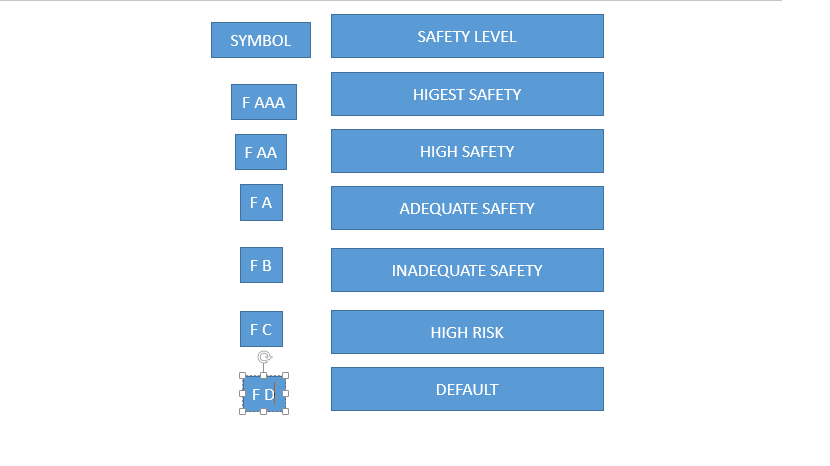

How to Understand the Rating?

The regulator (Securities and Exchange Board of India) has done a great job in ensuring that all the Credit Rating Agencies (CRA) provide a rating on the same scale.

This universal scale helps in more straightforward and more rational benchmarking.

While rating a fixed deposit, CRISIL follows the following rating system-

In addition, CRISIL may add (+) or (-) symbol (for example, CRISIL FAA+) to the rating category mentioned above (applicable only for FAAA to FC).

This symbol indicates the position of a company within the rating category.

Significance of Rating

Rating helps in determining a company’s or a bank’s credibility.

CRISIL rating is generally the first thing that investors look for before investing in any instrument. Ratings assure the timely servicing of the entity’s financial obligations, which defines its credibility.

The ratings, thus, enable an investor to differentiate between high-credit-risk organizations from low credit risk organizations.

For example, HDFC Bank is rated at FAAA by CRISIL, which indicates the high creditworthiness of the bank and the low risk involved with the deposits.

Interest Rate and CRISIL Rating

There is a relation between the interest rate offered and the CRISIL rating. Institutions offering a higher rate are primarily due to low creditworthiness and thus have high risk/low ratings.

Therefore, an institution with a low rating, such as CRISIL FC or CRISIL FB, will typically offer a very high-interest rate to avail funds as the risk involved will be high.

Why CRISIL Ratings?

Investors rely on CRISIL’s ratings because the company provides unbiased and accurate opinions, which an investor can count on for decision-making.

The company implements analytical rigour and utilizes its proprietary framework to arrive at the financial health of any company.

This process helps investors get a clear picture of a company’s strengths and weaknesses.

Lastly, the independent company ensures that the right information is disseminated to the investor at the right time so that actions may be taken accordingly.

The Interest Rate on FD and CRISIL’s Rating

The interest rate offered by banks is also a factor many other factors.

Therefore, there is no direct relation between CRISIL’s rating and the interest rate offered on fixed deposits. However, the rating undoubtedly provides a sense of the degree of safety and interest rate range that can be expected.

Let us now talk about a few examples of the CRISIL FD ratings.

Mahindra and Mahindra Finance

The Mahindra and Mahindra Finance Fixed Deposit have a Crisil rating of ‘FAAA’, which is the highest rating possible.

It, thus, indicates the highest degree of safety with the capital to be invested and minimal risk associated. The company offers an interest rate of 8.75 per cent on its 33-month and 40-month deposits.

Other fixed deposit ratings by CRISIL in the FAAA category are – Bajaj Finserv Limited, Kerala Transport Development Finance Corporation, PNB Housing Finance Limited, HDFC Limited, and Gruh Finance Limited.

Happy Investing!

Disclaimer: This blog is solely for educational purposes. The securities/investments quoted here are not recommendatory.