What Is Side Pocketing in Mutual Funds? (Explained With Examples)

After the unveiling of the IL&FS crisis back in September 2018, the investor community has become very cautious about their investments.

Amidst this, the industry is keen that the regulator allows schemes that have debt exposure to use side pocketing.

To begin with, let us start with the background of side pocketing to set the context right.

What Is Side Pocketing in Mutual Funds?

Side pocketing is a technique to safeguard investors in instruments that have exposure to risky assets.

It is basically an accounting method that is used to separate illiquid investments from liquid and quality investments, in a debt portfolio.

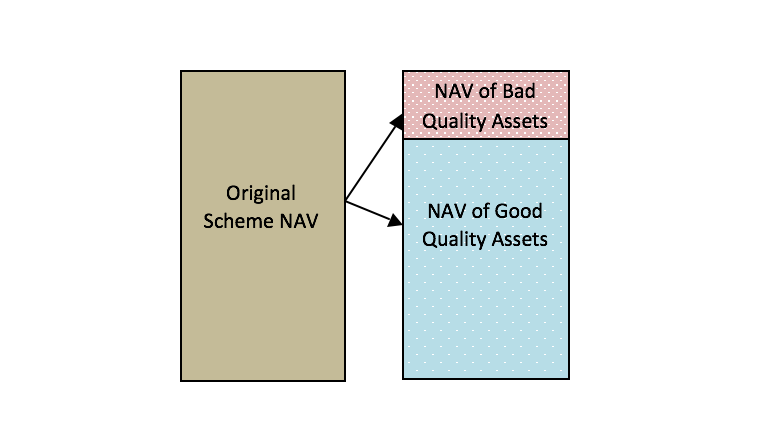

How Does it Work?

Whenever there is a case of rating downgrade for a bond that is held in the fund, the fund houses push the illiquid asset into a side pocket, and the existing holders receive a pro rata allocation in it.

What Is the Impact of Side Pocketing on NAV?

When side pocketing is implemented, and illiquid assets are pushed in a separate pocket, the fund’s NAV reflects the value of liquid assets only — a different NAV assigned to the side pocket assets based on an estimate of the realizable value of investors.

Does it Safeguard Investors?

With the help of side pocketing, risky bets can be segregated from the safer and liquid investments that may get impacted due to changing credit profile of risky assets.

And herein, the efforts are made to stabilize the net asset value of the scheme so that redemption by small investors does not get impacted due to any sudden exit by large investors.

Side pocketing also ensures that investors who were in the investment at the time of write-off will get a benefit if there is any recovery from the bond.

The process of side pocketing ensures liquidity is not choked for investors holding the units of the primary scheme as allotment and redemption are done on liquid assets.

Recent Development

The Securities and Exchange Board of India (SEBI) which is the market regulator has allowed debt mutual funds to implement the “side pocket” concept.

Earlier, the regulator was not in favour of side pocketing and did not allow mutual fund houses to segregate their bad investments.

Back in 2016, post the JP Morgan Asset Management (India)’s investments in Amtek Auto defaulted and the fund house resorted to the side pocket, the Association of Mutual Funds of India (AMFI) approached SEBI for the creation of rules surrounding side-pockets when the market faces a credit event.

However, SEBI did not accept the recommendation then.

In 2018, many debt schemes saw a sharp fall in the NAV. After these schemes, investments in Infrastructure Leasing & Financial Services Ltd (IL&FS) and some of its subsidiaries saw credit rating downgrades.

This crisis resulted in the change of regulation in debt funds.

Will Side Pocketing Encourage Fund Houses to Take More Credit Risk?

Quoting Ajay Tyagi, Chairman of SEBI, “No, enough steps will be taken and safeguards will be put in by SEBI to ensure that this facility is not misused. The final guidelines will contain these safeguards.”

Once the segregation of investment is done, segregated or toxic investments will be closed for future subscriptions. However, investors can continue to subscribe to the portion that comprises liquid assets or safer assets.

In a situation of crisis, generally, institutional investors have the first right to redemption. This process leads to retail investors getting stuck in segregated or toxic assets.

Thus, implementing side-pocketing in such a scenario helps fund houses manage redemption pressures better given the fact that other holdings are not impacted.

Let us now understand the process with an example –

Example

Assume a fund has 1000 Crore as the corpus. Of this, 50 crores is held in a company that is defaulting on its debt obligation. Under this situation, an institutional investor prefers to redeem the entire investment.

This redemption forces the fund manager to sell good bonds to pay large investors. This process results in toxic assets remaining at the end accounting for the high proportion of corpus.

Thus, retail investors get impacted due to the process.

To safeguard every investor, side pocketing will be implemented, whereby, 50 crores will be segregated and 950 crores will act as the safer corpus. Investors (both institutional and retail), will then be provided units according to the new allocation.

Disadvantages of Side Pocketing?

Side pocketing is a process that should be used cautiously. Also, the valuation of illiquid investments is contentious. Thus, the NAV of the illiquid asset will remain a concern.

Also, two NAVs – one each of the liquid asset and the illiquid asset will be difficult to track for investors.

Lastly, fund houses will be empowered more with the option of side pockets. Thus, the onus of using the method judiciously, and rationally lies with the fund manager.

Disclaimer: The views expressed in this post are that of the author and not those of Groww