Adani Wilmar Analysis – Growth, Revenue & Technical View

Adani Wilmar Ltd (AWL), is one of the top companies that have attracted investors’ interest since its listing in February 2022. The IPO price was Rs 230 and the stock trades at Rs 680 today (May 02), delivering a return of about 80% since listing.

There are a few reasons why most investors like this stock.

- One, the prospects of the company appear to be good. While it is among the leading players in the edible oil market, Adani Wilmar has plans to improve its food and FMCG segment.

- Two, in addition to edible oil, it provides other kitchen essentials, including rice, wheat, flour, pulses and sugar. These are staples, and there is always demand for such products.

- And three, AWL is one of the companies that has an integrated business model. That is, its manufacturing is well integrated that one business segments support the other. It drives the needed cost efficiencies across businesses. Further, most of its raw material requirements come from Wilmar Group (imports).

- Other factors including a wide distribution network, and good brand recognition work in AWL’s favour.

While it appears to be a good stock investment, there are a few pointers that investors should note and understand.

About Adani Wilmar

The company was started in 1999, as a joint venture between Adani Group, a large conglomerate in India and the Wilmar Group. Adani Wilmar is one of the largest players in the FMCG market specifically offering kitchen essentials. These include all kinds of edible oils, pulses, sugar and rice and flours.

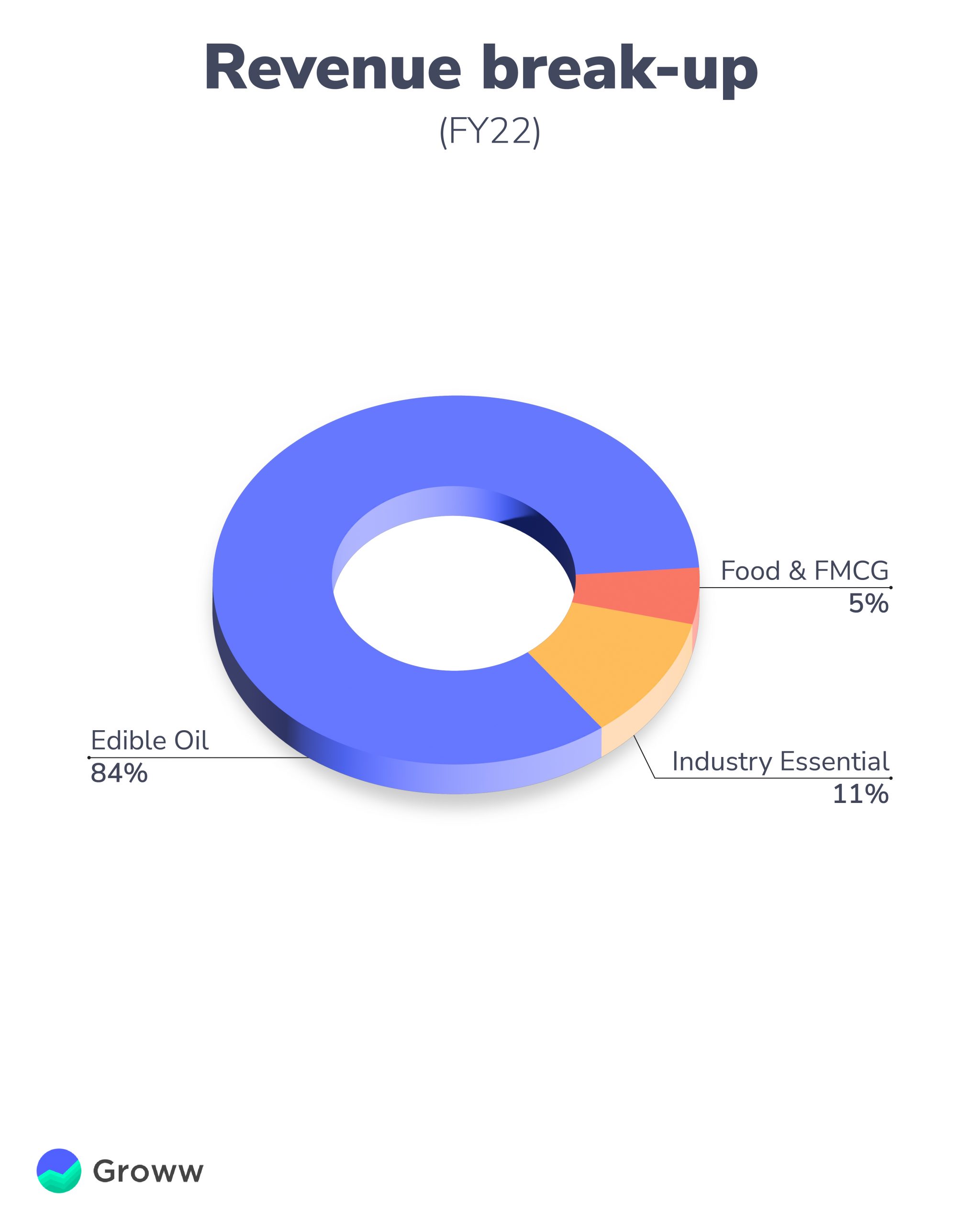

The company operates in three main categories – edible oil accounts for a chunk of the company’s revenue, about 83%. The other two segments, packaged food and FMCG and industry essentials offer 5% and 12% of the company’s revenue respectively.

Even in these three-business segments, AWL offers a wide platter of products. This diversification helps in reducing the risk of dependency on one product and is working well for the company.

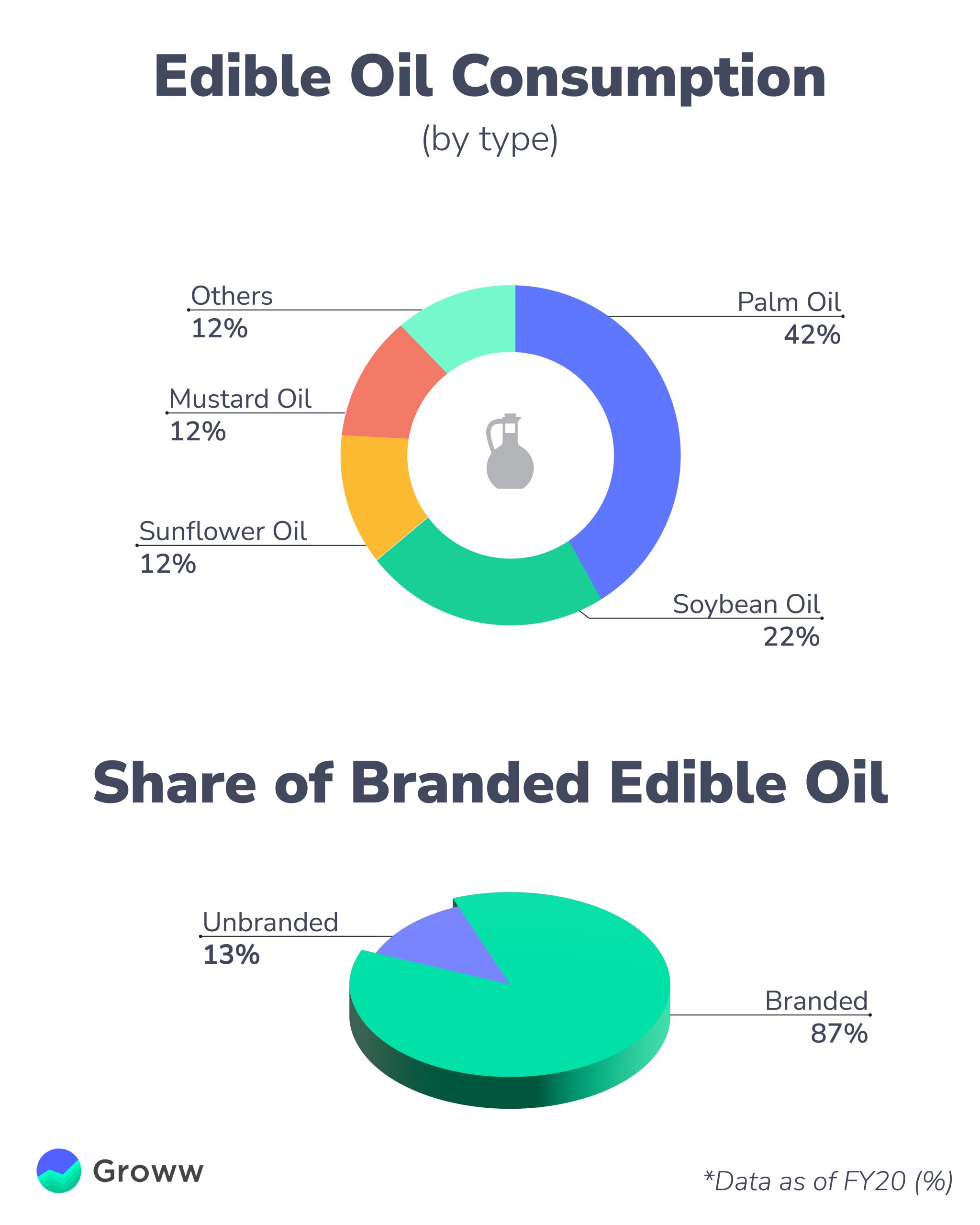

Take its Edible oil business segment for instance. AWL is present across all edible oil segments including palm oil which contributes about 38% of revenue, soya oil (38%), sunflower oil (12%), mustard oil (8%) and other oils account for 3%.

Where does Adani Wilmar’s growth come from?

Adani Wilmar has strong brand recognition in the domestic market and has a leading position in most of its products.

While the demand for products like wheat, rice, flour, and edible oil is constant, there are a few key triggers that helps in the growth of the companies operating in these segments in the coming years.

Preference toward packaged products:

There is a growing preference among consumers for packaged food instead of loose and unbranded products. This segment is likely to grow at the rate of 14% in the coming years as per industry reports. Health concerns and quality standards have accelerated this adoption.

For Adani Wilmar, this market condition bodes well. It has a dominant market position when it comes to edible oil. It comes in handy for expanding in new and value-added packaged foods.

- There is growth potential in RTE (ready-to-eat) and RTD (ready-to-drink) products and certain kitchen essentials like flours, rice, pulses and atta. And the company has plans to expand in this space as well.

- While the FMCG space is already competitive with players like HUL, there is still space for growth. This is because the market space for most kitchen essentials like atta or pulses is highly fragmented with regional and local players. For instance, AWL (through Fortune brand) has entered the atta market. For the year FY22, the company has launched Poha and Khichdi under RTE.

Increasing edible oil consumption:

Oil, like water, is one of the essential parts of everyday life. Considering the changing preferences of tastes of consumers, new and innovative eateries entering the market are driving the growth of all kinds of edible oil in India. And the largest oil consumer is food processing units like hotels. This is good for oil makers like AWL.

Brand

While the branded edible oil market is competitive, AWL’s brand of Fortune is among the leading players in the industry. There are four key edible oils that contribute about 85% of revenue for most players and the industry. These are palm, soy, mustard, and sunflower oils.

- Palm oil is mostly used in hotels, restaurants and even by caterers. And the other three oil is for domestic consumption. However, industry experts expect a shift towards lesser consumption of palm oil, considering the health benefits of other oils. So there is demand for other oils as well.

AWL like other players has established its brands of oils to cater to all socioeconomic classes of consumers. For instance, Fortune brand of sunflower oil caters to mostly premium consumers.

Distribution network

Adani Wilmar has the largest distribution network among the players in the industry when it comes to edible oil. The company has over 5600 distributors almost across all the States/UTs. The company also has its products across all the e-commerce platforms and via its own online platform. It is estimated that there are around 4.5 Mn retail outlets present in India and Adani Wilmar covers almost 35% of those.

Industry essentials:

AWL, in its industry essentials business, offers products like oleochemicals like stearic acid which are used in making soaps and other home and personal care products.

It also offers castor oil and its derivatives to industries like cosmetics and pharmaceuticals.

Lastly, it offers de-oiled cakes which are basically a by-product of oil extraction from soybean, castor and mustard etc, and serves as livestock feed.

It is among the largest manufacturers of industry essential products. Since sourcing raw materials aren’t challenging, the company is able to retain as well as expand its market in this segment.

Further, the company leverages its oleochemical manufacturing in its FMCG division to offer soaps and handwashes.

Key strengths of Adani Wilmar

Now that we know the growth potential for Adani Wilmar. Let’s understand a few of the strengths of the company.

Brand loyalty:

- AWL has a leadership position in the market when it comes to edible oil in India. ‘Fortune’ is the flagship product of the company and is the largest selling edible oil in India as per the company’s DRHP. The company’s other brands that are popular in different regions include King’s, Alpha, Raag, and Jubilee.

- AWL, according to its management, is on the lookout for strategic acquisitions. The plan is to consolidate the market share through acquisitions of regional players. Recently, Adani Wilmar acquired the Kohinoor rice brand to strengthen its position in the basmati rice business. It is also to establish its presence in FMCG.

- Adani Wilmar has strong raw material sourcing capabilities. Wilmar International, the promoter group, is among the largest palm oil supplier globally. And it provides the company with an additional competitive edge in terms of raw material sourcing. Thus, the company doesn’t depend on third-party suppliers. For instance, in FY21, about 30% of imported raw materials by value were sourced from Wilmar Group. This sourcing benefits AWL from price volatility. In India too the company has established a broad procurement network.

Integrated businesses:

Most of Adani Wilmar’s manufacturing units are fully integrated with refineries. For instance, the company uses palm stearin from palm oil refining to manufacturing oleochemical products like glycerine and stearic acid (for industrial use). It is also used in FMCG products like soaps and handwash. These backward and forward integration helps the company to achieve cost efficiencies across different business lines. Additionally, it has enabled the company to share its supply chain, storage facilities and distribution network.

Financials

Take caution before stock investment

Before you, as an investor consider buying or investing in Adani Wilmar, there are a few pointers to note.

- Commodities prices usually tend to fluctuate during lean and peak seasons. And in-turn AWL’s revenue could also fluctuate.

- Similarly, high commodities prices could also lead to high input costs. This could take a toll on the company’s operating margins. Input costs account for about 85-88% of FY22 revenue for the company.

- Considering that AWL imports most of its raw material requirements, currency fluctuations should also be kept in mind before investing. Further, Government regulations such as trade disputes or geopolitical disputes (Russia-Ukraine situation) between countries could be a risk for raw material prices. However, the company does have risk mitigation strategies in place in case such a situation arises.

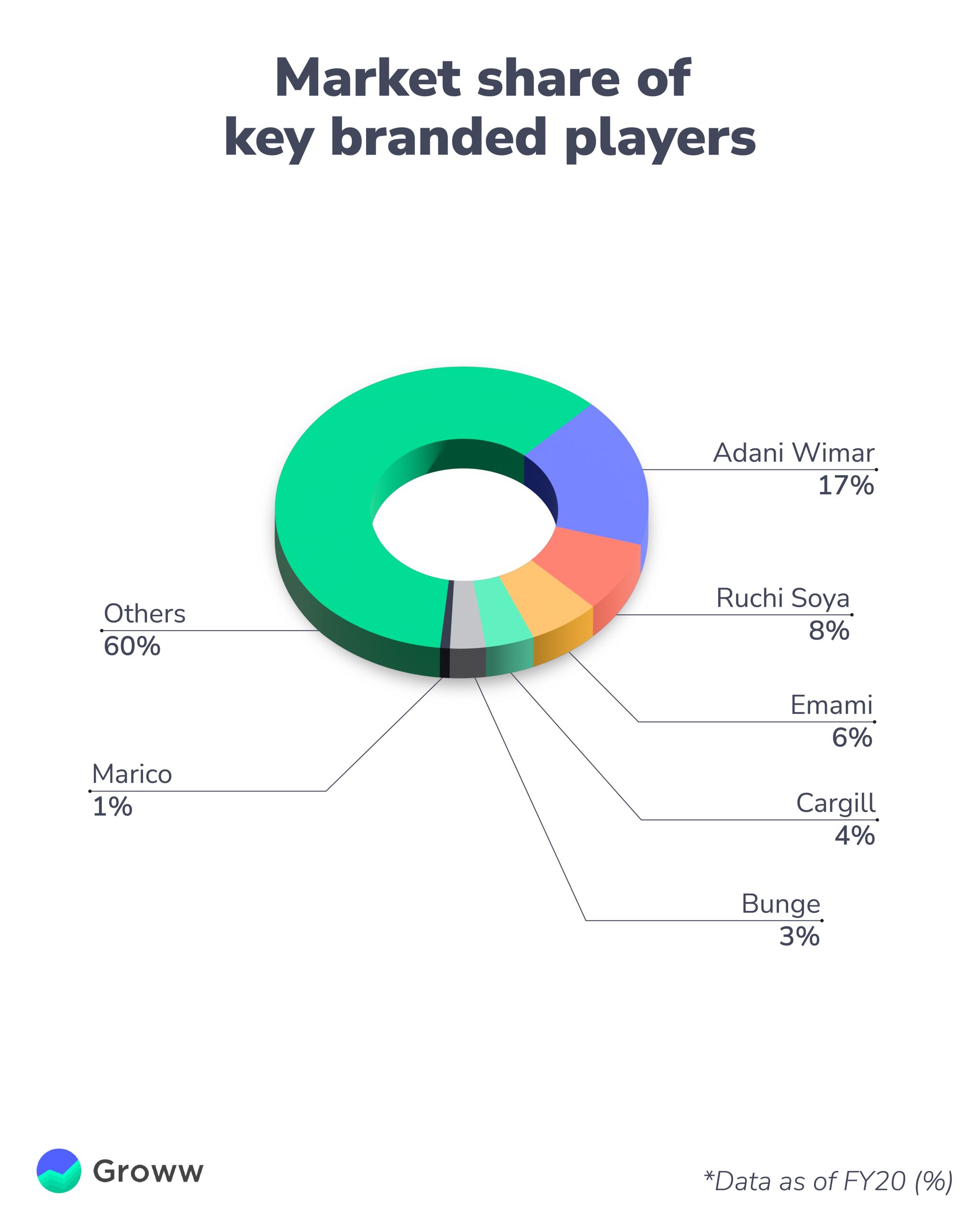

- The competition in the business the company operates is stiff. For instance, even in the edible oil segment, the mainstay business for the company, it faces competition from Ruchi Soya, Kaleesuwari Refinery and Emami Agrotech.

- Now, considering that AWL plans to expand in packaged foods and other FMCG products, capturing market share could be difficult with players like ITC, Nestle, Parle, and Britannia already in that space.

Valuation:

While Adani Wilmar’s IPO was fairly priced (at the time of its IPO), the stock has rallied from Rs 227 (listing price) to Rs 680. The stock currently trades around 110 times. This appears expensive when compared to its peers like Ruchi Soya (41 times) or HUL (58 times).

Technical View on Adani Wilmar

Adani Wilmar had quite a strong bull run immediately after the listing. In fact, in the first three days, we saw huge returns of around 70%. The stock went on to form an all-time high of 878 and from there on things went downhill.

The question here is if this is a healthy correction? The general notion is that any correction in between 10 to 20% is deemed a healthy correction. But in the case of Adani Wilmar, the stock has corrected in excess of 25%.

Until now, the stock was in an uptrend forming higher highs and higher lows. But now the price is at a very crucial level, we have a support zone at Rs 640 which is also a higher high. If the price breaks this level we can expect a further sell-off.

Moving average

Usually, when we are determining the trend of the stock, most investors naturally turn towards the 200-day moving average.

The idea is whenever the stock is trading above the 200-day moving average it is considered bullish. And whenever the stock is trading below the 200-day moving average the stock is considered bearish. Here since the stock has not been traded for 200 days, we will not be able to determine the 200-day moving average.

We shall however look for a 21-day moving average to determine the immediate trend. The 21-day moving average is 683.95 currently and the price is trading at 646.20 which goes to point out that the stock is bearish.

RSI

RSI is yet another tool which can help in identifying the general trend. Traditionally RSI is considered overbought above 70 and oversold below 30. In the case of Adani Wilmar, we can see a sharp decline in the RSI value. In this case, the RSI value is at 50.48 indicating the lack of bullish momentum.

All in all the stock at this particular moment looks quite weak in the lens of technical analysis.

We can expect a change in trend towards the upside, only if the price comfortably starts trading above the 21-day moving average. The immediate support for this stock is at 640 followed by one at 550.

(All the technical analysis was done on May 06, 2022)

To read the RA disclaimer, please click here

Research Analyst: Bavadharini KS