Analysis: How does the future look for Hero MotoCorp?

Hero MotoCorp is one of the leading players in the two-wheeler market. According to various media reports, Hero commands a significant chunk (32-35%) of market share in the two-wheeler segment in India.

With the way the petrol prices are skyrocketing, there are high chances for many of us to postpone a bike purchase!

If buying a bike isn’t happening soon, what about the stock of Hero MotoCorp?

Before you make any investment decision on this stock, it is better for you to understand the company and the industry.

The two-wheeler industry in India has witnessed a slow demand off-take mainly due to an increase in petrol prices and a rise in prices of bikes/scooters. In this regard, the stocks of the top players, including Hero MotoCorp, Bajaj Auto and Eicher Motors, have been down 13% on average in the past six months.

But according to various experts, the outlook for the two-wheeler industry is strong. This is on the back of many players stepping up on the electrification of bikes pick-up in demand from urban and rural areas, particularly with the festive season coming up, new launches and opportunities in the export market.

So, how does Hero fare against the competition? Do the company’s prospects remain bright in the coming years?

Let’s find out.

What works for Hero MotoCorp?

Hero MotoCorp is one of the leading players in the two-wheeler industry, focusing mainly on entry-level two-wheelers. That is, for mid-income category customers. The past few quarters have been difficult for the company due to a slowdown in demand. The company reported a 29% decline in volume in February this year.

Hero’s volume decline is slightly higher than its peers. For instance, Honda reported a 24% decline in volume during the same period. Baja Auto and TVS volume was better. The volume decline was around 16% and 7% y-o-y in February 2022.

Despite the weak cues for Hero MotoCorp, the company is on the path to recovery.

There are a few factors to support this argument. They are:

Diversification

Even with the demand slowdown, Hero MotoCorp continues to be in the leading position in the domestic two-wheeler segment. According to various media reports, it holds over 32% of the market share in the country.

While Hero had been mainly focusing on entry-level bikes that cater to mid-income category customers, the company has made a conscious effort to diversify its product offerings. That is, it caters to all income categories of customers. This had been in the works in the past few years. The company had been launching bikes in the premium segment, like Xpulse 200 and Xtreme.

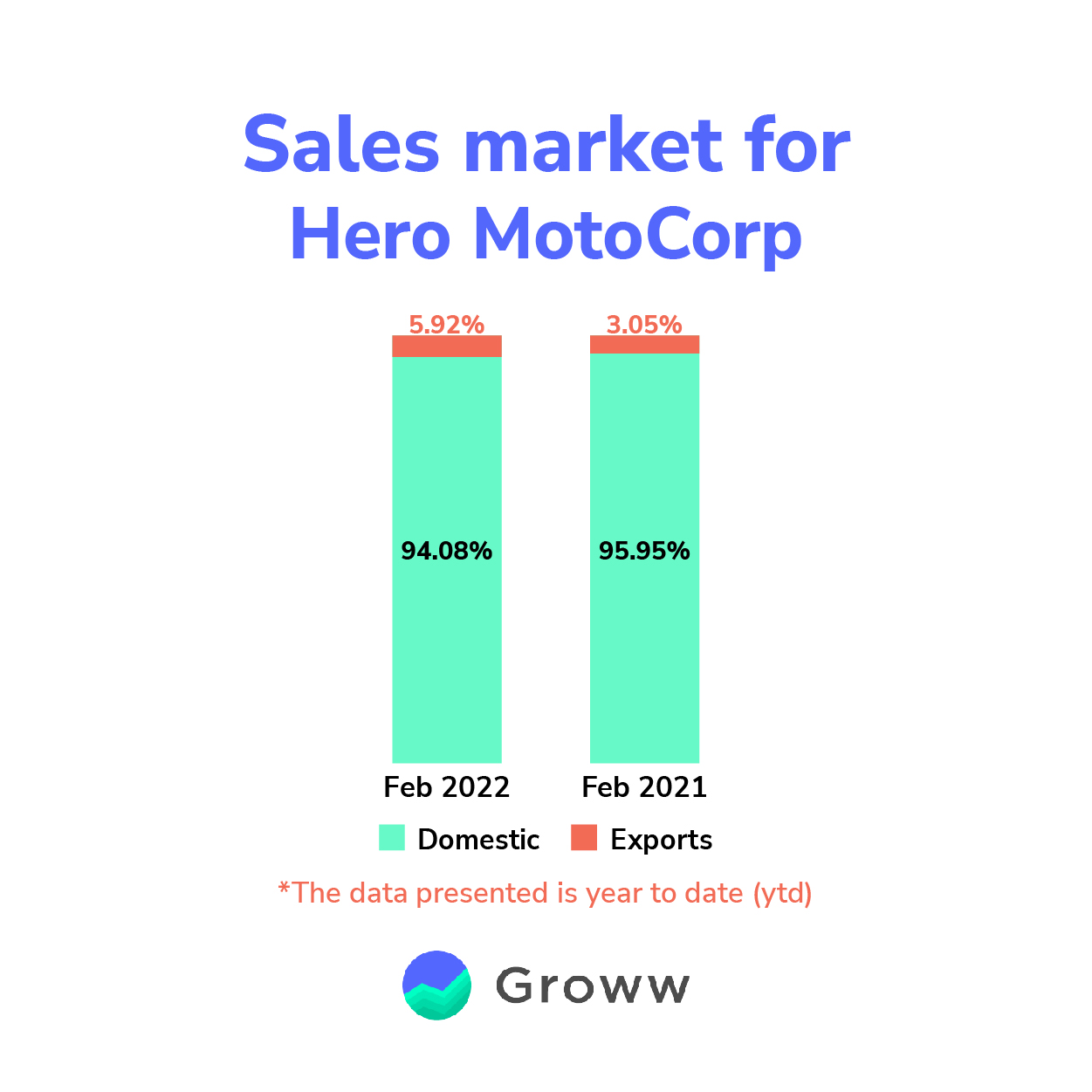

Further, it also started to explore the export market, like other players. And slow pick-up can be witnessed in that segment as well. For instance, in February 2022, the export segment saw a growth of 27% y-o-y.

All these growth drivers are likely to show their results in the coming quarters.

Dominant player

According to many experts, Hero had been slow in diversifying to the premium bike segment and penetrating the export market.

But despite these challenges, the company had been able to retain its dominant market share (domestic) in the two-wheeler industry. To offset increasing raw material costs, the company has taken price hikes. In the recent December quarter of 2021 (FY22), the company took a price hike of Rs 1,000 (ex-showroom price). As per the company’s statement, the management plans to take another price hike in the March quarter of FY22.

Strong brand position and vast dealer network have helped the company. It has a presence in Tier I cities and other cities and towns, especially in under-penetrated Tier II and Tier III regions. Hero’s market position in the country is likely to aid in its diversification strategy, particularly in premium bike segments.

(Original Equipment Makers -OEM)

Offtake of electric bike

Though Hero MotoCorp is late in joining the EV (electric vehicle) race, the company has a broad range of electric scooter products plans in the coming quarters. Accordingly, it has made its investment in Ather Energy plans to launch fixed battery and swappable battery for electric bikes. The company has joined hands with BPCL to introduce EV charging stations as per media reports. The company has also invested in Gogoro and Poema Holdings for battery swap technology.

The company’s extensive dealer network could come in handy with its EV take off. It has over 9,000 customer touchpoints.

Other factors

The are other factors that could also aid in the growth of Hero MotoCorp.

- The Government has introduced various structural reforms that could benefit the overall 2W industry, including Hero MotoCorp. Further, there are multiple reforms targeted at the agriculture sector. This could help Hero MotoCorp as it has a better presence in tier II and tier III regions.

- The rise in the middle-class population and Hero’s presence in entry-level bike/scooter segments are key positives. When the demand recovers in the market, Hero could improve faster than its competitors.

- Three, the company has maintained stable debt levels. Its debt-to-equity ratio is less than 1, thereby giving room for future expansion if any.

Valuation

Before investing, weigh the pros and cons of the company.

Hero’s recent December quarter (FY22) performance had been weak. It reported a revenue and profit decline of 18% and 31% y-o-y respectively compared to last year.

But its valuation appears reasonable when compared to its peers. Hero is trading at (PE) 17 times while Bajaj Auto trades at nearly 21 times and TVS Motors is 36 times.

Challenges ahead

While the stock has multiple positives, there are a few concerns.

Cost pressure

Two-wheeler makers, including Hero, feel the pinch with increased commodities prices. For bike makers, commodities including aluminium, steel, rubber and other petroleum products are required. And the prices of these commodities have skyrocketed in the past year. Hero took a price hike in 3QFY22 (December quarter) to negate the raw material cost pressure and is expected to take more in the March quarter. However, considering the segment Hero operates in (entry-level bikes), the headroom to take on more price hikes could be limited. If the prices of the raw materials continue to rise, then Hero’s margin and profit could have an impact.

Competition

Though Hero is one of the leading players in the market, it faces stiff competition, particularly in the premium bike segment. Players including TVS Motors, Bajaj Auto and Eicher Motors have a headstart.

Similarly, in the EV segment, not only the established players like TVS and Bajaj Auto are already present, but other players, including Ola Electric, Ampere Electric, and Okinawa, are also competing. Hero is late to join the market, and it could be challenging to catch up.

To read the RA disclaimer, please click here.

Research Analyst: Bavadharini KS