PMS vs Mutual Fund: Key Difference, Risk, Returns, Fees & Tax

Mutual funds are better suited for most investors because they are accessible, diversified, SIP-friendly and easier to manage. Portfolio Management Services (PMS) may be suitable for HNIs and other eligible investors who can invest a minimum of ₹50 lakh, want a customised portfolio, and can handle higher risk, higher fees and tax complexity. For many investors, mutual funds work best as the core portfolio, while PMS may be used as a limited satellite allocation.

Key Takeaways

- PMS is generally meant for HNIs and eligible investors.

- Mutual funds are suitable for beginners, retail investors, SIP investors, HNIs and institutions.

- SEBI states that a PMS has a minimum investment requirement of ₹ 50 lakh.

- Mutual funds enable small-ticket investing and are better suited to SIP-based investing.

- PMS may offer customisation and direct ownership of securities.

- Mutual funds offer pooled, diversified exposure through units of a scheme.

- PMS may carry a higher concentration risk, manager risk, fee complexity and tax-reporting burden.

- Mutual funds are usually better for core portfolio allocation.

- PMS may be useful as a satellite allocation for investors who need customisation.

What is PMS?

Portfolio Management Services, or PMS, is a professional investment management service in which a portfolio manager manages an investor's money based on their financial goals, risk appetite, and agreed investment mandate. PMS is generally designed for HNIs who want a more personalised investment approach than mutual funds.

SEBI mandates that PMS providers hold stocks and other assets in the investor’s name, unlike mutual funds, where money is pooled in a shared fund.

Types of PMS

There are three main types of PMS in India:

| Type of PMS | Meaning |

|---|---|

| Discretionary PMS | The portfolio manager takes investment decisions on behalf of the investor. |

| Non-discretionary PMS | The manager gives recommendations, but the investor makes the final decision. |

| Advisory PMS | The manager gives investment advice, but the investor executes transactions independently. |

SEBI classifies PMS into discretionary, non-discretionary and advisory PMS based on the level of decision-making control retained by the investor.

Read more: Difference Between Discretionary PMS, Non-Discretionary PMS, and Advisory PMS

What are Mutual Funds?

A mutual fund is a pooled investment product where money from many investors is collected and invested in assets such as equities, bonds, government securities and money market instruments. The portfolio is managed by a professional fund manager according to the scheme’s investment objective. AMFI states that mutual funds pool money from multiple investors and distribute income or gains proportionately after expenses and levies through the scheme’s NAV.

When you invest in a mutual fund, you receive units of the scheme. The value of these units is represented by the scheme’s Net Asset Value, or NAV. AMFI explains that NAV is the market value of securities in a scheme divided by the total number of units, and mutual fund NAVs are published daily on mutual fund and AMFI websites.

Types of Mutual Funds

Investors can invest in several types of mutual funds depending on their investment objectives and risk profile. Here are some of the different types of mutual funds:

Should You Go for One or Both of Them?

MFs and PMS are both guided investment tools that can help you buy stocks in the same general market. But both have very different approaches. In an MF, you can see a wider variety of stocks, sometimes more than 40-50. And because there are so many options, one can always choose the scheme as per one’s risk appetite and long-term financial goals.

On the other hand, PMS is much more curated in terms of taste and goals but is much costlier to operate and manage. Generally, PMS portfolios do not have more than 20-30 stocks at one time. Moreover, PMS is usually tailored per the investor’s preferences to let the investors have more control over the composition of the portfolio than MFs. They also have fewer regulatory controls compared to MFs, making them riskier; however, their returns are much greater for the same reason.

The critical point here is that the lowest investment limit in PMS is Rs 50 lakh, so they remain out of reach for most investors.

PMS allows portfolio customisation based on your risk profile and financial needs. Also, they are more flexible when it comes to investment. And that’s why PMS portfolios are more likely to outperform the markets and bring in better returns.

Furthermore, PMS investment only needs to disclose information to the client; the same data is not available to the general public. But the same also makes it harder for one to compare other PMS products. On the contrary, all the data about MFs is public, making it much more transparent.

And even though PMS may offer high returns, they also attract higher fees and taxes.

So, now the question is, should you invest in PMS vs. mutual funds?

This will depend on your investment corpus, risk appetite, and financial goals. If you have a small corpus and do not wish for extensive tax compliance, MFs could be your option. On the other hand, if your corpus runs into 6/7 digits, demands customisation, and more, PMS could be your best bet.

Let us say you have Rs 1 crore to invest. Now, you could invest in one PMS scheme and multiple MF schemes together, barring low-value MF schemes. This can help you maximise your chances of making a profit from both these investment areas.

PMS vs Mutual Fund: Quick Comparison Table

| Factor | PMS | Mutual Fund |

|---|---|---|

| Full form | Portfolio Management Services | Mutual Fund |

| Structure | Individually managed portfolio | Pooled investment scheme |

| Regulator | SEBI | SEBI |

| Minimum investment | ₹50 lakh | Usually much lower; varies by scheme/platform |

| Investor type | HNIs, experienced investors | Beginners, retail investors, HNIs, institutions |

| Ownership | Direct ownership of securities in many PMS structures | Units of a mutual fund scheme |

| Customization | High | Low |

| SIP suitability | Usually not designed for small SIPs | Highly SIP-friendly |

| Diversification | Can be concentrated | Usually more diversified |

| Fees | Management fee, performance fee and other charges | TER/expense ratio |

| Taxation | Transaction-level taxation for investor | Unit-level taxation on redemption/switch |

| Liquidity | Depends on PMS terms and holdings | Usually easier in open-ended schemes |

| Transparency | Holding-level visibility | Scheme-level disclosure |

| Best role | Satellite/customized allocation | Core portfolio allocation |

Key Differences Between PMS and Mutual Funds

1. Investment Structure

In PMS, the investor generally has an individual portfolio managed according to a specific mandate. The portfolio may be tailored to the investor’s goals, risk profile and preferences. This makes PMS more personalized than a mutual fund.

In mutual funds, money from many investors is pooled into one scheme. Every investor in the same scheme gets exposure to the same portfolio in proportion to the units held. Mutual funds are therefore more standardized and easier to scale.

2. Minimum Investment

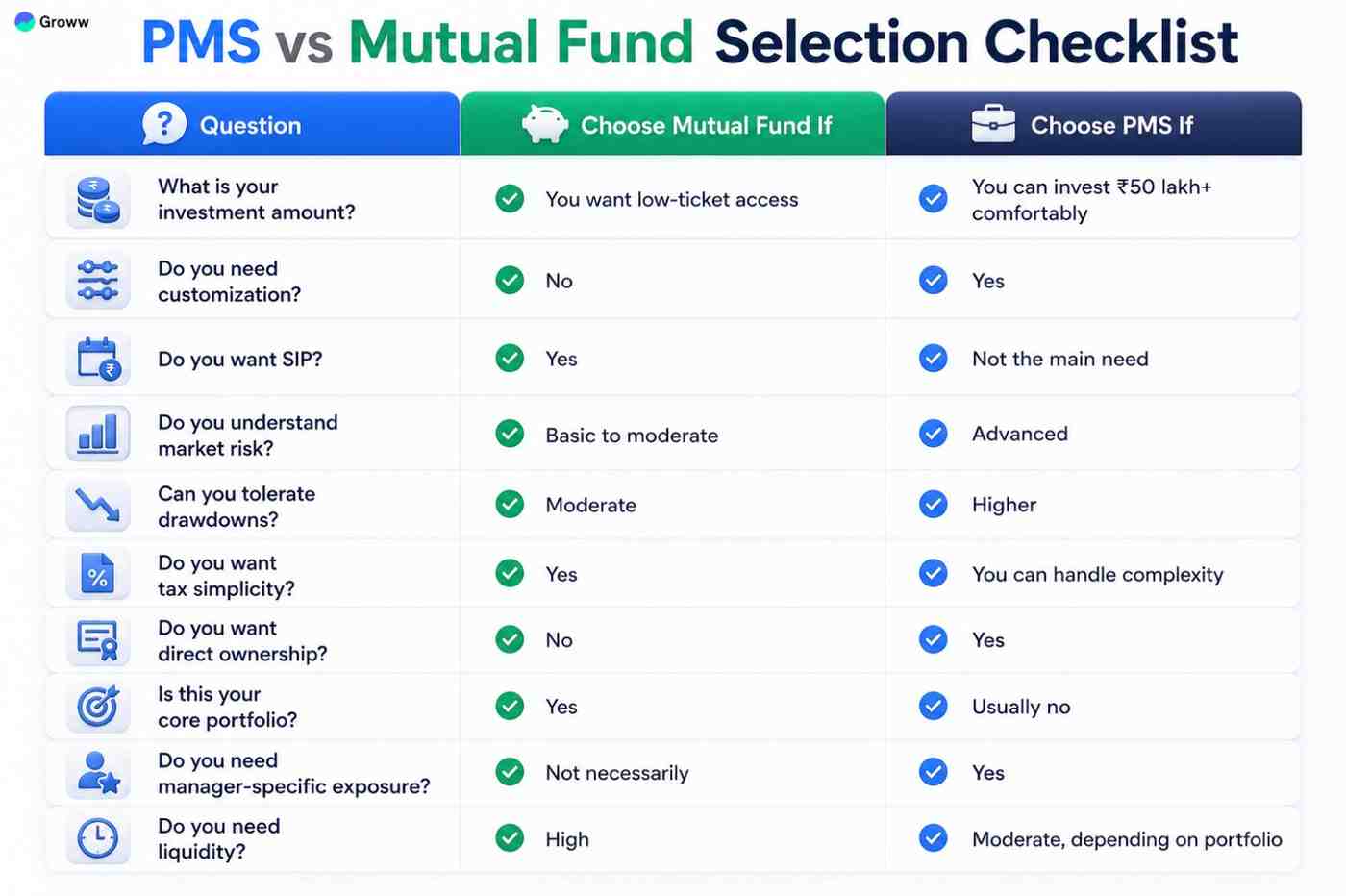

The minimum investment requirement is one of the biggest differences between PMS and mutual funds. SEBI states that PMS has a ₹50 lakh minimum investment requirement, which makes it more suitable for HNIs and investors with larger portfolios.

Mutual funds have a much lower entry barrier. Investors can usually start with small lump-sum amounts or SIPs, depending on the scheme and platform. AMFI also notes that mutual funds are suitable for investors who want to invest small amounts and do not have the time or expertise to invest directly in stock markets.

3. Customization

PMS can offer portfolio-level customization. Depending on the provider and strategy, the portfolio may reflect investor preferences, risk tolerance, sector restrictions, tax considerations or specific mandates.

Mutual funds do not offer investor-level customization. Every investor in the same mutual fund scheme follows the same scheme objective and portfolio strategy. This simplicity is also one of the reasons mutual funds are easier for retail investors.

4. Ownership of Securities

In PMS, the investor may directly own the underlying stocks or securities. This can give the investor holding-level visibility and a more personalized investment experience. SEBI highlights direct ownership as a key structural difference between PMS and mutual funds.

In mutual funds, the investor owns units of the scheme. The underlying securities are held by the mutual fund scheme, and the investor’s value is reflected through NAV.

5. Risk and Diversification

PMS portfolios can be more concentrated than mutual funds. A focused portfolio may generate strong returns when the strategy works, but it can also lead to higher drawdowns when a few holdings underperform. SEBI lists market risk, concentration risk, liquidity risk and managerial risk as key risks associated with PMS.

Mutual funds are generally more diversified, especially broad-based equity, hybrid, debt and index funds. However, not all mutual funds are low risk. Sectoral, thematic, small-cap and credit-risk funds can also carry high risk.

6. Fees and Costs

PMS fee structures can include fixed management fees, performance fees, brokerage, custody charges, exit charges and other operational costs. SEBI notes that PMS typically involves higher management and performance fees compared with mutual funds.

Mutual fund costs are mainly reflected through the Total Expense Ratio, or TER. AMFI’s TER disclosure page notes that direct plans have a lower expense ratio because they exclude distribution expenses and commissions.

7. Returns

PMS may offer differentiated return potential because it can run focused, customized or manager-led strategies. However, PMS returns can vary based on manager skill, portfolio concentration, market cycle, fees, taxes and the investor’s entry timing.

Mutual fund returns are easier to compare because schemes are grouped into categories and benchmarked publicly. Mutual fund investors can compare rolling returns, category returns, fund manager history, TER, AUM and risk metrics more easily.

8. Taxation

Taxation is an important difference between PMS and mutual funds.

In PMS, because the investor may directly own securities, tax events can arise whenever securities are sold in the investor’s portfolio. This means PMS taxation can be transaction-level and more complex.

In mutual funds, tax is generally triggered when investors redeem, switch or transfer units. For equity-oriented fund units, the Income Tax Department states that short-term capital gains on transfers on or after July 23, 2024 are taxed at 20%, subject to conditions such as STT. Long-term capital gains under Section 112A on listed equity shares, units of equity-oriented funds and units of business trusts are taxed at 12.5% on gains above ₹1.25 lakh for transfers on or after July 23, 2024.

For specified mutual fund units acquired on or after April 1, 2023, Section 50AA provides that gains from transfer, redemption or maturity are deemed to be gains from a short-term capital asset.

9. Liquidity

PMS liquidity depends on the PMS agreement, portfolio holdings and the type of securities held. A PMS portfolio holding liquid large-cap stocks may be easier to exit than one holding less liquid small-cap or concentrated positions.

Open-ended mutual funds generally offer easier redemption. However, mutual fund liquidity also depends on the scheme type, exit load, settlement timeline and market conditions. AMFI explains that mutual fund redemption price is based on applicable NAV adjusted for exit load, if applicable.

10. Transparency and Reporting

PMS can provide investor-level portfolio reports, including actual holdings, transactions and portfolio-level performance. This can be useful for investors who want direct visibility into what they own.

Mutual funds provide standardized scheme-level disclosure such as NAV, factsheets, portfolio holdings, TER and benchmark performance. NAV is declared at the end of each trading day after market close, according to AMFI.

PMS vs Mutual Fund: Which Is Better?

There is no universal winner. The better option depends on investor profile, investment amount, risk appetite, goals and need for customization.

| Investor Need | Better Option | Why |

|---|---|---|

| Beginner investing | Mutual Fund | Easier, lower-ticket, diversified |

| SIP-based investing | Mutual Fund | Designed for regular monthly investing |

| Goal-based investing | Mutual Fund | Easier to map to goals |

| Customized portfolio | PMS | More personalization |

| Direct security ownership | PMS | Investor may own securities directly |

| Low-cost investing | Mutual Fund | Simpler and usually lower cost |

| Concentrated portfolio exposure | PMS | Focused strategies possible |

| Tax simplicity | Mutual Fund | Easier reporting in most cases |

| Core portfolio | Mutual Fund | Better suited for broad allocation |

| HNI satellite allocation | PMS |

Can complement core portfolio |

When Should You Choose Mutual Funds Over PMS?

Mutual funds may be more suitable if:

- You are a beginner investor.

- You want to invest through SIPs.

- You have less than ₹50 lakh available for this allocation.

- You want simple diversification.

- You want lower cost and easier tracking.

- You want simpler tax reporting.

- You are investing for long-term goals like retirement, children’s education or wealth creation.

- You do not need portfolio customization.

- You want liquidity through open-ended funds.

- You want a core portfolio product.

For most retail investors and salaried investors, mutual funds are usually the better starting point because they are easier to understand, easier to diversify and more suitable for disciplined monthly investing.

When Should You Choose PMS Over Mutual Funds?

PMS may be more suitable if:

- You are an HNI or experienced investor.

- You can comfortably invest ₹50 lakh or more.

- You want a customized portfolio.

- You want direct ownership of securities.

- You are comfortable with portfolio concentration.

- You can tolerate market volatility and drawdowns.

- You can evaluate portfolio manager quality.

- You understand PMS fee structures.

- You can handle more complex tax reporting.

- You want a satellite allocation beyond mutual funds.

PMS should not be selected only because it sounds premium. The investor should understand the strategy, costs, risks, liquidity and tax implications before investing.

Can You Invest in Both PMS and Mutual Funds?

Yes. Many HNIs may use both PMS and mutual funds in the same portfolio.

A practical way to think about this is the core-satellite approach:

- Mutual funds can form the core portfolio because they are diversified, liquid and suitable for long-term goals.

- PMS can be used as a satellite allocation for focused, customized or manager-led strategies.

- Debt funds, liquid funds or fixed-income products can support liquidity and stability.

- SIFs or AIFs may be considered separately by sophisticated investors, depending on risk and suitability.

The key is to avoid portfolio overlap. If your PMS portfolio holds the same type of stocks as your mutual funds, the portfolio may become more concentrated than it appears.

PMS vs Mutual Fund for Different Investor Types

Beginner Investor

Better fit: Mutual Fund

Beginners should usually start with emergency funds, insurance, basic asset allocation and mutual funds. PMS may be too complex and high-ticket at this stage.

Salaried Investor

Better fit: Usually Mutual Fund

Salaried investors often benefit from SIPs because they invest from monthly income. PMS may be considered only by high-income salaried investors with large surplus capital and a strong core portfolio.

HNI Investor

Better fit: Both, depending on need

HNIs may use mutual funds for core allocation and PMS for customized satellite exposure. The decision depends on whether customization is actually needed.

Retired Investor

Better fit: Usually Mutual Funds or Conservative Products

Retired investors often need liquidity and income stability. PMS may be suitable only in limited allocation and with a conservative strategy.

Business Owner

Better fit: Depends

Business owners with lump-sum surplus may consider PMS, but they should separate business liquidity needs from personal investment capital.

PMS vs Mutual Fund Based on Goals

| Goal | Better Option |

|---|---|

| Emergency fund | Neither equity PMS nor equity mutual funds; use liquid/low-risk options |

| Monthly investing | Mutual Fund |

| Retirement planning | Mutual Fund as core |

| Long-term wealth creation | Mutual Fund or PMS, depending on corpus and risk |

| Tax-saving under Section 80C | ELSS Mutual Fund |

| Customized equity exposure | PMS |

| Portfolio diversification | Mutual Fund |

| Focused manager-led strategy | PMS |

PMS vs Mutual Fund Based on Risk Appetite

Conservative Investors

Conservative investors may be better suited to debt funds, liquid funds, conservative hybrid funds or other lower-risk products. PMS may not be suitable unless the strategy is conservative and the allocation is limited.

Moderate-Risk Investors

Moderate investors can use mutual funds as the core portfolio and consider PMS only if portfolio size and risk appetite allow.

Aggressive Investors

Aggressive investors may consider PMS for focused equity exposure, but they should understand concentration risk, manager risk and potential drawdowns.

PMS vs Mutual Fund Taxation

| Tax Factor | PMS | Mutual Fund |

|---|---|---|

| Tax trigger | Security-level transactions | Unit redemption, switch or transfer |

| Complexity | Higher | Lower |

| Reporting | Portfolio-level transactions | Capital gains statement / fund statement |

| Equity taxation | Based on individual stock trades | Based on equity-oriented fund rules |

| Debt taxation | Based on underlying instrument | Depends on scheme classification |

| Tax efficiency | Depends on manager and churn | Depends on scheme type and holding period |

PMS taxation can become complex because individual transactions in the portfolio may trigger gains or losses. Mutual fund taxation is usually easier because tax is generally calculated when units are redeemed, switched or transferred.

PMS vs Mutual Fund Fees

| Fee Type | PMS | Mutual Fund |

|---|---|---|

| Management fee | Yes | Included in TER |

| Performance fee | May apply | Usually not applicable for standard MF schemes |

| Brokerage | May apply | Embedded at scheme level |

| Exit load | May apply | Scheme-specific |

| TER | Not the main fee metric | Main expense metric |

| Fee complexity | Higher | Lower |

A PMS investor should understand fixed fees, performance fees, hurdle rate, high-water mark, brokerage and other charges. A mutual fund investor should understand TER and exit load. AMFI’s TER disclosure notes that direct plans exclude distribution expenses and commissions, which is why direct plans generally have lower expense ratios than regular plans.

How Much Should You Allocate to PMS vs Mutual Funds?

This depends on total portfolio size, goals and risk appetite. A simple illustrative framework:

| Investor Type | Mutual Fund Allocation | PMS Allocation |

|---|---|---|

| Beginner | 100% | 0% |

| Regular salaried investor | 90–100% | 0–10%, only if suitable |

| Affluent investor | 70–90% | 10–30% |

| HNI | 50–80% | 20–40% |

| UHNI / family office | Customized | Customized |

This table is only illustrative and should not be treated as investment advice. PMS allocation should be decided after considering liquidity, taxes, goals, existing mutual fund exposure and risk tolerance.

Common Mistakes Investors Make While Comparing PMS and Mutual Funds

1. Choosing PMS only because it sounds premium

PMS is not automatically better because it has a higher minimum ticket. Suitability matters more than exclusivity.

2. Assuming PMS always gives higher returns

PMS can underperform mutual funds depending on the strategy, manager and market cycle.

3. Ignoring PMS fees

Performance fees, fixed fees, brokerage and other costs can reduce post-cost returns.

4. Ignoring tax impact

High portfolio churn in PMS can create tax events for the investor.

5. Comparing returns without risk adjustment

A focused PMS and a diversified mutual fund should not be compared only on absolute returns.

6. Using PMS for short-term goals

PMS is generally better suited for long-term capital allocation, not short-term liquidity needs.

7. Stopping mutual fund SIPs too early

For many investors, mutual fund SIPs should remain part of the core portfolio even if PMS is added.

8. Ignoring portfolio overlap

If PMS and mutual funds hold similar stocks or sectors, the investor may be more concentrated than expected.

Conclusion

Mutual funds are better for most investors because they are accessible, diversified, SIP-friendly and easier to manage. PMS may be suitable for HNIs and experienced investors who can invest ₹50 lakh or more, want customization, and can handle higher risk, higher fees and tax complexity.