The Mid-Cap Sector Revives, but Why Should Investors Be Careful?

The mid-cap sector has undergone a roller coster ride since 2017.

The segment that generated over 48.1 per cent returns in 2017 concluded 2018 at -13.4 per cent and is currently at -2.0 per cent returns in 2019 as of May 28, 2019.

If we have to dissect the performance of 2019 in two parts, let us look at the following two charts.

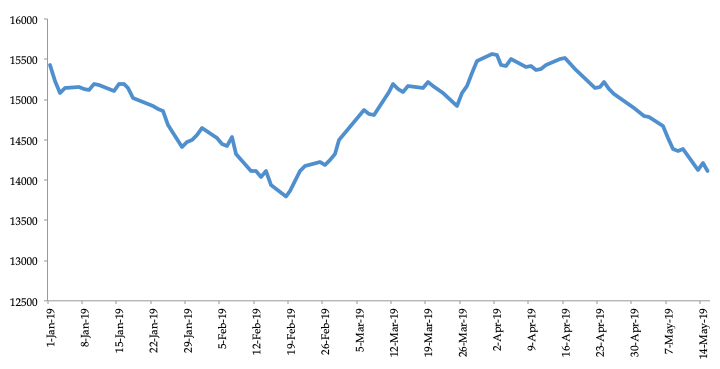

BSE Midcap Index between Jan 1, 2019, to May 15, 2019

Source: BSE

BSE Midcap Index between May 15, 2019, to June 12, 2019

Source: BSE

Clearly, the second chart shows positive returns. This is the period after May 15, 2019 – the period when it was pretty much clear regarding the verdict of the general elections 2019.

In this blog, we seek to discuss how an investor should react to this sudden change in the environment after the elections. We shall discuss how an investor like you and me should read this movement, but before that, let us see the state of the economy currently.

While we accept the fact that the people's mandate has been magnificent with the party of the prime minister gaining a majority share in the lower house of the parliament, the victory isn’t immune to the slowdown in the economy which is lingering currently.

If we have to talk of the economic situation in India, the Reserve Bank of India (RBI)’s cut in growth estimate for fiscal 2020 from 7.2% to 7% is a testament to the fact that the path to economic recovery appears daunting.

Is the Slowdown Different this Time from the Past?

In India, the slowdown, this time, is different from any time in the past three decades. In the past, the downturns were majorly driven by global outbreaks such as currency volatility and high oil prices, geopolitical tension, trade barriers, and the likes.

However, this time around, the nation is in the middle of a structural slowdown. For the first time since the liberalization of 1991, the country is facing a downturn due to a decline in private consumption. The economy is facing a sharp decline in its savings rate for two decades.

On the one hand, the private capital expenditure has remained sluggish for the past few years, and the consumption engine that was pulling the economy all this while is losing its steam on the other hand.

Also, the economy is facing the problem of piling bad loans in formal and shadow banks (non-banking finance companies).

How Has the Consumption Pattern Been?

If we see the consumption pattern currently, the private consumption breakdown is reasonably broad and structured. Housing demand has remained sluggish for several years now.

Also, automobile sales have slowdown in the recent past with the weakest performance coming in the fourth quarter of fiscal 2019.

This decline has compelled some large automobile players even to shut down their plants in the running month. In addition to automobiles, the fast-moving consumer goods (FMCG) sector is also seeing a decline in volume growth over the past few quarters, particularly the fourth quarter of fiscal 2019.

We believe the ongoing consumption slump in the economy is a mix of the decline in savings, credit, income, and business confidence. These factors have resulted in the synchronized collapse of demand in credit-driven sectors such as housing, auto, and consumer durables.

RBI and the Slowdown

The complexity of the slowdown has compelled the RBI and the government to take measures that may only aggravate the pain over time. Despite three consecutive rate cuts by the central bank, the interest rate has not seen any cooling down. We believe a shrinking deposit base coupled with a tepid growth rate in deposits has not allowed the banks to transmit the rate cut to the borrowers.

Also, the RBI has denied any direct or indirect lines of liquidity for NBFCs despite the government’s willingness to bail some of the names.

Now, due to fiscal pressure and a possible contraction in revenue, the government is likely to cut spending, which could have a ripple effect on the slowdown intensifying further. So, the situation is more like a vicious cycle now, and the government will have to take some severe measures to break this cycle.

When an ailing economy needs a massive dose of funds, the funding pipeline of the government dries up due to the rising deficit and sinking revenues. Thus, the segment mainly mid-cap is not likely to get any fillip immediately with the victory of the Narendra Modi-led BJP.

BSE mid-cap has seen a decline since June 3, 2019, and many mid-sized companies rely on loans to meet the working capital requirement and thus are prone to liquidity tightness in the financial system.

Conclusion

To conclude, we can say that growth has to come back, but the situation doesn’t indicate it is coming any time soon. This, as an investor, remain cautious of the economic situation before taking any bets in the capital market.

The main aim for investors currently should be a scout for fundamentally sound businesses, that have scalability options and are trading at a discount.

An investor should look for companies in the segments such as insurance and consumer-focused sectors where the impact will be short-lived.

Happy Investing!

Disclaimer: The views expressed in this post are that of the author and not those of Groww