Bull Put Spread Strategy - Example, Payoff, Greeks & Tax

What is a Bull Put Spread?

A Bull Put Spread is a two-leg options strategy where you sell a put option at a higher strike price (ITM) and simultaneously buy a put option at a lower strike price (OTM), both on the same underlying asset and expiry date. Since the premium received from the sold put exceeds the premium paid for the bought put, the strategy generates a net credit to your account on the day you enter the trade.

This makes the Bull Put Spread a credit spread, which is its defining advantage. Unlike the Bull Call Spread, which requires you to pay a net debit upfront, the Bull Put Spread puts money in your account from day one. Your job is simply to ensure the underlying asset stays above the higher strike price at expiry. If it does, you keep the entire credit as profit.

The strategy is designed for a moderately bullish or neutral market outlook. It works especially well after a sharp market selloff, when put premiums are elevated due to high implied volatility. In those conditions, the credit you collect is significantly larger, giving you a wider buffer before the trade moves into a loss.

Because the premium received from selling the ITM put exceeds the premium paid for the OTM put, the strategy generates a net credit to your account upfront, making it a "credit spread."

For example -

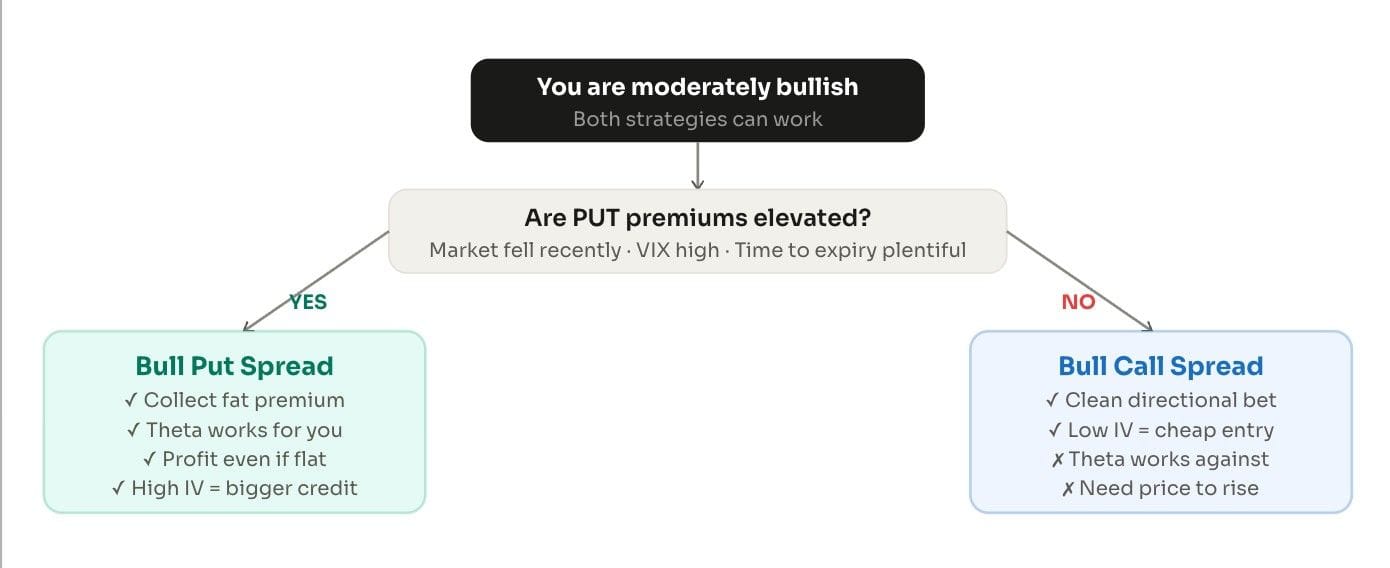

Why Choose a Bull Put Spread Over a Bull Call Spread?

Both the Bull Put Spread and the Bull Call Spread are designed for a moderately bullish view. The question every trader must ask before choosing between them is: are put premiums inflated right now, or are call premiums? The answer to that question determines which strategy puts more money in your pocket.

The Bull Put Spread is executed for a net credit. The Bull Call Spread is executed for a net debit. This means the Bull Put Spread is most attractive when put premiums are swollen, typically after a market selloff, when India VIX is elevated, or when there is significant time remaining to expiry. In those conditions, the ITM put you sell carries an inflated premium. By selling it and using the cheaper OTM put as a hedge, you lock in a large upfront credit with clearly defined risk.

The Core Rule:

Use the Bull Put Spread when put premiums are inflated after a market selloff, when VIX is high, or when there is plenty of time to expiry. Use the Bull Call Spread when call premiums are reasonable, and you want a clean directional bet upward.

You can consider using a Bull Put Spread when -

- The market has recently corrected, and put premiums have spiked

- India VIX is above 18-20

- You expect the asset to remain flat or rise gently, but not necessarily rally hard

- You prefer to receive money upfront rather than pay a debit

- There is adequate time to expiry (15 days or more)

- You want defined risk on both sides of the trade

You can consider using a Bull Call Spread when -

- The market is stable, and you expect a clear directional move upward

- India VIX is low, and call premiums are cheap

- You have a strong conviction that the price will rise above a specific level

- You are comfortable paying a net debit at entry

- Expiry is near, and time decay is less of a concern

How Does the Bull Put Spread Work?

To set up a Bull Put Spread, you execute two trades simultaneously on the same underlying asset with the same expiry date:

- Sell (write) one ITM put option at the higher strike price. (You receive a premium credit for this)

- Buy one OTM put option at the lower strike price. (You pay a premium debit for this)

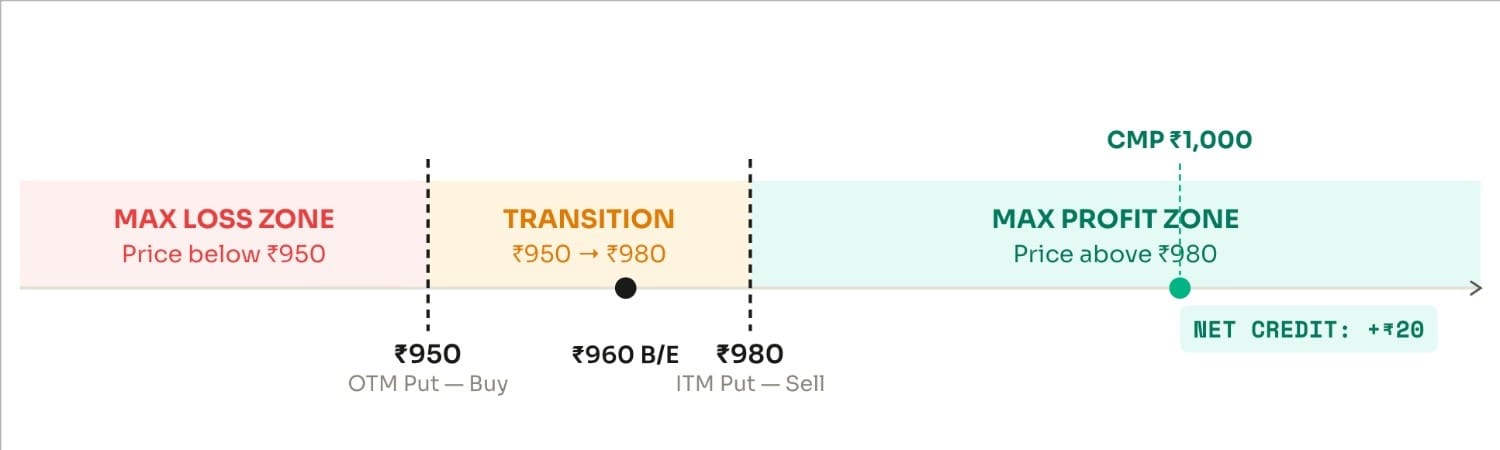

- Net credit = Premium received - Premium paid. (This net credit is your maximum possible profit)

The sold ITM put obligates you to buy the underlying at the higher strike if the buyer exercises. The OTM put you bought is your hedge. It caps your maximum loss at the spread width minus the net credit, regardless of how far the asset falls. This is the key structural advantage over a naked put sale, which carries theoretically unlimited downside.

Consider the following example -

Leg 1: Sell (Write)

ITM Put Option - Higher Strike

Strike = ₹980

Premium Received = +₹30

Leg 2: Buy (Long)

OTM Put Option - Lower Strike

Strike = ₹950

Premium Paid = -₹10

Net Credit = Premium Received - Premium Paid = +₹20

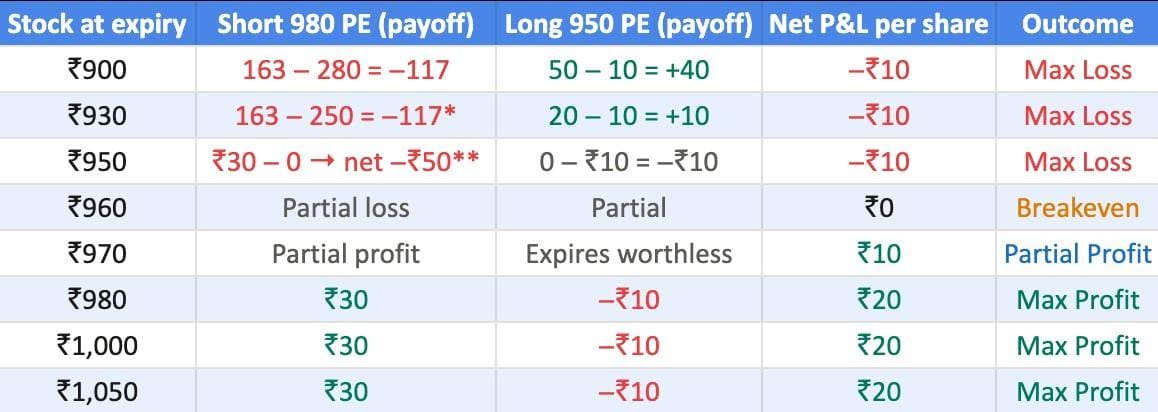

Detailed Example with Full P&L Table

Consider Infosys is trading at ₹1,000. You are moderately bullish after a recent 8% correction and expect the stock to stay above ₹960 for the next 3 weeks. You notice that put premiums are elevated due to the recent volatility. You set up a Bull Put Spread -

Leg 1 - Sell

Strike: ₹980 Put (ITM)

Premium received: ₹30/share

Obligation: To buy shares at ₹980 if exercised

Leg 2 - Buy

Strike: ₹950 Put (OTM)

Premium paid: ₹10/share

Right: To sell shares at ₹950 (your hedge)

Payoff at different expiry prices

Here’s why the loss is capped. Without the long 950 PE, selling the 980 PE naked would expose you to unlimited downside (theoretically, if the stock fell to ₹0, you'd lose ₹980/share minus premium). They bought 950 PE. It acts as insurance, capping your loss at the spread width minus the net credit, regardless of how far the stock falls.

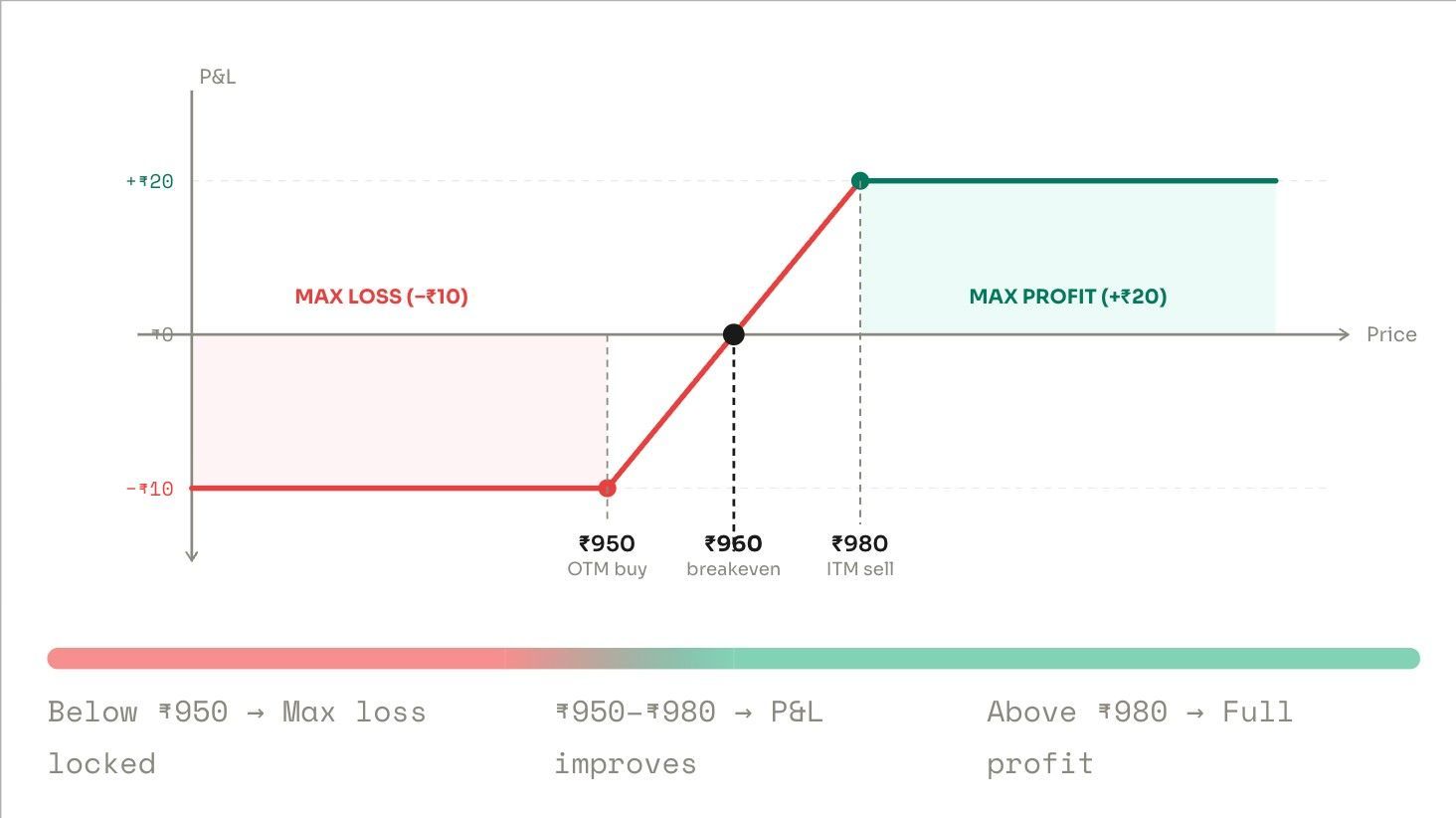

Payoff Diagram

The payoff curve shows three distinct zones: a flat floor (max loss), a rising diagonal as price moves from the lower to higher strike, and a flat ceiling (max profit). This "truncated profit" shape is the hallmark of all vertical credit spreads.

Notice that once the stock price exceeds ₹980, the profit no longer increases; it remains flat at +₹20. This is because the premium received on the sold ITM put is the upper limit of the profit. The strategy does not benefit from further price increases beyond the short put strike. This is the trade-off you accept in exchange for receiving the credit upfront.

Strike Selection

The strikes you choose define everything about the trade, i.e., your maximum profit, maximum loss, breakeven level, and probability of success.

The relationship is straightforward: the wider the spread (the further apart the two strikes), the higher the credit you collect and the higher your potential profit. However, a wider spread also means a higher maximum loss and a breakeven that is further below the current price.

A narrow spread is conservative. You collect less credit, but the maximum loss is small, and the position is easier to defend if the market moves against you.

A wide spread is aggressive. You collect more credit but accept a larger maximum loss. Choose based on your conviction level: narrow spread for low conviction, wide spread for high conviction.

Assume, spot price = ₹7,612 (Nifty)

Strike Selection Rule of Thumb for Indian Markets

Short put (sell): Consider placing 1-2% below the current market price for a standard moderately bullish setup. For the ATM maximum credit, place at the current price. However, this significantly increases risk.

Long put (buy): Consider placing 3-5% below the short put strike for standard protection. A wider gap between the two strikes gives you more credit but also increases your maximum loss proportionally.

Liquidity check: Always verify that both strikes have open interest above 1,000 contracts and a bid-ask spread below ₹3. Also, avoid illiquid strikes where the execution price will be significantly worse than the mid-price.

Impact of Greeks: Theta, Vega, Delta and Gamma

The four major options Greeks - Theta, Vega, Delta, and Gamma. Each affects your Bull Put Spread differently. Understanding these effects helps you time your entry, manage the trade mid-flight, and decide when to close. Unlike a single-leg position, a spread has both a long and a short option, so the Greek effects partially cancel each other out. The net impact is what matters.

Theta - Time Decay

Time Decay works in your favour. As each day passes, both put options lose time value. You sold the more expensive ITM put and bought the cheaper OTM put. The ITM puts decay faster in absolute terms, so the net value of your position decreases, which is exactly what you want as the position holder of a net short spread.

If the stock stays flat for two weeks, you still profit. The passage of time alone moves the trade toward its maximum profit. This is the opposite of a debit spread, where time decay hurts you every day

Vega - Implied Volatility

Falling implied volatility (IV) benefits you. High implied volatility at entry means inflated premiums where you collect a larger net credit. After the event that caused volatility (a rate decision, earnings, or a global shock), IV typically drops. When IV falls, the premiums on both options shrink. Since you are net short premium on the spread, the falling IV reduces the spread's value, benefiting you.

Enter the Bull Put Spread when VIX is above its 30-day average. Avoid entering when the VIX is near multi-year lows, as premiums will be thin and not worth the risk.

Delta - Directional Exposure

The overall position has a positive delta, meaning you benefit when the underlying asset rises. The short ITM put has a large negative delta; the long OTM put has a smaller negative delta. The net delta of the spread is positive, meaning the position behaves like a modestly bullish bet.

You do not need a big rally. Even a flat or slightly rising market is enough to achieve maximum profit. As the underlying rises above the short put strike, the net delta approaches zero, making the position delta-neutral.

Gamma - Rate of Delta Change

Gamma measures how fast delta changes as the underlying moves. In the final 5-7 days before expiry, gamma generally accelerates sharply. If the stock falls toward your short put strike in those final days, the delta of your position can shift dramatically, turning a profitable trade into a loss very quickly.

Do not hold Bull Put Spreads through the final week unless you are confident the market will not move against you. The best practice could be to close when 70-80% of the maximum profit has been achieved. This eliminates gamma risk and frees capital for the next trade.

IV vs Theta Impact on Bull Put Spread

Here’s an illustration of implied volatility vs Theta impact on a Bull Put Spread -

When to Use the Bull Put Spread

You can consider using the bull put spread when -

- The market has recently sold off, and you expect it to stabilise or recover

- India VIX is above 18, and put premiums are elevated and worth selling

- You are moderately bullish, and you do not expect a sharp or dramatic rally

- You want to earn income from a range-bound or gradually rising market

- There are 15 days or more to expiry, so the sold put carries meaningful time value

- You want a fully defined risk trade where both maximum profit and maximum loss are fixed at entry

- You have identified a clear technical support level below the short put strike

When to Avoid the Bull Put Spread

You can consider avoiding the bull put spread when -

- You have a bearish or strongly negative view of the underlying asset

- India VIX is at multi-year lows, and put premiums are too thin to justify the risk

- You expect a large, sharp rally where a long call or bull call spread could profit more

- A major binary event (budget, general election results, RBI emergency meeting) is within a span of a couple of days

- You are in the final few days before expiry, and the position has not reached a profit, and the gamma risk is extreme

- The underlying has low open interest or wide bid-ask spreads in the options chain

Real-Life Scenarios for Indian Market Traders

The Bull Put Spread is particularly well-suited to the recurring patterns of Indian equity markets. These four scenarios represent the most common and reliable entry opportunities that traders encounter:

Scenario 1: Post-Market Selloff

Situation: Assume that Nifty has fallen 4-6% over three consecutive sessions amid weak global cues such as a US Fed surprise, a banking crisis abroad, or a commodity price shock. Put premiums spike as retail traders rush to buy protection. India VIX jumps from 14 to 22 within a week.

Why this works: After a sharp but non-fundamental selloff, markets often stabilise over the following two to three weeks. The elevated put premiums mean you collect a large credit. The VIX drop that typically follows the recovery amplifies your gain through volatility crush.

Possible Action: You can consider selling an ITM put 2-3% below the current depressed price and buying an OTM put 3-5% further below, as protection could help. Also, you can collect the elevated credit and consider holding for 10-14 days in such cases.

Scenario 2: RBI Policy Week

Situation: The RBI Monetary Policy Committee meets in five days. The market is cautious, and IV has risen modestly. You expect no surprise rate hike and believe Nifty Bank will hold its major support level at a round number.

Why this works: Pre-event IV is elevated but not extreme. Once the RBI statement is released and there is no negative surprise, IV drops sharply, indicating a classic volatility crush. This drops the value of the spread, creating profit for the credit spread holder.

Possible Action: You can consider entering the Bull Put Spread three to four days before the policy date and place the short put below the key support level. However, plan to close the position within 24 hours of the announcement to capture the IV crush.

Scenario 3: Quality Stock Post-Earnings Dip

Situation: Assume that HDFC Bank reports its quarterly results. Revenue and profit have beat estimates, but the management commentary on margins is slightly cautious. The stock drops 7% in reaction, which is an overreaction relative to the actual numbers. The stock is now at a historically strong support zone.

Why this works: The earnings-driven IV spike has inflated put premiums to unusually high levels. The overreaction has placed the stock at a level where fundamental buyers typically step in. The combination of cheap-to-defend support and inflated premiums is a classic Bull Put Spread setup.

Possible Action: You could consider selling the ITM put at or just below the current depressed price and buying the OTM put as protection in such a scenario. The IV crush after the earnings event, along with the price recovery, could both work in your favour.

Scenario 4: Sustained High VIX Environment

Situation: India VIX has been above 22 for two consecutive weeks due to a geopolitical escalation or global macro concerns, and the put premiums are 2-3 times their normal levels. The market has stopped falling and is holding a range. However, the confidence is low

Why this works: A sustained high-VIX environment is tailor-made for credit spreads. The premium you collect is enormous relative to normal conditions. Even if the market oscillates, the wide credit buffer means you have a large margin of safety before reaching the breakeven.

Action: You could run a series of monthly or bi-weekly Bull Put Spreads, each time collecting the elevated credit. However, ensure that you are not tempted to widen spreads excessively, as the goal is consistent income with defined risk, not a leveraged bet on the market holding.

A Complete Nifty 50 Trade Example

The following is a realistic trade example based on a common Nifty setup. The specific dates and exact premiums are illustrative, but the structure, logic, and calculations reflect real market conditions. Use this as a reference for how to plan and evaluate an actual Bull Put Spread trade on Nifty.

Underlying: Nifty 50

India VIX: 21.4 (elevated)

Nifty CMP (current market price): 24,300

Outlook: Moderately bullish

Expiry: Monthly (next month)

Entry Date: 15 days before expiry

Lot size: 75 units per lot

Consider the following trade setup -

|

Leg |

Option |

Strike |

Premium |

Cash flow |

|

Leg 1 - Sell |

Nifty 24,000 PE |

24,000 (ITM) |

+₹155/unit received |

CREDIT |

|

Leg 2 - Buy |

Nifty 23,700 PE |

23,700 (OTM) |

-₹65/unit paid |

DEBIT |

So,

Net credit per unit = ₹155 - ₹65 = ₹90

Nifty lot size = 75 units per lot

Total credit per lot = ₹90 × 75 = ₹6,750

Spread width = 24,000 - 23,700 = 300 points

Maximum loss per unit = 300 - 90 = ₹210

Total maximum loss per lot = ₹210 × 75 = ₹15,750

Breakeven point = 24,000 - 90 = 23,910

Risk-reward ratio = ₹90 reward : ₹210 risk = 1 : 2.3

Here are the possible outcomes -

|

Nifty at expiry |

Net P&L per unit |

P&L on one lot (75 units) |

Verdict |

|

Below 23,700 |

-₹210 |

-₹15,750 |

|

|

23,800 |

-₹110 |

-₹8,250 |

|

|

23,910 (breakeven) |

₹0 |

₹0 |

|

|

24,000 or above |

+₹90 |

+₹6,750 |

|

Bull Put Spread Compared to Other Strategies

The Bull Put Spread sits in a specific niche: it earns income like a naked put but with defined, capped downside. Understanding how it compares to similar strategies helps you choose the right tool for each market condition.

|

Strategy |

Cash Flow |

Max Profit |

Max Loss |

Theta |

Best used when |

|

Bull Put Spread |

Net credit received |

Net credit (capped) |

Spread - credit |

Positive |

High IV, moderately bullish, and want an income |

|

Net debit paid |

Spread - debit |

Net debit |

Negative |

Low IV, expecting a clear price rise |

|

|

Long Call |

Net debit paid |

Unlimited upside |

Premium paid |

Negative |

Very bullish, expect a sharp, rapid rally |

|

Naked Put Sell |

Large credit |

Premium received |

Unlimited |

Positive |

High IV, strongly bullish, large capital available |

|

Cash-Secured Put |

Credit + cash block |

Premium received |

Strike - premium |

Positive |

Want to acquire the stock at a lower price |

|

Covered Call |

Credit (hold stock) |

Premium + limited up |

Full stock downside |

Positive |

Already own stock, slightly bullish or neutral |

The Bull Put Spread's unique advantage is combining the credit-receiving benefit of a naked put with a fully defined, capped downside. A naked put earns more but exposes you to catastrophic loss if the stock collapses. The Bull Put Spread sacrifices some credit in exchange for the peace of mind that your maximum loss is fixed and known from the moment you enter the trade.

Advanced Variations of the Bull Put Spread

ATM Bull Put Spread

The standard Bull Put Spread uses an ITM short put and an OTM long put. However, you can place the short put at the money, i.e., at the current market price, to collect the maximum possible credit. The trade-off is that the short put is immediately at risk if the market falls even one point. Use this variation only when you have a strong conviction on a specific support level and want the highest possible credit.

Diagonal Bull Put Spread

In a diagonal Bull Put Spread, you buy a longer-dated OTM put for protection and sell a shorter-dated ITM put to collect income. The near-term sold put decays faster than the long-dated protective put. When the near-term put expires, you sell another short-dated ITM put against the same long put. This allows you to accumulate multiple credits against a single protective leg over time.

Rolling the Spread

Rolling is the act of closing your current Bull Put Spread and immediately opening a new one with adjusted parameters. It is your primary risk management tool when the trade moves against you.

Bull Put Spread + Covered Call

If you own the underlying stock, you can combine a Bull Put Spread below the current price with a covered call above the current price. The Bull Put Spread provides limited downside protection; the covered call generates additional premium income above. The combined position profits as long as the stock stays within a defined range, which is ideal during low-volatility consolidation phases after a run-up.

Tax Implications

Profits from the Bull Put Spread, like all F&O options trading, are classified as non-speculative business income under Section 43(5) of the Income Tax Act. They are not taxed as capital gains. This has significant implications for how you report income, how you set off losses, and whether a tax audit applies to you.

|

Tax Aspect |

Treatment for F&O Options Traders |

|

Income classification |

Non-speculative business income under Section 43(5) of the Income Tax Act. It is NOT short-term or long-term capital gains. |

|

Tax rate |

Your net F&O profit is added to your total income from all sources and taxed at the applicable income tax slab rate |

|

Loss set-off |

F&O losses can be set off against other non-speculative business income in the same year. Remaining losses can be carried forward for 8 financial years to set off against future non-speculative business income. |

|

Turnover calculation |

Turnover for F&O is the absolute sum of all positive and negative differences on trades, plus the premium received on options sold. This is used to determine whether a tax audit is applicable. |

|

Tax audit (Section 44AB) |

A tax audit is required if: (a) your F&O turnover exceeds ₹10 crore, OR (b) your turnover is below ₹10 crore, but your declared profit is less than 6% of turnover, AND your total income exceeds the basic exemption limit. |

|

Deductible expenses |

Brokerage commissions, STT, transaction charges, internet costs, advisory fees, and any other expense directly related to F&O trading can be deducted from income before calculating tax. |

|

GST |

GST is not payable on trading profits. GST is applicable to brokerage and transaction charges paid to your broker. |

|

ITR form |

Use ITR-3 if you have F&O income in addition to salary or other income. Maintain a trading ledger as your books of accounts. |

Disclaimer: F&O taxation in India has specific rules that vary based on your other income sources, turnover, and trading patterns. The information above is for general guidance only and does not constitute professional tax advice. Consult a qualified Chartered Accountant before filing your return if you have F&O income.

Risks and Common Mistakes to Avoid

- Holding through an earnings announcement without a specific plan

A single bad quarterly result can gap the stock through both strikes in minutes. Before entering any Bull Put Spread, check the earnings calendar. If results are due within your holding period, either avoid the trade or close the position before results are announced. - Not accounting for the early assignment of stock options

Index options (Nifty, Nifty Bank, and Finnifty) are European-style and cannot be exercised before expiry. However, individual stock options in India are American-style and can be exercised early if the short put is deep in the money and close to a dividend record date. Monitor deep ITM stock option positions carefully. - Sizing the spread based on the credit amount rather than the maximum loss

A wide spread looks attractive because it offers a higher credit. But the maximum loss is proportionally larger. Always size the trade based on the percentage of your trading capital you are willing to lose on this one position, not on how large the credit looks. - Entering into illiquid options

Both legs of the spread must have adequate open interest and a tight bid-ask spread. If the bid-ask spread on either leg is wider than ₹3-5, you could lose money on entry and again on exit. You can consider sticking to the most liquid underlying assets, such as Nifty 50, Nifty Bank, Finnifty, and the top 20 Nifty 50 individual stocks. - Refusing to take the maximum loss and hoping for a recovery

Once both strikes are breached at expiry, the maximum loss is locked in. There is no recovery. Recognising when the original thesis is wrong and exiting early, even at a partial loss, is better than holding through a maximum loss. Consider setting a stop-loss at 2x the credit received and respecting it.

Conclusion

The Bull Put Spread is one of the most practical strategies available to the moderately bullish Indian options trader. By selling an ITM put and buying an OTM put as a hedge, you collect a net credit upfront, benefit from time decay every day, and limit your maximum loss to a fixed amount known at entry. You do not need the market to rally. You simply need it to hold above your short put strike.

The strategy is most powerful in elevated-volatility environments such as after a selloff, around major policy events, or during sustained high-VIX periods when put premiums are bloated. In those conditions, the credit you collect is large, the buffer before breakeven is wide, and the subsequent drop in volatility accelerates your path to maximum profit.

Before implementing the Bull Put Spread, ensure you have selected liquid strikes with a tight bid-ask spread, sized the position based on your maximum acceptable loss rather than the credit amount, and identified the conditions under which you will exit, whether that is capturing 70-80% of the maximum profit, hitting a stop-loss at 2x the credit received, or closing before a major event. With these guardrails in place, the Bull Put Spread is a consistent, income-generating strategy suited to experienced and novice traders alike.