Do You Want to Start Investing? Here Are the Essentials!

Maybe you’ve just got your yearly bonus and a novel idea has struck you: what if I invest this money?

You’re on the right track. The right investment early on in your career can pay off big if you play your cards well. But before you even start investing, there are some basics that you should take care of.

For instance, a lot of people begin investing before they have cleared off their dues fully or taken care of basics like insurance.

This is a bad idea.

Investments should only be done with the money you have. Never invest money that you don’t have.

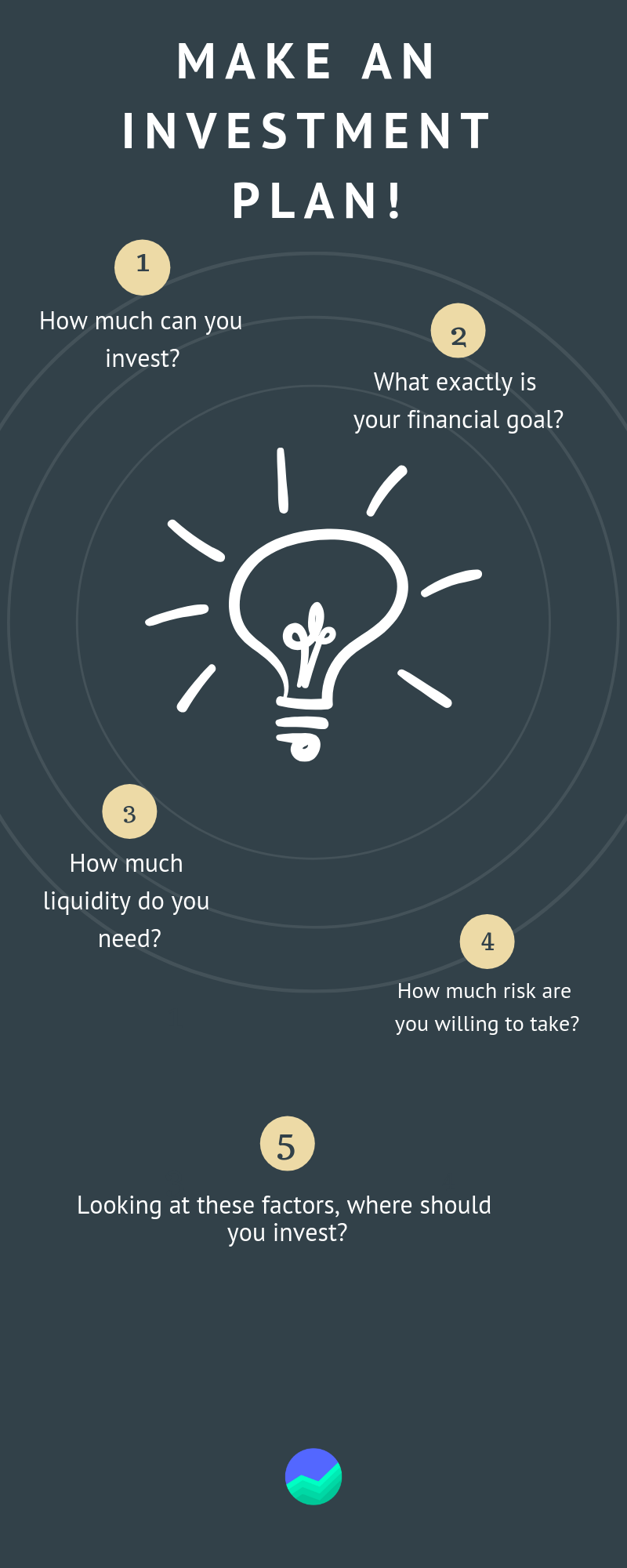

Another important part of investing well is to have a financial plan. A solid financial plan is not only essential but unique to every person depending on their financial situation.

In the increasingly gig dependent economy that we live in, not everyone has a stable monthly income.

Some of us might be freelancers, who get periodic windfalls of money. Depending on your salary, expenses and future plans, you can chalk out a financial plan that is unique to your spending pattern and needs.

A well chalked out financial plan would cover all aspects of one’s financial goals, including present financial situation, future financial situation, any financial goals you might have, how to implement the plan itself, and crucially, alternative courses of action in case Plan ‘A’ doesn’t work out.

However, simply implementing it doesn’t mean your work is done. The financial plan also needs to be revised periodically as circumstances change. This brings us back to the original point, investing money is a big part of the planning process. But before you invest, there are some basics which should be taken care of first:

Step 1: How Much Do You Need for Household Spending?

Sketching out a household budget should be one of the most basic accounting practices that everyone should follow. The household budget is where the bulk of everyone’s salaries end up going anyway, so it’s important to keep track of these expenses and keep them efficient so that you have more to save.

The first thing you need to do is note down on a piece of paper your sources of income.

This would include your salary, bonuses, returns from other investments, money from freelance work and so on and so forth. Once you have a clear grip on approximately how much money is coming in every month, you can start monitoring your spending practices.

The second step here would be to start noting down your expenses. Start with the basics: rent, grocery bills, electricity bills, WiFi and any other such recurring expenses. This is usually a bulk spend that all of us do every month.

Now comes the crucial part: you need to monitor how you’re spending the rest of your money and where.

One way to do this is to draw up your bank balance and look at how much you’re spending on say, online shopping, Uber and Ola, fuel, eating outside etc.

If you don’t have the patience to go through your bank statement, there are also apps like the Walnut Android App which will go through your SMSes and track this information automatically for you.

This is variable spending, depending on what your needs are for that particular month, so a little more judiciousness here can go a long way in your savings plan.

Step 2: Pay off Your Debt

While India has many investment options, we can’t stress enough how much clearing off your debt matters!

The faster you settle any existing debt, the faster you can make money off your investment. For example, if you’ve invested in a mutual fund through the Groww app and get a ten per cent annual return, it’s going to be totally pointless if you’re going to spend that extra ten per cent paying off your existing debts instead of saving or re-investing it.

There are many types of debt, but a debt that people usually struggle with is generally divided into two types: the first is called unconstructive loans, which usually refer to personal loans, car loans and credit card debt.

In India, credit card debt is rising at an exponential rate. As of May 2016, the total credit card debt incurred by Indians was 42,100 crore, compared to 27,000 crores during the great recession of 2008.

If you have an outstanding credit card debt, it is wise to take stock of the situation and plan of paying off the principal amount as quickly as you can. You can also convert this into a personal loan to prevent you from paying too much interest.

The second category of loans is constructive loans and generally include things like home loans which have an interest rate of close to 9 per cent.

These are easier to manage than credit card debt which has a rate of 36 to 48 per cent a year. But they still need to be paid off. To make the most of your investment, make sure your debt is taken care of.

Step 3: Have a Contingency Fund in Place

Life can be unpredictable. As we have discussed in previous articles, you might have a medical emergency, which can lead to a hefty hospital bill.

Or worse, you could be laid off from work and have no money. In these cases, many people turn to credit cards, which is a recipe for debt.

In case things don’t go as planned, credit card bills can compound and skyrocket very quickly. In these cases, it is absolutely essential to have a contingency fund.

You can start by setting up an online savings account. Once you have set up your account, you can transfer a certain amount into the account every month without breaking the bank too much.

Over time, this will build and give you a solid contingency amount for when difficult situations arise. Ideally, you should save an amount equivalent to 3 months of your salary as a contingency amount.

Step 4: See the Big Picture and Seek Good Advice

The biggest mistake you can make while investing is not having a plan.

To have a solid plan, you must be aware of what you want out of your investment. To have an investment plan, you must have an achievable financial plan. To start achieving your financial plan, you can break it into smaller steps and get them done one by one.

Let me tell you this, some of you might think that taking financial advice is not the right way to go about things. And what if the “advice is wrong?”, what if “It’s a scam?”.

That’s the wrong approach.

If you feel like you are jittery about the finance world, there is no harm in taking help from a financial adviser!

Also Read – Best Investment Options in India 2022

Conclusion

Once you have enough money to invest, don’t go just by intuition. Although stocks are a great option, for early investors, the mutual fund route is much more preferable because you’re essentially trusting your money with someone who knows the market much better.

At this stage, it’s also a good idea to consult an expert. However, you don’t need to pay an expert to give you advice throughout the duration of your investment journey. An initial input and some periodical guidance should do.

Disclaimer: The views expressed in this post are that of the author and not those of Groww