Please Do Not Invest In Mutual Funds

For the last few days, I have been talking to a lot of first-time investors. And was greatly alarmed by the kind of conversations I had.

“Will my money double by the next year?”

“I invested in SBI Small Cap Fund one week back and it is down by x% percent, should I sell it?”

“I invested in X fund one month back but Y fund has given better returns, should I switch”

I think various mutual fund campaigns have set very wrong expectations and understanding of mutual funds among beginners.

Mutual funds are one of the best products for retail investors to build wealth or meet other goals – however here are a few important points you should consider about mutual funds.

There is no guarantee of returns in mutual funds

When you look at returns on Groww or Valueresearchonline – they are historical returns. They are returns generated by mutual funds in the past. It does not mean they will generate the same returns in future. Historical returns just tell you how the fund manager has been performing in the past.

As an example, consider Amit who has been a topper in his class for the last 3 years. You can say Amit is very bright academically. We can also say with good chances that Amit would do well in his academic career in the long term. But there is no guarantee, he would be a topper next year.

There is a possibility that Amit will be the 2nd ranker.

There is also a possibility that Amit will fail in case he falls sick on the day of the exam (think market crash).

Investors invest for long-term but they can see returns in short-term

A lot of new investors say that they are investing for long-term, but the moment they see negative returns in their portfolio – they start panicking.

So logically, there might be no need to worry because you invested in small-cap funds for the long term and short term blips do not matter. Your risk capability is high.

But behaviorally – you panic. Investors sell and suffer huge losses. Your risk tolerance is low.

Risk capability is different from risk tolerance level.

Investors invest based on their risk capability but because of a different risk tolerance level, they behave differently when they see negative returns.

SIP is not the solution to everything

Yes, SIP is good for retail investors. It is a good way of saving regularly. It helps in staying disciplined. We don’t need to remember every month, it is automatic.

But it does not mean you will always make positive returns. SIP is just a way of investing in mutual funds. And hence your SIP returns can also go negative.

So never invest in mutual funds?

I am a strong proponent of investing in mutual funds, but against investing in mutual funds if you do not understand them.

At Groww, we try to educate users about advantages and disadvantages of mutual funds. And so you can read a lot of about them in the articles and Groww communities. Here is the most important thing:

The most important thing

The most important thing to know about a mutual fund is its category. If you are right here – mutual funds can become your best friend.

It is more important to choose the right category than choosing the best mutual fund in that category.

If you invest in a small cap category for one year – you are making a big mistake.

If you invest in a small cap category for one year – you are making a big mistake.

Yes, I repeated that line on purpose.

How to choose the right category of mutual funds?

There are a bunch of articles on Groww about how you can choose the right category , but here is a quick primer.

There are different types of funds, but to make it very simple – there are two types.

Equity funds – that invest in stock markets. And Debt funds that invest in debt markets.

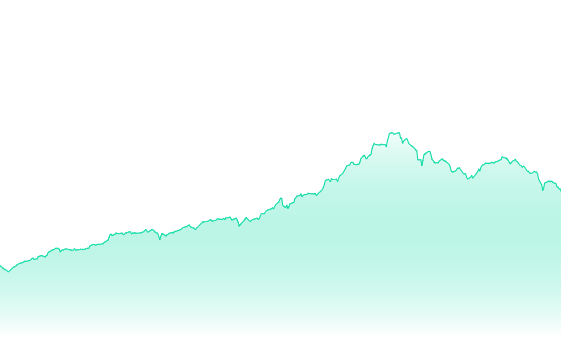

This is how equity funds can behave:

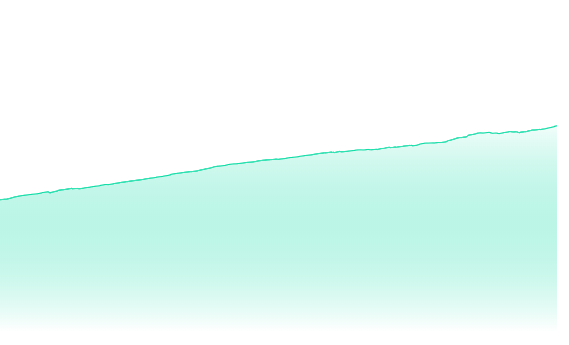

This how debt funds behave:

So whats the difference?

1. Equity funds are more volatile – that is they go up and down with higher magnitude. Debt funds are less so.

2. Equity funds give higher returns in long-term.

There are various types of equity funds – large-cap funds investing in large companies, mid-cap investing in mid-cap companies and so on.

They all carry a different level of risk. The risk level of a small cap is higher than a mid-cap. Mid-cap is higher than large cap. There are also funds that diversify into all. They are called multi-cap funds. If you are a beginner, I recommend starting with multi-cap funds while you learn about other types.

Likewise, debt funds also have different types (liquid funds, ultra-short duration funds, short duration funds). For beginners, I recommend to start with liquid funds or ultra short term funds and then learn about other funds.

Investing is about learning while doing. The key is to not make a major mistake. The key is not getting out too early. It is a test match of your life.

Happy investing.

Disclaimer: The views expressed here are of the author and do not reflect those of Groww.